The correct answer is the 1. Bank statement and bank column of the cash book, because it will help the business to verify whether amounts entered and entries recorded are correct or not. It will also help in verifying the balances of bank statements and cash books whether they tally or not. What isRead more

The correct answer is the 1. Bank statement and bank column of the cash book, because it will help the business to verify whether amounts entered and entries recorded are correct or not. It will also help in verifying the balances of bank statements and cash books whether they tally or not.

What is Reconciliation?

Reconciliation is an accounting procedure that compares two sets of records to check figures are correct and in agreement. Reconciliation can also be used for personal purposes.

What is a Bank Reconciliation Statement?

A statement showing causes of disagreement between the balance of bank statement and bank column of the cash book at the end of a specific period is called a Bank Reconciliation Statement.

Steps in preparation of Bank Reconciliation Statement

Step 1: Comparing items appearing on the debit and credit sides of the bank statement and bank column of the cash book.

Step 2: Make a list of missed entries.

Step 3: Analyse the causes of differences.

Step 4: Select the date for the preparation of the Bank Reconciliation Statement.

Step 5: Choose the starting point i.e balance as per cash book or balance as per bank statement.

Step 6: Adjust the starting point by adding or subtracting the missed entries.

Step 7: Bank Statement must match with the cash book.

To prepare a bank reconciliation statement a business will need a bank statement from its bank and cash book which it prepares to record entries.

See less

Specimen of Ledger account This is the specimen of a ledger account. J.F. here represents the journal folio. A Ledger account is an account that consists of all the business transactions that take place during the current financial year. For Example, cash, bank, machinery, A/c receivable account, etRead more

Specimen of Ledger account

This is the specimen of a ledger account. J.F. here represents the journal folio.

A Ledger account is an account that consists of all the business transactions that take place during the current financial year.

For Example, cash, bank, machinery, A/c receivable account, etc.

After the financial data is recorded in the Journal. It is then classified according to the nature of accounts viz. Asset, liability, expenses, revenue, and capital to be posted in the ledger account.

With this head, the identification as to whether the opening balance will come under the debit side or the credit side is done.

The table below would help to understand the concept of opening balance in the ledger.

For further clarification of the concept let me give you a practical example.

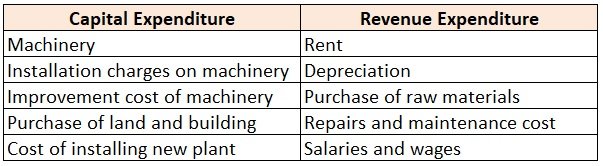

Suppose, a manufacturing firm Amul purchased machinery for, say, Rs 2,50,000. The installation charges were Rs 25,000 and the opening balance of machinery during the year was Rs 5,00,000.

So as the machinery account comes under the category assets, its opening balance would come under the debit side of the ledger account.

And as purchase and installation charges mean expenses for the firm, they would also come under the debit side of the account.

And in case of any sale of a part of the machinery, it would be posted on the credit side of the account as the sales would generate revenue for the firm.

See less