Let us begin with a short explanation of what opening balance is: The opening balance is the amount of funds that are bought forward from the end of one accounting period to the beginning of a new accounting period. In a firm’s account, the first entry done is of the opening balance. It can either hRead more

Let us begin with a short explanation of what opening balance is:

The opening balance is the amount of funds that are bought forward from the end of one accounting period to the beginning of a new accounting period.

In a firm’s account, the first entry done is of the opening balance. It can either have a debit balance or a credit balance depending upon whether the firm has a negative or positive balance.

Opening balance of a ledger

Opening balance is the first entry of the ledger account at the beginning of an accounting period.

In the case of a newly started business, there will be no closing balances and as such there will be no balances to be carried forward. In such a case, the investment and capital of the business will be entered as an opening balance for the current accounting period.

So the first and foremost part is to identify on which side of the ledger i.e. the debit side or the credit side the opening balance is to be entered.

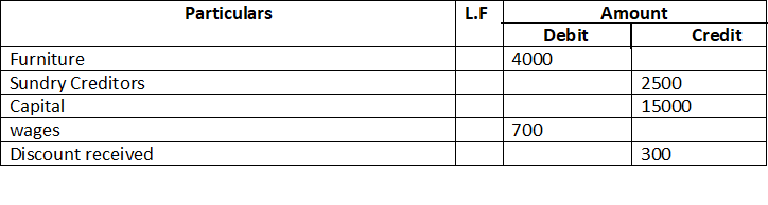

For Example, A trial balance is given which represents the debit and credit balances, accordingly, I will prepare different ledger accounts to make it simpler.

The trial balance shows the opening balance of various accounts. Now posting them in ledger accounts.

The trial balance shows the opening balance of various accounts. Now posting them in ledger accounts.

As the Furniture is an Asset account, the opening balance will be on the debit side of the ledger account.

As Sundry creditor is a credit account, we put the opening balance on the credit side.

As the Capital is a credit account, we put the opening balance on the credit side.

As Wages is a debit account, we put the opening balance on the debit side.

As the Discount received is a credit account, we put the opening balance on the credit side.

Exception

Drawing Account.

Drawing account is an exception to this topic. It is considered a contra account to the owner’s capital account because it reduces the value of the owner’s equity. Drawings, therefore, have no opening balance.

Contra Entry.

Contra entry involves transactions of cash and bank. Any entry which involves both the cash and bank is contra entry.

For example, we deposit cash 5000 into the bank.

Accounting entry for this transaction would be

In this case, the ledger entry would be

As the bank account has a debit balance, the opening balance would come on the debit side.

As the cash account has a credit balance, the opening balance would come on the credit side.

Alternatively, If we withdraw cash 5000 from the bank.

Accounting entry would be

In this case, the ledger entry would be

As the Cash account has a debit balance, the opening balance would come on the debit side.

As the Bank account has a credit balance, the opening balance would come on the credit side.

See less

To understand the accounting treatment of fixed assets under IFRS let us first understand what fixed assets are. What are Fixed Assets? Fixed assets are the assets that are purchased for long-term use by a business and not for resale. Some examples of fixed assets are land, buildings, machinery, furRead more

To understand the accounting treatment of fixed assets under IFRS let us first understand what fixed assets are.

What are Fixed Assets?

Fixed assets are the assets that are purchased for long-term use by a business and not for resale. Some examples of fixed assets are land, buildings, machinery, furniture and fixtures, etc.

Fixed assets are essential for the smooth operations of the business. It often shows the value of the business. The value of fixed assets usually decreases with time, obsolescence, damage, etc.

As per IAS-16 Property, Plant and Equipment, an asset is identified as a fixed asset if it satisfies the following conditions:

What is IFRS?

IFRS stands for International Financial Reporting Standards. It provides a set of standards to be followed globally by all companies to ensure transparency, comparability, and consistency.

What is the accounting treatment of fixed assets under IFRS?

Under IFRS, the first step is to measure the value of the fixed assets on cost. The cost of the fixed assets includes the following:

After this step, the entity may choose any one of the following two primary methods:

For example, a company bought a piece of machinery for 60,000. 5,000 were spent on its installation. It has a useful life of 10 years. The machinery would be depreciated over its useful life of 10 years based on its cost which is 65,000.

2. Revaluation model: As per this model, the fixed assets are valued on their fair value, as on the revaluation date. The amount of depreciation and impairment losses is subtracted from the fair value.

If the value of an asset increases, the gain goes to equity (revaluation surplus) unless it can be set off with a past loss recorded in profit or loss.

On the other hand, if the value decreases, the loss goes to profit or loss unless it offsets a past surplus in equity.

For example, a building was purchased for 100,000. On the revaluation date, the fair value of this building was 150,000. Hence, there is a revaluation surplus of 50,000 which shall be credited to the revaluation surplus account.

Impact on Financial Statements

Fixed assets are shown on the Assets side of the Balance Sheet.

Conclusion

From the above discussion, it may be concluded that:

See less