Advantages of Bill of Exchange: Bill of Exchange is generally used as an instrument of credit as it offers many advantages to its users. The advantages are as follows: CONCLUSIVE EVIDENCE: It acts as a shred of conclusive evidence in case of any dispute between the parties like seller-buyer, drawer-Read more

Advantages of Bill of Exchange:

Bill of Exchange is generally used as an instrument of credit as it offers many advantages to its users. The advantages are as follows:

- CONCLUSIVE EVIDENCE: It acts as a shred of conclusive evidence in case of any dispute between the parties like seller-buyer, drawer-drawee, debtors creditors, etc. Issuing the Bill of Exchange binds the party into a legal relationship. It acts as a legal document and proof in a court of law.

- TERMS AND CONDITIONS: When a Bill of Exchange is issued, it mentions all the terms and conditions of payments. The terms and conditions can be like the amount of bill, date of payments, place of payment, interest amount if any, maturity period, etc.

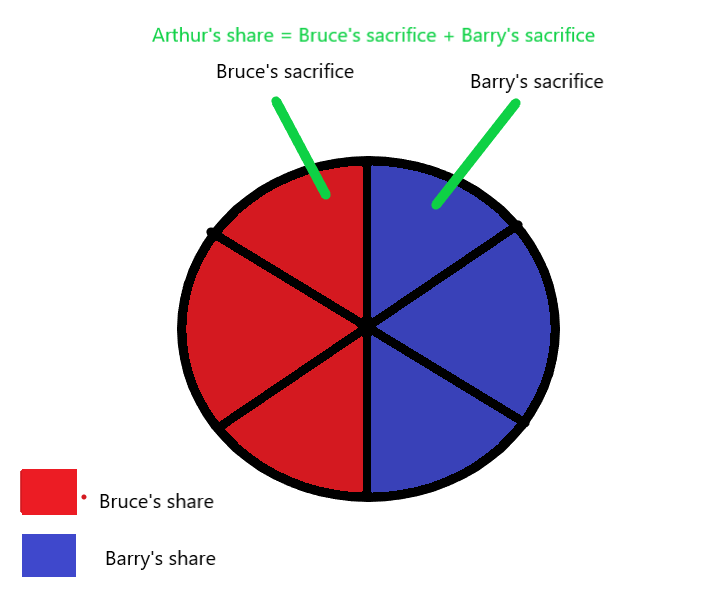

- ACT AS MEANS OF CREDIT: With the help of the Bill of Exchange, buyers can purchase goods on a credit basis and make payment after the credit period expires. If in case of emergency the drawer can also get such Bills discounted before the maturity period.

- WIDER ACCEPTANCE: The Bills of Exchange carries a wide acceptance feature for the parties through which payments can be received and made without any difficulty.

- RELATIONSHIP FRAMEWORK: The Bill of Exchange acts as an instrument that provides a framework enabling the smooth credit transaction between the parties as per the agreement.

- MUTUAL ACCOMMODATION: Sometimes bills are mutually accommodated for the benefit of the parties. The Bill is drawn and accepted by drawer and drawee. Then the same bill is discounted by the drawer and the agreed sum is remitted to the drawee. This is basically done mutually to provide financial help to each other.

The term ‘bad debt’ and ‘write off’ are often used together in a sentence but they have different meanings. First, we will discuss them in brief to understand the differences between them. Bad debts We know, debtors for a business are their assets because the business has the right to receive moneyRead more

The term ‘bad debt’ and ‘write off’ are often used together in a sentence but they have different meanings. First, we will discuss them in brief to understand the differences between them.

Bad debts

We know, debtors for a business are their assets because the business has the right to receive money from the debtors due to the goods supplied to them.

But if due to circumstances, there appears no probability that the amount due to one or more debtors will be realised to the business, then such debts are categorised as bad debts.

In short, bad debts refer to the amount of money that will not be received from some debtors of the business due to some circumstances like insolvency of debtor etc.

Bad debt is deducted from debtors account by the following journal entry:

As bad debts are losses to a business, it is ultimately written off from the profit and loss account.

Write off

In layman terms, write off means to deduct something out from something. In accounting, write off means to deduct or reduce value of assets by crediting it to a liability account which is usually a reserve account or the profit and loss account.

It also refers to the elimination of an item from the books of accounts particularly losses and expenses.

Generally, writing off is associated with the following:

Write off can be done in one of the following methods:

Hence, the following differences can be observed between bad debts and write off or writing off:

See less