Ledger Folio A ledger folio, in simple words, is a page number of the ledger account where the relevant account appears. The term 'folio' refers to a book, particularly a book with large sheets of paper. In accounting, it's used to maintain ledger accounts. The use of ledger folio is generally seenRead more

Ledger Folio

A ledger folio, in simple words, is a page number of the ledger account where the relevant account appears. The term ‘folio’ refers to a book, particularly a book with large sheets of paper. In accounting, it’s used to maintain ledger accounts.

The use of ledger folio is generally seen in manual accounting, i.e the traditional book and paper accounting as it is a convenient tool used for tracking the relevant ledger account from its journal entry. Whereas, in computer-oriented accounting (or computerized accounting), it’s not really an issue to track your relevant ledger account.

Ledger folio, abbreviated as ‘L.F.’, is typically seen in journal entries. The ledger folio is written in the journal entries, after the ‘date’ and ‘particulars’ columns. It is really convenient when we’re dealing with and recording a large number of journal entries. As we will be further posting them into ledger accounts, thus, ledger folio comes in as a really useful component of journal entries.

- The number in the ledger folio may be numeric or alphanumeric.

- The ledger folio column in the journal has nothing to do with the accounting principles and rules. It’s used by us as per our methods and needs.

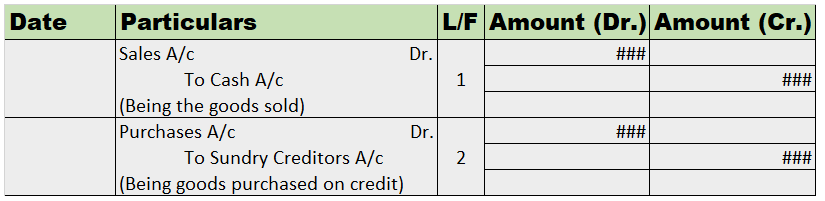

Example

We’ll look at how the ledger folio column is used while recording journal entries.

We can find the relevant ledger accounts on the page numbers of the book as mentioned in the above entries, i.e. the cash and sales account on page – 1 whereas, the purchases and sundry creditors on page – 2 of the relevant ledger book.

See less

An asset is an item of property owned by a company/business. It may be for a longer or shorter period of time. Assets are classified into two broad heads: Non-Current Assets Current Assets The asset may be sold for several reasons such as: An asset is fully depreciated. It should be sold becaRead more

An asset is an item of property owned by a company/business. It may be for a longer or shorter period of time. Assets are classified into two broad heads:

The asset may be sold for several reasons such as:

The journal entry for profit on the sale of assets will be:

According to the golden rules of accounting, in the above entry “Cash/Bank A/c” it is a Real Account and the rule says “Debit what comes in” and so is debited.

“Asset A/c” is a real account and the rule says “Credit what goes out” and so is credited. Any Gain on sale of an asset goes to the Nominal account and according to the rule “Credit, all incomes and gains” and so is credited.

The journal entry for loss on sale of the asset will be:

In the above entry, “Loss on Sale of Asset” is debited because according to Nominal account rules “Debit all losses and expenses” and so is debited.

According to modern rules of accounting, “Debit entry” increases assets and expenses, and decreases liability and revenue, a “Credit entry” increases liability and revenue, and decreases assets and expenses.

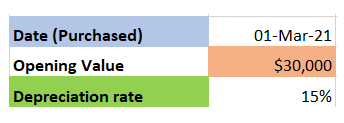

For example, Mr. A sold furniture for $2,500 and incurred a loss on the sale which amounted to $2,500.

According to modern rules, the journal entry will be: