A balance sheet is a financial statement that reports the position or value of assets, liabilities and equity at a particular date, which is usually the closing date of a financial year. Formats of balance sheet A balance sheet may be presented in two formats: T-form or Horizontal format This formatRead more

A balance sheet is a financial statement that reports the position or value of assets, liabilities and equity at a particular date, which is usually the closing date of a financial year.

Formats of balance sheet

A balance sheet may be presented in two formats:

T-form or Horizontal format

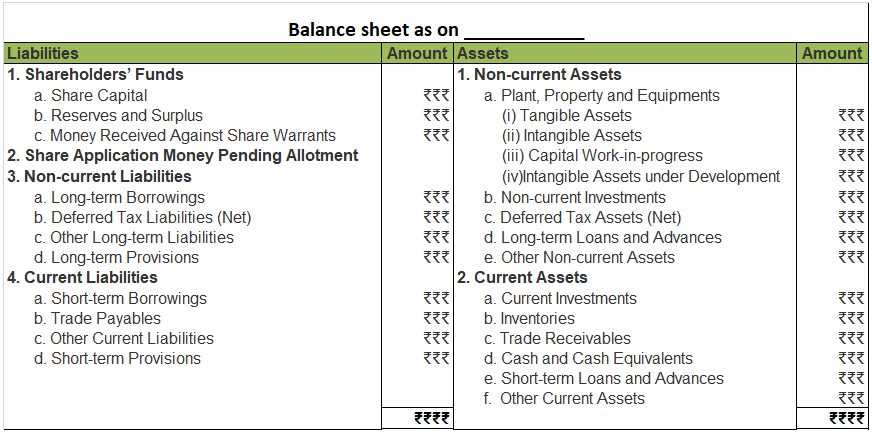

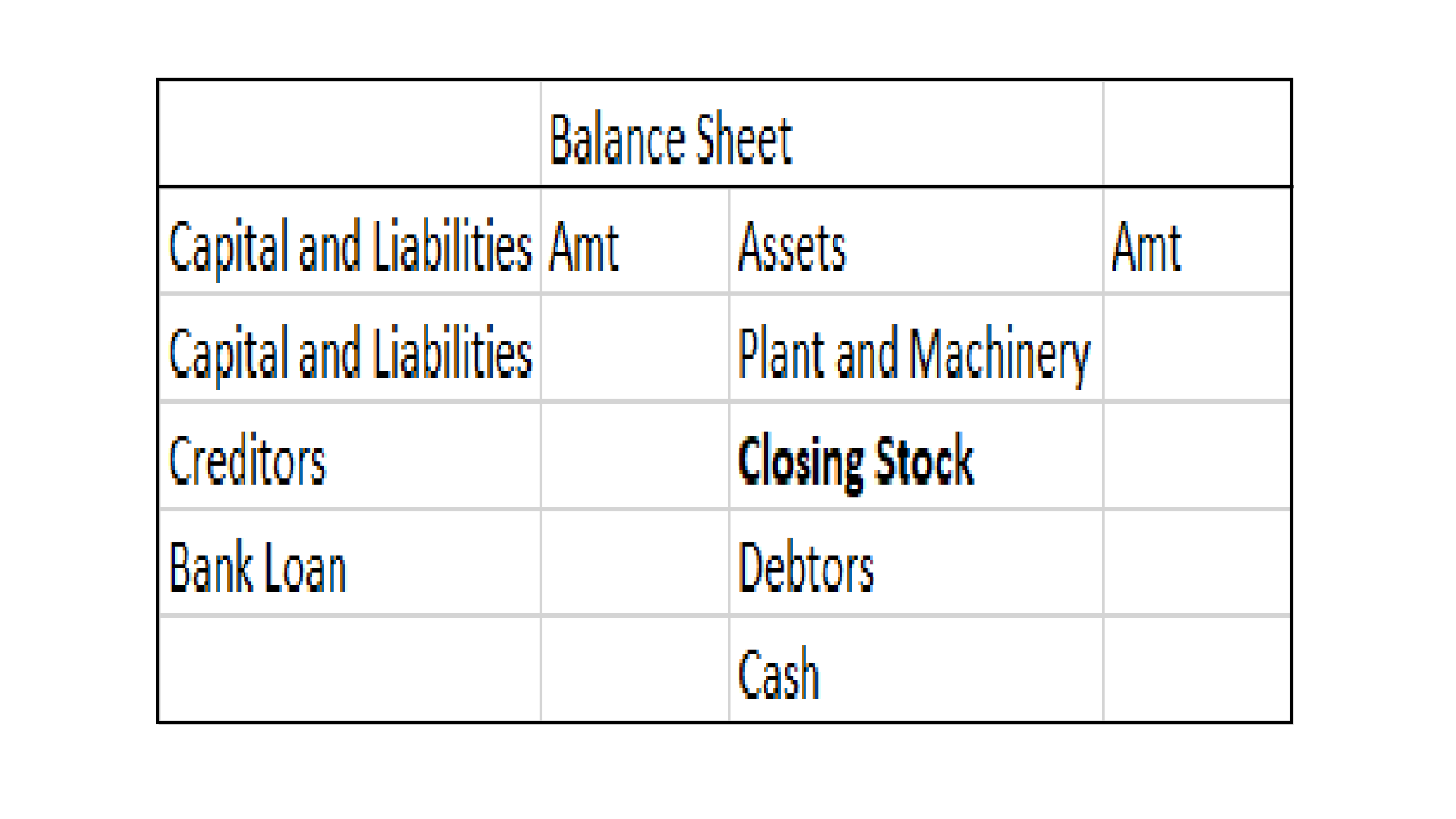

This format is the same as the format of ledger accounts. There are two columns with the headings ‘Liabilities’ for the left column and ‘Assets’ for the right column and columns adjacent to both columns for amounts. The liabilities and equity (capital) are shown on the liabilities side because they both have credit balance and assets are shown on the asset side. Most of the non-corporates prepare their balance as per this format. The T-form balance sheet looks as given below:

Vertical format

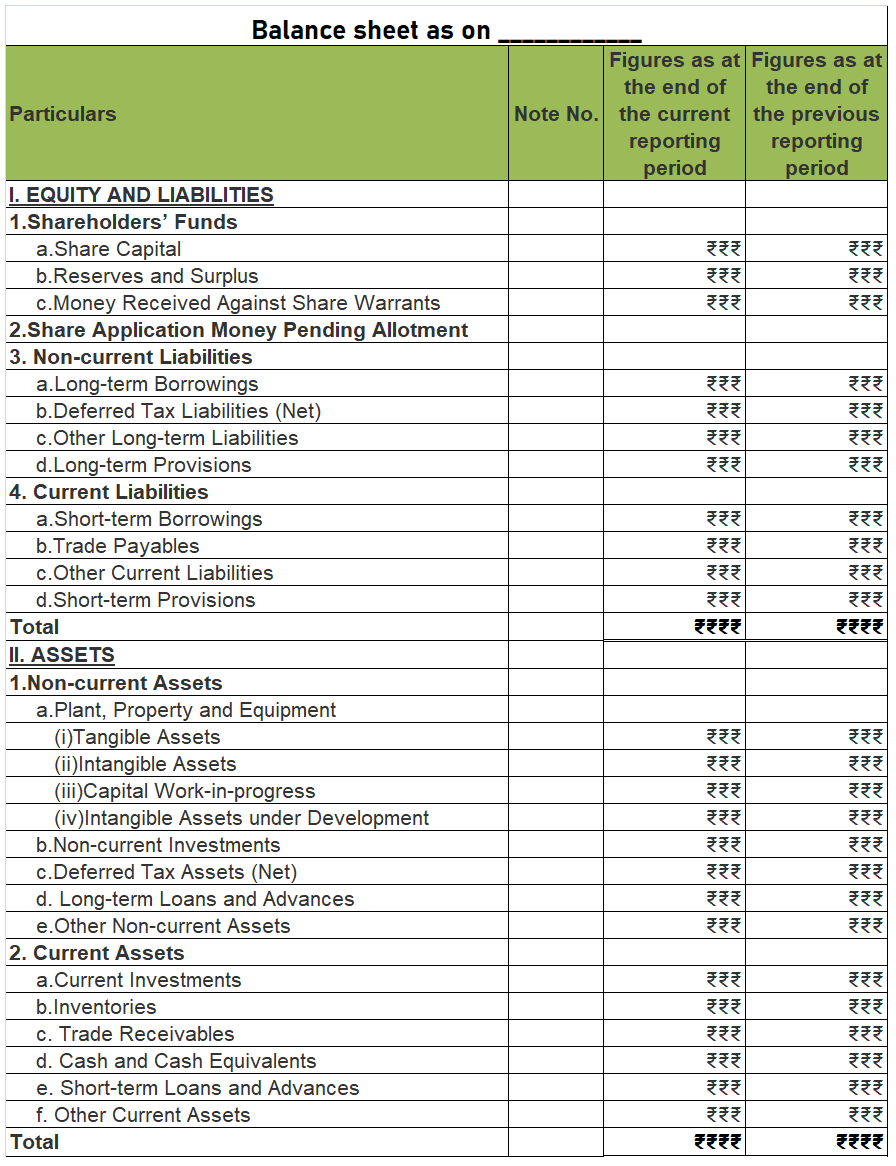

The vertical format of the balance sheet is mostly prepared by corporate entities. Here, the liabilities and assets are shown in the same column as compared to two separate columns in the horizontal format. This results in having a longer shape. Hence, it is called a ‘vertical’ balance sheet. Generally, companies prepare their balance sheet as per this format.

Also, many times, there are two columns for the amount in this format presenting the amount of both the current year and the previous year. This format looks like as given below:

Grouping and marshalling

Beside the structure of the balance sheet i.e. horizontal and vertical, the grouping and marshalling of the items inside the balance sheet are also very important.

Grouping refers to the presenting of similar items under a heading or group. This is done in order to present the balance sheet in a concise manner. This is very important to do. For example, a business can have numerous creditors, but they are all presented under one ‘Creditors’ heading or two or more heading specifying different types of creditors.

The assets of a business are grouped under the heading such as Plant, Property and equipment, Current assets, Non-current investments etc.

Marshalling means the arranging of items as per a particular order. We know that a balance sheet consists of many items and to make the statement more useful and easy to comprehend, the items are arranged in one of the following orders:

- Order of Liquidity: The items which are more liquid i.e which can be easily converted into cash are kept at the top. Like in assets, cash is the most liquid asset and requires no conversion. Then items like current investment, inventories (in case of fast-moving goods) are placed under and so on. At the near bottom, items that require a long time of conversion into cash are placed such as land, plant and machinery.

In case of liabilities, the items which are due for repayment soon are kept at the top, like bank overdraft etc. The items which are due for repayment after a long time or at the time of winding capital are kept at the bottom, like long term loans and capital funds. Given below is a format of horizontal balance sheet in which the items are marshalled in order of liquidity:

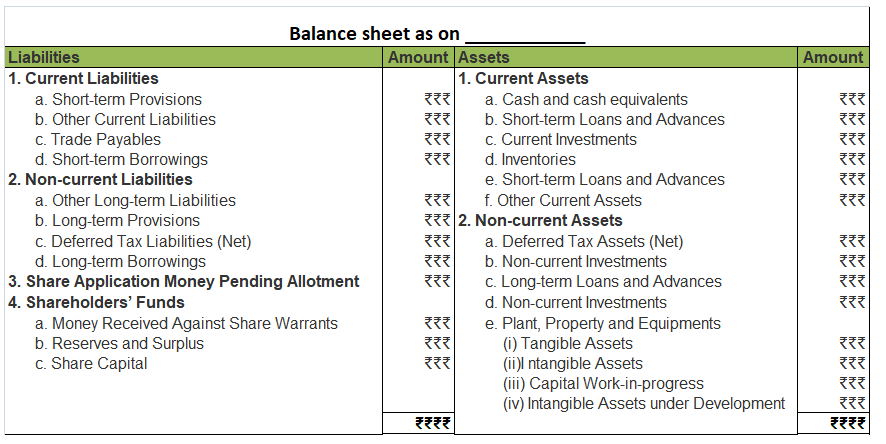

- Order of permanence: This type of arrangement is just the opposite of the order of liquidity. Here the items which are least liquid are placed at the top and the more liquid items are placed at the bottom. Like in the case of assets, cash appears at the bottom and non-current assets at the top. On the liabilities side, equity and non-current liabilities are at the top while current liabilities are at the bottom. Mostly all balance sheets are marshalled in order of permanence.

Financial Reporting is a common practice in accounting where the financial statements of the company are disclosed to present its financial information and performance over a particular period. It is important to know where a company’s money comes from and where it goes. Types of Financial StatementRead more

Financial Reporting is a common practice in accounting where the financial statements of the company are disclosed to present its financial information and performance over a particular period. It is important to know where a company’s money comes from and where it goes.

Types of Financial Statements

There are 4 important types of financial statements such as:

Importance of Financial Reporting

See less