Introduction First, we should know what Earnings per share is. Earnings per share or EPS is the earnings available to each equity share of a company. The general formula of Earning per share is as follows: Earnings per share indicate the profit-generating capability of an enterprise and potential inRead more

Introduction

First, we should know what Earnings per share is.

Earnings per share or EPS is the earnings available to each equity share of a company. The general formula of Earning per share is as follows:

Earnings per share indicate the profit-generating capability of an enterprise and potential investors often compare the EPS of different companies to choose the best investment alternative.

Earnings per share indicate the profit-generating capability of an enterprise and potential investors often compare the EPS of different companies to choose the best investment alternative.

It is shown at the bottom of the Statement of profit and loss of a company.

Basic Earnings per share

As per AS-20, there are two types of EPS.

- Basic EPS

- Diluted EPS

Basic Earnings per share has the same meaning as given above. But the formula of basic earnings per share as per AS-20 is as follows:

The formula of basic earnings per share is slightly different from the general formula of EPS. Here the numerator is the same as discussed above. But the denominator is different.

Here it is ‘Weight average number of equity shares outstanding’ instead of ‘Total number of equity shares outstanding.

The two components of the formula are discussed below:

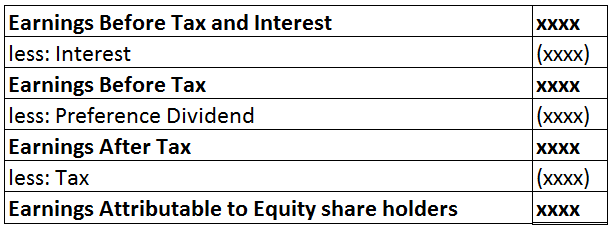

Meaning of earnings available to equity shareholders

The earnings or net profit which remains after deduction of interest payable, preference dividend, if any, and tax is known as earnings available to equity shareholders. It is calculated as shown below:

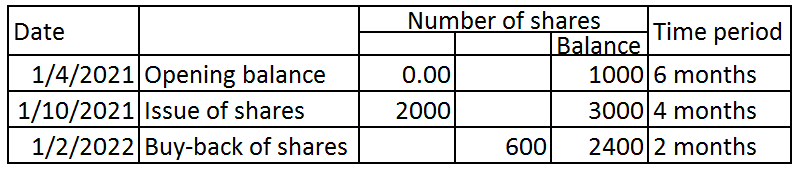

Weighted average number of equity shares outstanding

The weighted average will be calculated by applying the weight of the time period for which the numbers of shares were outstanding. Let’s see a simple case to understand the calculation of the weighted average number of equity shares outstanding:

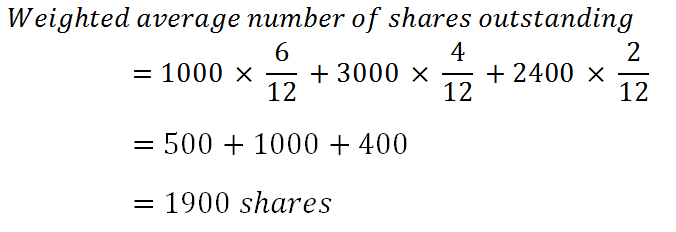

Solution:

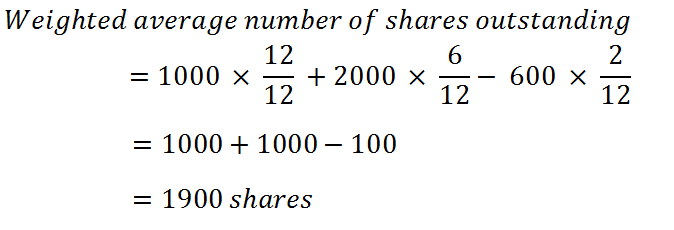

Alternative way:

The calculation of the weighted average number of equity shares is different in special cases like:

- party paid-up shares

- bonus shares and

- right issue shares

Partly paid-up shares

Partly paid-up shares are not considered in the above calculation unless they are eligible to take part in dividends. In that case, such partly paid-up shares are included in the calculation as fractional shares.

For example, 300 equity shares of Rs. 10 each and Rs. 5 paid up will be considered as 150 shares. (300 x 5/10)

Bonus shares

We know bonus shares are issued at no cost to the shareholders. Issue of bonus shares leads to an increase in the number of equity shares without an increase in the resources.

AS-20 tells us to make adjustments to the number of shares outstanding before the issue of bonus shares as if the bonus shares were issued at the beginning of the earliest reported period. The effect will be retrospective.

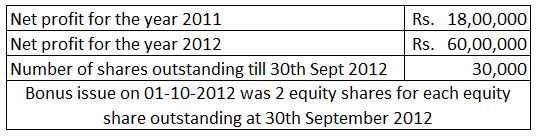

Take the following example:

Here, number of bonus shares = 30,000 x 2 = 60,000

Therefore, EPS for 2012 = 60,00,000 /(30,000 + 60,000)= Rs. 6.67

As the earliest report period is 2011, its EPS will also have to be adjusted. Bonus issue will be treated as if it had occurred at the beginning of the earliest reported period.

Adjusted EPS for 2011= 18,00,000 / (30,000 + 60,000) = Rs. 20

Right issue

The right issue generally has an exercise price that is less than the fair value of the shares. Hence, we can say that the right issue has an element of bonus in them.

So, just like in the case of a bonus issue, we will have to adjust the number of shares outstanding before the right issue up to the earliest reported period by an adjustment factor.

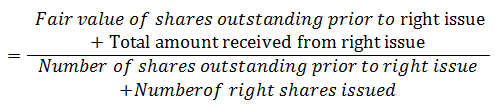

The number of shares outstanding before the right issue is to be multiplied by the adjustment factor given below:

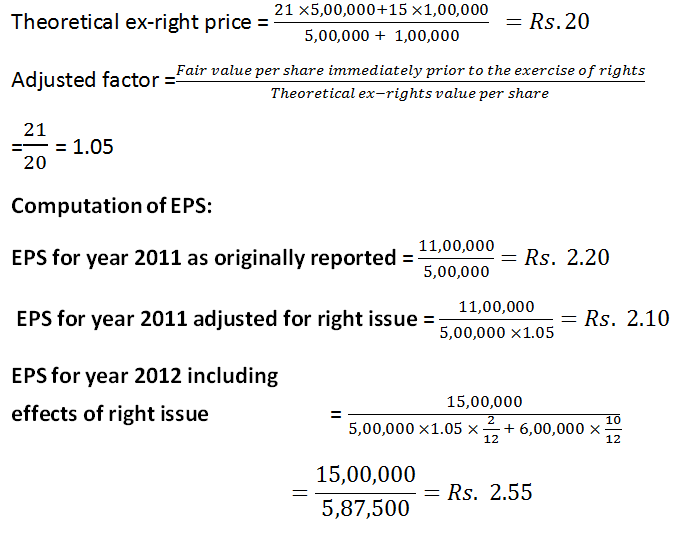

Theoretical ex-right value per share is calculated in the following way:

Let’s see an example:

Net profit for 2011 Rs. 11,00,000

Net profit for 2012 Rs. 15,00,000

No. of shares outstanding prior to rights issue 5,00,000 shares

Rights issue price Rs. 15

Last date to exercise rights 1st March 2012

The right issue is one new share for every 5 shares outstanding (i.e. 1,00,000 new shares)

The fair value of shares immediately prior to 1st March 2012 = Rs. 21

Solution:

See less

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization's activities. For example - Tax Authorities, Banks, Customers, Trade Unions, Government, Investors,Read more

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization’s activities.

For example – Tax Authorities, Banks, Customers, Trade Unions, Government, Investors, or Creditors.

External Users:

Here is a summary of external users

See less