General reserve is the part of profits or money kept aside to meet future uncertainties and obligations of the entity. General reserve is created out of revenue profits for unspecified purposes and therefore is also a part of free reserves. General reserve forms a part of the Profit & Loss ApprRead more

General reserve is the part of profits or money kept aside to meet future uncertainties and obligations of the entity. General reserve is created out of revenue profits for unspecified purposes and therefore is also a part of free reserves.

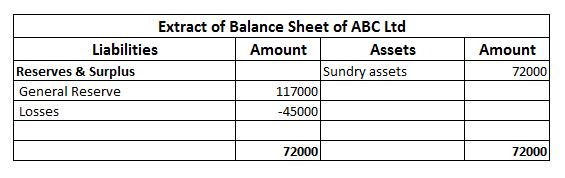

General reserve forms a part of the Profit & Loss Appropriation account and is created to strengthen the financial position of the entity and serves as a sources of internal financing. It is upon the discretion of the management as to how much of a reserve is to be created. No reserve is created when the entity incurs losses.

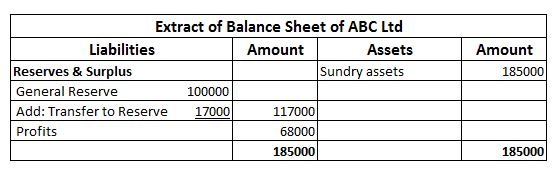

General reserve is shown in the Reserves & Surplus head on the liability side of the balance sheet of the entity and carries a credit balance.

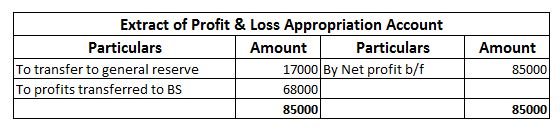

Suppose, an entity, ABC Ltd engaged in the business of electronics earns a profit of 85000 in the current financial year and has an existing general reserve amounting to 100000. The management decides to keep aside 20% of its profits as general reserve.

Then the amount to be transferred to general reserve will be = 85000*20% = 17000.

In the financial statements it will be shown as follows-

Now, in the next financial year, the entity incurs losses amounting to 45000. In this case, no amount shall be transferred to the general reserve of the entity and will be shown in the financial statement as follows-

The creation of general reserve can sometimes be deceiving since it does not show the clear picture of the entity and absorbs losses incurred.

See less

Meaning We know that an account in ledger format has two amount columns i.e. debit and credit amount columns. Now, most of the time, the total of debit and credit sides do not match. The difference between their totals is called the balance of the account and it is posted on the shorter side. ThisRead more

Meaning

We know that an account in ledger format has two amount columns i.e. debit and credit amount columns. Now, most of the time, the total of debit and credit sides do not match. The difference between their totals is called the balance of the account and it is posted on the shorter side. This result in equalling the total of both sides, hence this act is called ‘balancing an account.

Types of balances

Balancing an account is a very usual practice so that the balance of an account can be known. An account can have two types of balances:

The balance of an account is posted on the shorter side. It means:

Example

The following is a cash account that is not balanced:

We can see the debit side is ₹800 more than the credit side. It means there is a debit balance. It will be posted on the credit side as ‘By balance c/d’ to balance the account.

Exceptions

Balance of the income and the expense accounts (nominal accounts)are not computed. Instead, they are closed to trading account or profit and loss account to balance their amount totals. For example, the salaries account and sales accounts

Only the balance of the following types of accounts are computed and carried forwarded to successive accounting years:

The balance of these accounts is shown on the trial balance and balance sheet as well.

See less