Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic lRead more

Simply explaining the meaning of the useful life of an asset, it is nothing but the number of years the asset would remain in the business for purpose of revenue generation, making it more simple, the amount of time an asset is expected to be functional and fit for use. It is also called economic life or service life

It is a useful concept in accounting as it is used to work out depreciation. By knowing this useful life of an asset an entity can easily analyze how to allot the initial cost of an asset across the relevant accounting period rather than doing it unfairly manner.

How do we calculate the useful life of an asset?

The useful life of an asset is not an accounting policy, but an accounting estimate. calculating useful life is not an exact phenomenon but an estimate that is done because it directly impacts how much an asset is to expense every year.

Factors affecting “how long an asset is expected to be useful” depends on some stated points as below:

- Usage, the more the assets are used, the more quickly it will deteriorate.

- Whether the asset is new at the time of purchase or reused model.

- Change in technology.

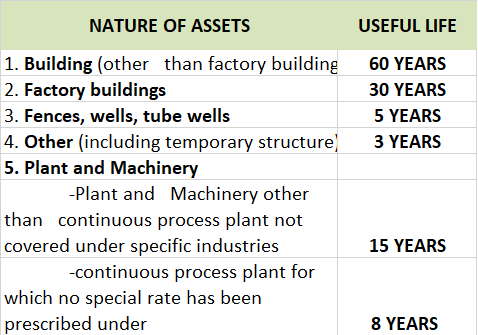

As per the companies act 2013, some of the useful life of assets are stated below

To know more about the different categories of assets you can follow the given link useful life of assets.

POINT TO BE NOTED:- There lies a huge difference in the useful life v/s the physical life of an asset. It is very important to note that amount of time an asset is used in a business is not always be same as an asset’s entire life span.

See less

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization's activities. For example - Tax Authorities, Banks, Customers, Trade Unions, Government, Investors,Read more

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization’s activities.

For example – Tax Authorities, Banks, Customers, Trade Unions, Government, Investors, or Creditors.

External Users:

Here is a summary of external users

See less