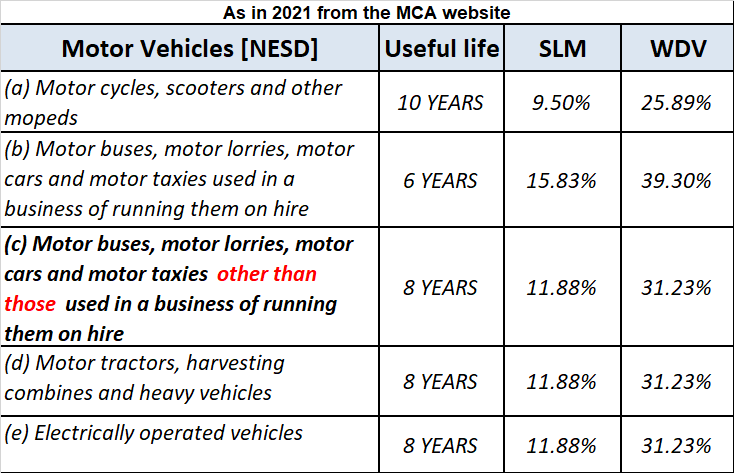

As per the companies act 2013, the rate of depreciation for cars/vehicles and their useful life is mentioned below They are categorized by the companies act as follows: when these car/ motor vehicles are owned with no intention to sell within the accounting period and are generally used to generateRead more

As per the companies act 2013, the rate of depreciation for cars/vehicles and their useful life is mentioned below

They are categorized by the companies act as follows:

- when these car/ motor vehicles are owned with no intention to sell within the accounting period and are generally used to generate revenue. For example, giving cars/motor vehicles on lease or hire purpose.

- cars/motor vehicles when used for purposes other than the business of hire. For example, a car is owned for official use.

Car/motor vehicles are considered as fixed tangible assets. Treatment of these cars/ motor vehicles is similar to those of other fixed assets. The depreciation will be shown as an expense in the profit and loss account and also the value of these assets will be adjusted in the balance sheet.

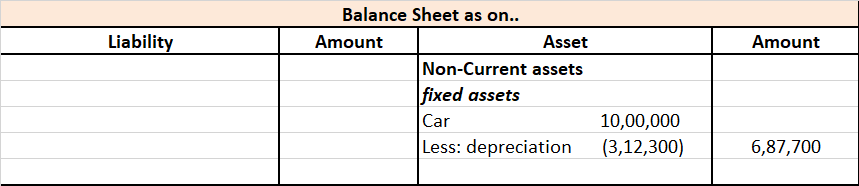

Explaining with a simple example: Mars.Ltd purchased a car for Rs 10,00,000, and use it for its official purpose. Its useful life as per act is taken as 6 years and the rate of depreciation as 31.23% as per the WDV method.

Therefore depreciation as per WDV is calculated as follows

Cost of car = Rs 10,00,000

Residual value = NIL

Rate of depreciation = 31.23%

depreciation for first-year = Rs (10,00,000 – NIL)*31.23%

= Rs 3,12,300

Calculated depreciation on this car will be shown in the profit and loss account as an expense and the same will be treated under the balance sheet every year. Here is the extract of profit and loss and the balance sheet for the above example.

Let me brief you about the nature of computers, their parts, laptops according to the companies act 2013. Basically, these are treated as non-current tangible fixed assets. This is because these types of equipment are used in business to generate revenue over its useful life for more than a year. AsRead more

Let me brief you about the nature of computers, their parts, laptops according to the companies act 2013. Basically, these are treated as non-current tangible fixed assets. This is because these types of equipment are used in business to generate revenue over its useful life for more than a year. As per the companies act 2013, the following extract of the depreciation rate chart is given for computers.

Giving you a short example, suppose M/s spy Ltd purchased 20 computers worth Rs 30000 each. As per the companies act 2013, the computer’s useful life is taken to be 3 years, and the rate of depreciation rate is 63.16%. Applying the WDV method we can calculate depreciation as follows:

So for the first year, the depreciation amount will be

Cost of computers = Rs 6,00,000 (20*30000)

Salvage value = NIL

Rate of depreciation as per the Act = 63.16%

Therefore depreciation = (6,00,000 – NIL)* 63.16%

= Rs 3,78,960

this amount of depreciation will be shown in the profit & loss account as depreciation charged to computers and the same will be adjusted in the balance sheet. The extract of Profit & Loss and corresponding year Balance sheet is shown below.

See less