Sundry Debtors Sundry Debtors are those persons or firms to whom goods have been sold or services rendered on credit and the payment has not been received from them. In other words, Debtors are the persons or firms from whom the payment is to be received by the business. For Example, Ramen Sold goodRead more

Sundry Debtors

Sundry Debtors are those persons or firms to whom goods have been sold or services rendered on credit and the payment has not been received from them. In other words, Debtors are the persons or firms from whom the payment is to be received by the business.

For Example, Ramen Sold goods to Sam on credit, Sam did not pay for the goods immediately, so here Sam is the debtor for Ramen because he owes the amount to Ramen.

Another Example, If goods worth Rs 7000 have been sold to Sid on credit, he will continue to remain as debtor of the business so long as he does not make the full payment.

Treatment:

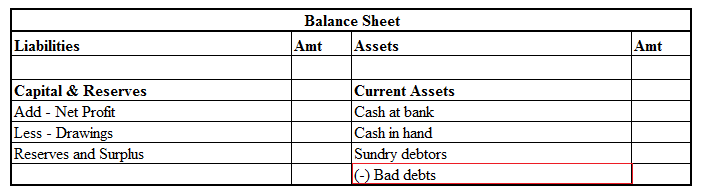

Sundry Debtor is considered as a current asset and hence it is shown on the assets side of the balance sheet under the Current Assets heading.

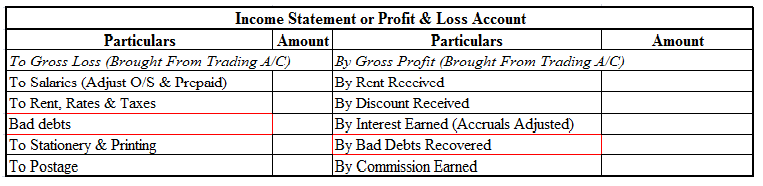

Sundry Debtors are not considered as an item of profit and loss because it is not considered as an item of income or expense. However, the items associated with sundry debtors such as bad debts or provision for doubtful debts or bad debts recovered are shown in profit and loss accounts in the debit and credit sides respectively.

Sundry Creditors

Sundry creditors are those persons or firms from whom goods have been purchased or services rendered on credit and for which payment has not been made. In other words, Creditors are the person or firms to whom some money has to be paid by the business.

For Example, Ramen purchased goods from Sam on credit, Ramen did not pay for the goods immediately, so here Ramen is the creditor for Sam because he owes money to Sam.

Another Example, If Mr. Johnson purchased goods worth Rs 3000 from M/s. Rick & Co. on credit, Mr. Johnson will continue to remain as a creditor of M/s. Rick & Co. as long as the full payment is made by Mr. Johnson.

Treatment:

Sundry Creditor is shown in the liabilities side of the balance sheet under the heading Current Liabilities.

See less

Ledger posting The process of entering all transactions from journal to ledger is called ledger posting. Each ledger account contains an individual asset, person, revenue, or expense. As we're aware the journal records all the transactions of the business. Posting to the ledger account not only helpRead more

Ledger posting

The process of entering all transactions from journal to ledger is called ledger posting. Each ledger account contains an individual asset, person, revenue, or expense. As we’re aware the journal records all the transactions of the business.

Posting to the ledger account not only helps the proper maintenance of the ledger book but also helps in reflecting a permanent summary of all the journal accounts. In the end, all the accounts that are entered and operated in the ledger are closed, totaled, and balanced.

Balancing the ledger means finding the difference between the debit and credit amounts of a particular account, it’s done on the day of closing of the accounting year. Sometimes journal entries are made and maintained monthly. Therefore, the balancing of the ledger’s date depends on the business’ closing date and the way a business maintains its books of accounts.

Example

Mr. Jack Sparrow decided to start a new clothing business. On 1st April 2021, He started the business with a total sum of $100,000 cash. He purchased furniture, including desks and shelves for $25,000. Mr. Sparrow then decided to start with women’s clothing and purchased a complete range of clothes from the wholesale market for $50,000. On the next day, he sold all the stock for $75,000. He also hired a worker for $5,000.

We need to journalize these transactions and post them into the ledger account.

Journal Entries

Ledger Accounts

Cash A/c

Capital A/c

Purchases A/c

Sales A/c

Salary A/c

See less