Here are 10 examples of accounting entries: A company purchases $500 worth of office supplies on credit from a supplier. Office supplies expense account would be debited Accounts payable would be credited A firm receives $1,000 in cash from a customer for services rendered. In this case, CashRead more

Here are 10 examples of accounting entries:

- A company purchases $500 worth of office supplies on credit from a supplier.

- Office supplies expense account would be debited

- Accounts payable would be credited

- A firm receives $1,000 in cash from a customer for services rendered. In this case,

- Cash account would be debited

- Service revenue account would be credited

- A business pays $250 in salaries to its employees.

- A debit would be made to the salaries expense account

- A credit would be made to the cash account

- A business borrows $5,000 from a bank and receives the funds as a loan. The entry would be,

- A debit to the bank account

- A credit to the loan payable account

- A company sells $800 worth of inventory to a customer for cash.

- The entry would be a debit to the cash account

- A credit to the sales revenue account

- A firm purchases $3,000 worth of equipment on credit from a supplier.

- The entry would be a debit to the equipment account

- A credit to the supplier’s account

- A company incurs $500 in advertising expenses for a new marketing campaign (cash).

- The entry would be a debit to the advertising expense account

- A credit to the cash account

- A firm collects $1,200 from a customer. The entry would be,

- A debit to the cash account

- A credit to the customer’s account

- A business pays $700 in rent for its office space. The entry would be,

- A debit to the rent expense account

- A credit to the cash account

- An organization pays off a $2,000 loan to the bank. The entry would be,

- A debit to the loan payable account

- A credit the cash account

I also found a long list of example journal entries and a free PDF to download here.

See less

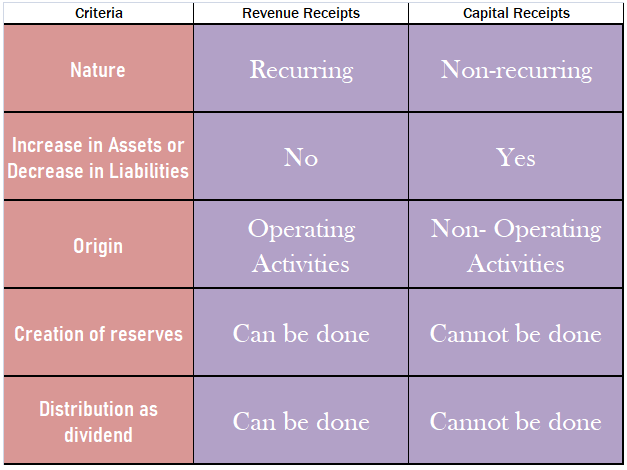

Debtors are treated as an asset. A debtor is a person or an entity who owes an amount to an enterprise against credit sales of goods and/or services rendered. When goods are sold to a person on credit that person is called a debtor because he owes that much amount to the enterprise. Debtors are consRead more

Debtors are treated as an asset.

A debtor is a person or an entity who owes an amount to an enterprise against credit sales of goods and/or services rendered.

When goods are sold to a person on credit that person is called a debtor because he owes that much amount to the enterprise.

Debtors are considered assets in the balance sheet and are shown under the head of current assets.

For example – Ram Sold goods to Sam on credit, Sam did not pay for the goods immediately, so here Sam is the debtor for Ram because he owes the amount to Ram. This amount will be payable at a later date.

Liabilities Vs Assets

Liabilities

It means the amount owed (payable) by the business. Liability towards the owners ( proprietor or partners ) of the business is termed internal liability. For example, owner’s capital, etc

On the other hand, liability towards outsiders, i.e., other than owners ( proprietors or partners ) is termed as an external liability.

For example creditors, bank overdrafts, etc.

Assets

An asset is a resource owned or controlled by a company. The benefit from the asset will accrue to the business in current and future periods. In other words, it’s something that a company owns or controls and can use to generate profits today and in the future.

For example – machinery, building, etc.

Current assets are defined as cash and other assets that are expected to be converted into cash or consumed in the production of goods or rendering of services in the normal course of business. They are readily realizable into cash.

In other words, we can say that the expected realization period of current assets is less than the operating cycle period.

For example, goods are purchased with the purpose to resell and earn a profit, debtors exist to convert them into cash i.e., receive the amount from them, bills receivable exist again for receiving cash against it, etc.

Why debtors are treated as assets?

Now let me explain to you why debtors are treated as assets and not as liabilities because of the following characteristics :

Conclusion

Now after the above discussion, I can conclude that debtors are considered to be an asset and not a liability.

See less