The correct option is 3.) The term current assets do not include furniture. Explanation A current asset is any asset that can reasonably be expected to be sold, consumed, or exhausted through the normal operations of a business within one accounting year. Thus, current assets don't have life for morRead more

The correct option is 3.)

The term current assets do not include furniture.

Explanation

A current asset is any asset that can reasonably be expected to be sold, consumed, or exhausted through the normal operations of a business within one accounting year. Thus, current assets don’t have life for more than a year.

Example: Cash and cash equivalent, stock, liquid assets, etc.

Furniture is expected to have a useful life for more than a year and they are bought for a long term by a company.

Cash is a more liquid asset of a company making it a more “current” asset. It requires no conversion and is spendable as it is. Thus, making it a vital current asset.

Stock in trade is a current asset because it can be converted into cash within one year and all the stock in trade of a company is expected to be sold within one accounting period and should not stick for a longer period.

Advance payment, on the other hand, is an amount paid to an employee, essentially a short-term loan by the employer. It’s recorded on the asset side of the balance sheet and as these assets are used, they are expended and recorded on the income statement for the period in which they are incurred, making it a short-term asset ending within an accounting year.

Thus, on the asset side of the balance sheet, we can clearly see which current assets are and which are not included in the current asset

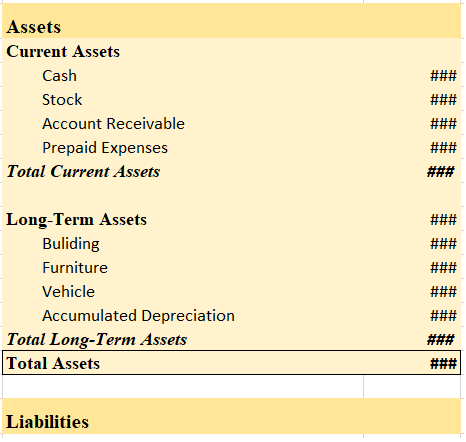

Balance Sheet (As at…..)

Therefore, (3) Furniture, won’t be included in current assets.

See less

Introduction In GST, a supply is a taxable event. This means whenever there is a supply of goods or services or both, GST is charged. Supply includes the exchange of goods or services between supplier and recipient by way of sale, barter, lease etc for consideration and in the course or furtheranceRead more

Introduction

In GST, a supply is a taxable event. This means whenever there is a supply of goods or services or both, GST is charged. Supply includes the exchange of goods or services between supplier and recipient by way of sale, barter, lease etc for consideration and in the course or furtherance of business. The rate of GST on any supply depends on the type of good or service supplied.

Composite supply and mixed supply are two special types of supplies, in which two or more goods or services or both are offered together in a bundle. As two or more goods are supplied together, the question arises at which rate the GST is to be charged on such supplies as such goods or services may have different rates of GST applicable to them. Sections 8 of the CGST act, 2017 deals with the tax liability of such supplies.

Composite supply

A composite supply is a type of supply in which two or more goods or services or both are supplied together in the ordinary course of business. Such goods or services are natural bundles. By natural bundle, we mean the goods or services are complementary to each, they are naturally provided together and are to be used along with each other.

For example, mobile phones and chargers are supplied as a bundle. This concept of the natural bundle is the main determiner of a composite supply.

In such supplies, there is one main product which is called the principal supply. Like in the above example, the mobile phone is the principal supply. Other goods or services are dependent on the principal supply.

A composite supply will be taxable as the rate of GST applicable on the principal supply.

For example, suppose the rate of GST on mobile phones is 18% and that on the charger is 12%, then the whole supply will be taxable at the rate of 18%.

Mixed supply

A mixed supply is a type of supply in which two or more goods or services or both are supplied together but they do not complement each other and are not a natural bundle. They are not supplied in the ordinary course of business, For example, a combo of bottled honey and face cream.

In mixed supply, the good or service which attracts the highest rate of GST is considered the rate of supply for the whole supply.

For example, suppose bottled honey attracts 5% GST and face cream 18% GST, then the whole supply will be charged 18% GST.

See less