No, Goodwill cannot be called a fictitious asset. A fictitious asset does not have any physical existence or realizable value. Although it is recorded in the assets column, it is not really an asset, rather it is an expense that is incurred during the accounting period. Its benefit, however, is realRead more

No, Goodwill cannot be called a fictitious asset.

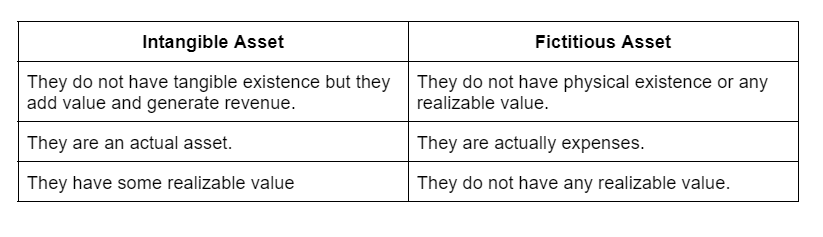

A fictitious asset does not have any physical existence or realizable value. Although it is recorded in the assets column, it is not really an asset, rather it is an expense that is incurred during the accounting period. Its benefit, however, is realized for extended periods. This is why they are recorded as assets. They are recorded in a single year and are amortized over the years. A fictitious asset is neither tangible nor intangible.

Examples of Fictitious Assets

- Preliminary expenses

- Promotional expenses

- Discount on issue of shares/debentures etc.

Now, goodwill is an intangible asset that relates to the purchase of a company. It is the amount that a company pays over the net worth of the company being purchased. This can be because of its brand value, good customer base, etc. As a company’s reputation improves, its goodwill increases accordingly. Therefore, It does not have a tangible existence but it does have a monetary value. They are also recorded on the asset side of the balance sheet under the head “Intangible assets”.

Reason for not being a fictitious asset

Since goodwill is an asset and not an expense, it cannot be called a fictitious asset. Moreover, goodwill has a realizable value. Unlike fictitious assets, goodwill can be purchased or sold. Therefore, goodwill is termed as an intangible asset but not a fictitious asset. The major difference between an intangible asset and a fictitious asset is:

Sales return shows the sale price of goods returned by customers. It is deducted from sales or gross sales in the income statement. It is a contra revenue account that represents returns from the customers and deductions to the original selling price, in case of any defective product received by theRead more

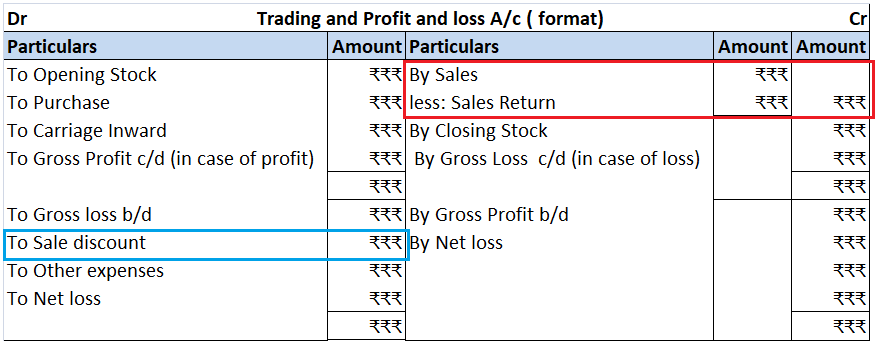

Sales return shows the sale price of goods returned by customers. It is deducted from sales or gross sales in the income statement.

It is a contra revenue account that represents returns from the customers and deductions to the original selling price, in case of any defective product received by the customer or any other manufacturing default.

Sales allowances arise when any customer accepts the product at a lower price than the original price or, in other words, a reduction in the price charged by a seller, due to any problem related to the sold product like a quality issue, an incorrect price charged or shipment issue.

Sales allowances are created before the final billing is paid by the buyer.

Journal entry for sales return and allowances:

See less