Under GST, Input Tax Credit (ITC) refers to the tax already paid by a person on input, which is available as a deduction from tax payable on output. This means that if you have paid tax on some purchases, then at the time of paying tax on the sale of goods, you can reduce it by the amount you alreadRead more

Under GST, Input Tax Credit (ITC) refers to the tax already paid by a person on input, which is available as a deduction from tax payable on output. This means that if you have paid tax on some purchases, then at the time of paying tax on the sale of goods, you can reduce it by the amount you already paid on purchase and pay only the balance amount.

EXAMPLE

Suppose Ashok purchased goods worth Rs 100 while paying tax at 10%, that is Rs 10. He now sold the goods for Rs 200, with a tax payable of Rs 20. Now, Ashok can avail input tax credit of Rs 10 that he already paid for the purchase and hence the net tax payable is Rs 10 (20-10).

METHOD OF UTILISATION OF ITC

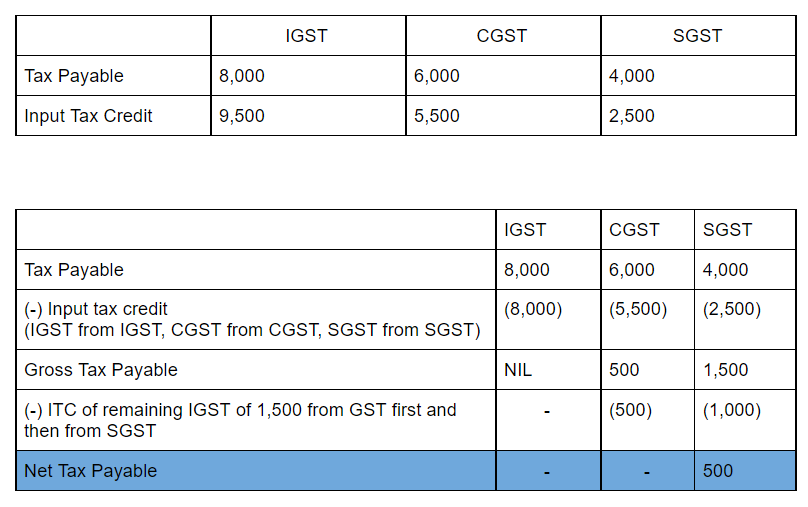

The central government collects CGST, SGST, UTGST or IGST based on whether the transactions are done intrastate or interstate.

The amount of input tax credit on IGST is first used for paying IGST and then utilised for the payment of CGST and SGST or UTGST. Similarly, the amount of ITC relating to CGST is first utilised for payment of CGST and then for the payment of IGST. It is not used for the payment of SGST or UTGST. Meanwhile, the amount of ITC relating to SGST is utilised for payment of SGST or UTGST and then for the payment of IGST. Such amounts are not used for payment of CGST.

We can see how Input Tax Credit is used from the below example and table:

The term "principal book of accounts'' refers to the set of ledgers that an entity prepares to group the similar transactions recorded as journal entries under an account. So to put it simply, the principal book of accounts mean ledgers. Ledgers are prepared by posting the debits and credits of a joRead more

The term “principal book of accounts” refers to the set of ledgers that an entity prepares to group the similar transactions recorded as journal entries under an account.

So to put it simply, the principal book of accounts mean ledgers.

Ledgers are prepared by posting the debits and credits of a journal entry to the respective accounts.

A ledger groups the transactions concerning the same account. For example, Mr B is a debtor of X Ltd. Hence all the transactions entered into with Mr. will be grouped into the ledger Mr B A/c in the books of X Ltd.

Ledgers are of utmost importance because all the information to any account can be known by its ledger.

Preparation of ledger is very important because all the information to any account can be known by its ledger. Ledgers also display the balance of each and every account which may be debit or credit. This helps in the preparation of the trial balance and subsequently the financial statements of an entity.

Hence, it is the most important book of accounts and calling it the ‘books of final entry’ is also justified.

See less