Sundry Debtors in Trial Balance The debtor is a company's asset, and assets are always debited in the trial balance. The trial balance is a statement maintained at the end of an accounting period, listing the ending balances in each general ledger account. There are two sides to this account, debit,Read more

Sundry Debtors in Trial Balance

The debtor is a company’s asset, and assets are always debited in the trial balance.

- The trial balance is a statement maintained at the end of an accounting period, listing the ending balances in each general ledger account.

- There are two sides to this account, debit, and credit and they include all the transactions done in the business over a particular accounting period.

As we know, assets, expenses, and drawings are always debited. That applies not only in journals but here as well, hence, all of your assets are to be debited.

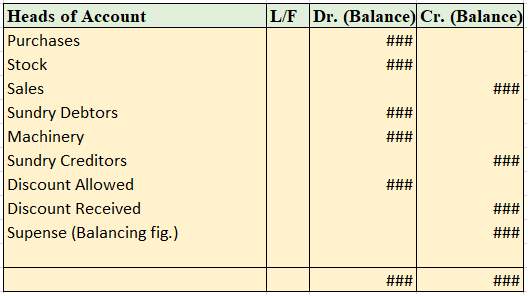

Trial Balance Statement

As we can see here, the sundry debtors (on the 4th) are debited like all the other assets, expenses, and losses. In the end, if the basic accounting equation i.e. assets=capital+liability is violated, a mismatch arises which in the balancing figure is shown under the name of suspense account. Such errors must not be found and corrected to avoid any mismatch in the balance sheet of the company.

Total Assets = Capital + Other Liabilities.

Therefore, this is how the sundry debtors are treated in the Trial Balance.

See less

A cash flow statement presents the changes in the cash and cash equivalents of a business. It classifies the cash flow items into either operating, investing, or financing activities. The cash flow statement provides information about the flow of cash over a period of time. General reserve is a reseRead more

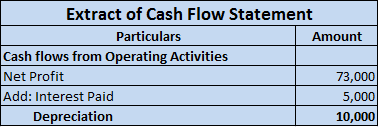

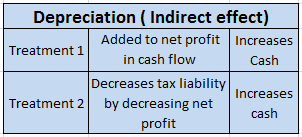

A cash flow statement presents the changes in the cash and cash equivalents of a business. It classifies the cash flow items into either operating, investing, or financing activities. The cash flow statement provides information about the flow of cash over a period of time.

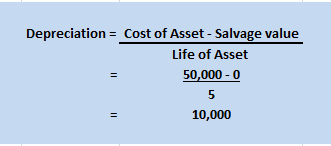

General reserve is a reserve created by taking a portion of the profits for future requirements.

TREATMENT OF GENERAL RESERVE

As per the indirect method, Since there is no actual flow of cash, any addition to reserves is added back to net profit for calculation of net profit before tax and extraordinary items. This net profit before tax will appear under cash flow from operating activities. If there is a reduction in reserve, then they are subtracted from net profit.

As per the Direct method, an increase or decrease in general reserve will not affect the cash flow statement since non-cash items are not recorded. Only cash receipts and payments that come under operating activities are recorded. So, net profit is not shown in the direct method and hence neither is general reserve.

General reserve does not fall under the head investing activities as investing activities involve the acquisition or disposal of long-term assets or investments. They do not fit in financing activities either as financing activities relate to change in capital or borrowings of the company.

EXAMPLE

If the balance in general reserve for the period of March was Rs 4,000 and in April the balance was Rs 7,000, then its treatment in cash flow would be:

See less