Debtors are treated as an asset. A debtor is a person or an entity who owes an amount to an enterprise against credit sales of goods and/or services rendered. When goods are sold to a person on credit that person is called a debtor because he owes that much amount to the enterprise. Debtors are consRead more

Debtors are treated as an asset.

A debtor is a person or an entity who owes an amount to an enterprise against credit sales of goods and/or services rendered.

When goods are sold to a person on credit that person is called a debtor because he owes that much amount to the enterprise.

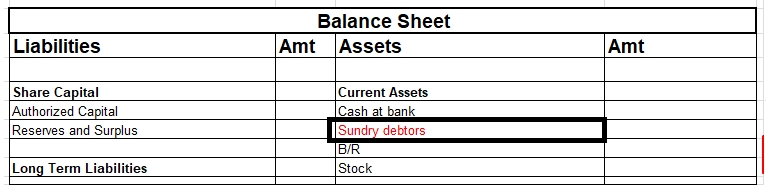

Debtors are considered assets in the balance sheet and are shown under the head of current assets.

For example – Ram Sold goods to Sam on credit, Sam did not pay for the goods immediately, so here Sam is the debtor for Ram because he owes the amount to Ram. This amount will be payable at a later date.

Liabilities Vs Assets

Liabilities

It means the amount owed (payable) by the business. Liability towards the owners ( proprietor or partners ) of the business is termed internal liability. For example, owner’s capital, etc

On the other hand, liability towards outsiders, i.e., other than owners ( proprietors or partners ) is termed as an external liability.

For example creditors, bank overdrafts, etc.

Assets

An asset is a resource owned or controlled by a company. The benefit from the asset will accrue to the business in current and future periods. In other words, it’s something that a company owns or controls and can use to generate profits today and in the future.

For example – machinery, building, etc.

Current assets are defined as cash and other assets that are expected to be converted into cash or consumed in the production of goods or rendering of services in the normal course of business. They are readily realizable into cash.

In other words, we can say that the expected realization period of current assets is less than the operating cycle period.

For example, goods are purchased with the purpose to resell and earn a profit, debtors exist to convert them into cash i.e., receive the amount from them, bills receivable exist again for receiving cash against it, etc.

Why debtors are treated as assets?

Now let me explain to you why debtors are treated as assets and not as liabilities because of the following characteristics :

- We can say that the expected realization period is less than the operating cycle period.

- Expected to be converted into cash in the normal course of business.

- In the business, debtors are treated as current assets which we can see on the asset side of the balance sheet.

- Debtors have a debit balance.

Conclusion

Now after the above discussion, I can conclude that debtors are considered to be an asset and not a liability.

See less

Yes, the account receivable is a sub ledger account. It is an account that is used to record the payment history of each and every customer to whom the business has sold goods or provided services on credit. Accounts receivable represent the amount that the customers owe to the business with respectRead more

Yes, the account receivable is a sub ledger account. It is an account that is used to record the payment history of each and every customer to whom the business has sold goods or provided services on credit.

Accounts receivable represent the amount that the customers owe to the business with respect to the goods sold or services provided to them on credit. They are also known as trade receivable or debtors.

The accounts receivable subledger shows various details of every transaction like the invoice number, amount due, date of payment, discount allowed etc. The subledger accounts are also known as the subsidiary accounts.

Difference between general ledger and subledger accounts

Here is a list of the major differences between sub-ledgers and the general ledger:

Importance/ use of Subsidiary Account

The usefulness of an accounts receivable sub ledger account lies in the fact that it provides detailed information about the money different customers owe to the business.

For example, the general ledger account may show that the total balance of trade receivable is 1 lakh without indicating the individual amount that each customer owes to the business. The subsidiary account can help us by showing that customer A owes 50000 rupees, customer B owes 30000 rupees while customer C owes 20000 rupees.

In short, the subsidiary accounts provide detailed information about each and every transaction. They help us to find useful information quickly and easily. They help us analyze the business policies and take corrective actions.

Thus, we can conclude that accounts receivable is a subledger account that provides us detailed information about the various credit transactions and the amount that each customer owes to the business. It helps us analyze our credit policies and take corrective actions. It helps us identify and classify bad debts as such on

See less