Yes, accounting is necessary even for not-for-profit organizations. NPOs or not-for-profit organizations are those that are created for the welfare of the society. They intend to advance some social cause. For example charities, orphanages etc Accounting for NPOs becomes necessary as the trustees ofRead more

Yes, accounting is necessary even for not-for-profit organizations.

NPOs or not-for-profit organizations are those that are created for the welfare of the society. They intend to advance some social cause. For example charities, orphanages etc

Accounting for NPOs becomes necessary as the trustees of these institutions are liable to their members, the donors and the government. They discharge this function with documenting activities of the institution.

What is a not-for-profit organization?

A not-for-profit organization is an entity that undertakes charitable activities. These institutions do not have earning profit as their primary motive. Their focus is on extending social welfare.

Every not-for-profit organization usually has a group of trustees that are responsible for handling all its operations. These trustees are accountable to the members of the NPO.

A not-for-profit organization usually relies on donations and grants as its primary source of revenue. They do not charge the stakeholders to whom they extend their services or goods.

What does accounting for Not-for-profit organizations entail

The professionals undertaking accounting of not-for-profit organizations must have a significant knowledge of statutory provisions and accounting principles. Here is a brief overview of what accounting for a not-for-profit organizations entails

- Ensuring that the institution fulfills all the legal compliances necessary for it to continue functioning as a NPO.

- Documenting all the activities of the institution and ensuring that the NPO has the necessary permits to carry out those activities.

- Accounting for all the revenue receipts and expenses of the institution. The professional must keep in mind that the interests of the members and other stakeholders are not being subjected to any prejudice.

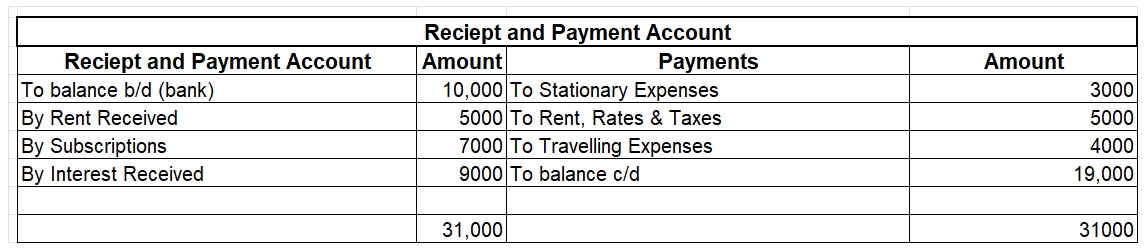

- In India, every NPO has to compulsorily prepare a receipt and payment account, income and expenditure account and a balance sheet. These have to be submitted to the Registrar of Societies before the due dates.

- Every professional undertaking the accounting of a not-for-profit organization must keep in mind that a single non-compliance or partial-compliance can result in the NPO losing out on its tax-exempt status.

- In the past there have been many instances when NPOs have been used for the purpose of money laundering or tax evasion.

- This has resulted in the government making the compliances for these institutions more stringent. The institutions are now required to be more transparent regarding their operations.

We can conclude that accounting is an indispensable requirements for not-for-profit organizations to be able to continue their operations and claim the statutory benefits that the government has extended to them.

See less

By the name, it can be easily deduced that Advance tax means the tax paid in advance. Advance tax is the tax paid by an assessee in the Previous Year itself based on his estimated income. We know that Income tax liability is known in the Assessment Year based on the income of the Previous Year. But,Read more

By the name, it can be easily deduced that Advance tax means the tax paid in advance.

Advance tax is the tax paid by an assessee in the Previous Year itself based on his estimated income.

We know that Income tax liability is known in the Assessment Year based on the income of the Previous Year. But, the government encourages the taxpayers to pay the tax in the Previous Year itself based on the estimated income.

As per section 208 of the Income Tax 1961, if the total income liability on the estimated income comes up more than Rs. 10,000, then advance tax has to be paid.

The advance tax has to be paid according to the following schedule for the individual and corporate assessees [Other than the assessee who computing profits on a presumptive basis under section 44AD(1) and 44ADA(1)]:

Any amount paid by the way of advance tax on or before 15th March shall be treated as advance tax paid during each financial year on or before 15th March.

Also as per section 219, the tax credit is given for the advance tax paid in the regular assessment of income tax.

In case of non-payment or short payment of the advance tax, interest is payable as per section 234B. Interest is also attracted in case of delayed payment of advance tax as per section 234C.

That’s all, I would conclude my answer hoping that it was helpful in making the concept of advance tax easy to grasp.

See less