Fluctuating Capital Fluctuating capital is a capital that is unstable and keeps changing frequently. In the fluctuating capital, the capital of each partner changes from time to time. In partnership firms, each partner will have a separate capital account. Any additional capital introduced during thRead more

Fluctuating Capital

Fluctuating capital is a capital that is unstable and keeps changing frequently. In the fluctuating capital, the capital of each partner changes from time to time. In partnership firms, each partner will have a separate capital account. Any additional capital introduced during the year will also be credited to their capital account. In the fluctuating capital method, only one capital a/c is maintained i.e no current accounts like in the fixed capital a/c method. Therefore, all the adjustments like interest on capital, drawings, etc. are completed in the capital a/c itself.

It is most commonly seen in partnership firms and it is not essential to mention the Fluctuating Account Method in the partnership deed.

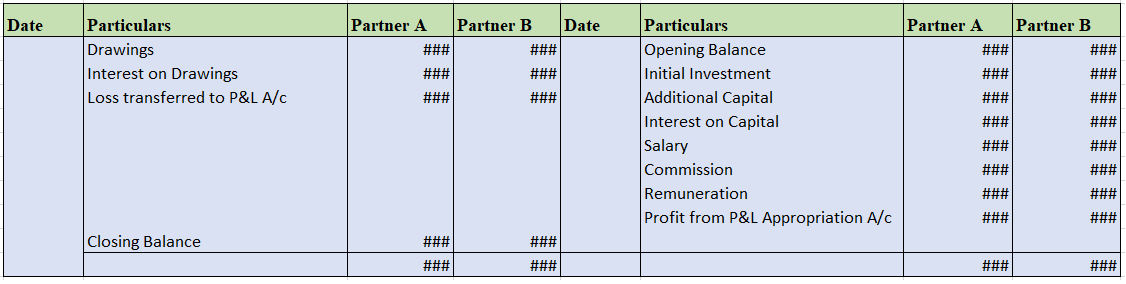

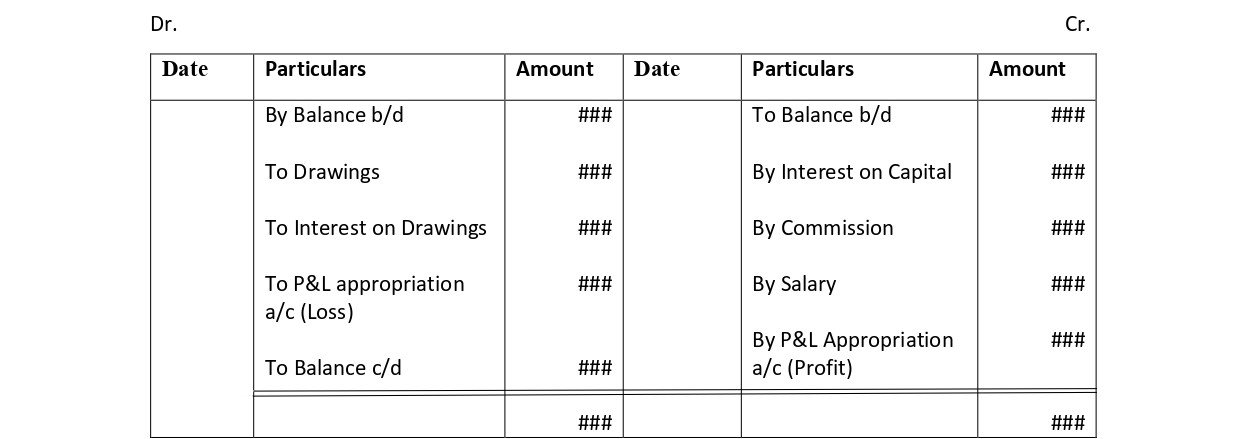

- All the adjustments resulting in a decrease in the capital will be debited to the partner’s capital, such as drawings made by each partner, interest on drawings, and share of loss.

- Similarly, the activities or adjustments that lead to an increase in the capital are credited to the partner’s capital account, such as interest on capital, salary, the share of profit, and so on.

Fluctuating Capital Account Format

See less

Meaning of Working Capital Firstly, let’s understand the meaning of the working capital. Working capital is the factor which demonstrates the liquidity position of the business to carry out day to day operations. It majorly includes cash & bank balances and liquid assets. Managing working capitaRead more

Meaning of Working Capital

Firstly, let’s understand the meaning of the working capital. Working capital is the factor which demonstrates the liquidity position of the business to carry out day to day operations. It majorly includes cash & bank balances and liquid assets.

Managing working capital is a crucial process to maintain short term liquidity and so ultimately resulting into achieving long term objectives efficiently. Working capital can be calculated by deducting business’s current liabilities from current assets.

To achieve the ideal working capital requirement for any business, it is important to understand various types of working capital and various ways to manage it.

Coming to Permanent Working Capital, also called as Fixed Working Capital, it is the minimum working capital required or maintained by businesses. Such type of working capital is maintained to take care of regular financial obligations like creditors, inventory, salaries etc.

Irrespective of scale of operations carried out in business, Permanent Capital is maintained by businesses which can be in form of Net Working Capital.

There is no specific formula for calculating Fixed Working Capital, it completely depends upon the business’s assets and liabilities. So accordingly, it can be estimated through the balance sheet of the business.

For calculating Permanent Working Capital, you can follow below steps:

The requirement of Permanent Working Capital changes as the business expands. It is crucial to make sure that the working capital level does not fall below the Permanent Working Capital requirement.

Types of Permanent Working Capital:

Permanent working capital is further divided into two types:

- Regular working capital – This refers to capital required to maintain healthy cashflow for purchases of raw materials, payment of wages etc.

- Reserve working capital – This refers to amount which is more than regular working capital to take care of unexpected business expenses due to contingent events.

See less