20 Journal Entries Journal is the book of initial entry, hence the transactions are at first recorded in the journal by the way of journal entries. Journal entries are made as per the double entry system of accounting, where for each transaction one account is debited and another account is creditedRead more

20 Journal Entries

Journal is the book of initial entry, hence the transactions are at first recorded in the journal by the way of journal entries.

Journal entries are made as per the double entry system of accounting, where for each transaction one account is debited and another account is credited.

In the case of compound journal entries, one set of accounts is debited and one set of accounts is credited.

The amount of debit and credit always remains the same.

For example, when cash is introduced into a business, it affects two accounts: Cash A/c and Capital A/c. The accounts are debited and. credited as per the golden rules of accounting.

The journal entries which I have provided are based on the following transactions and events:

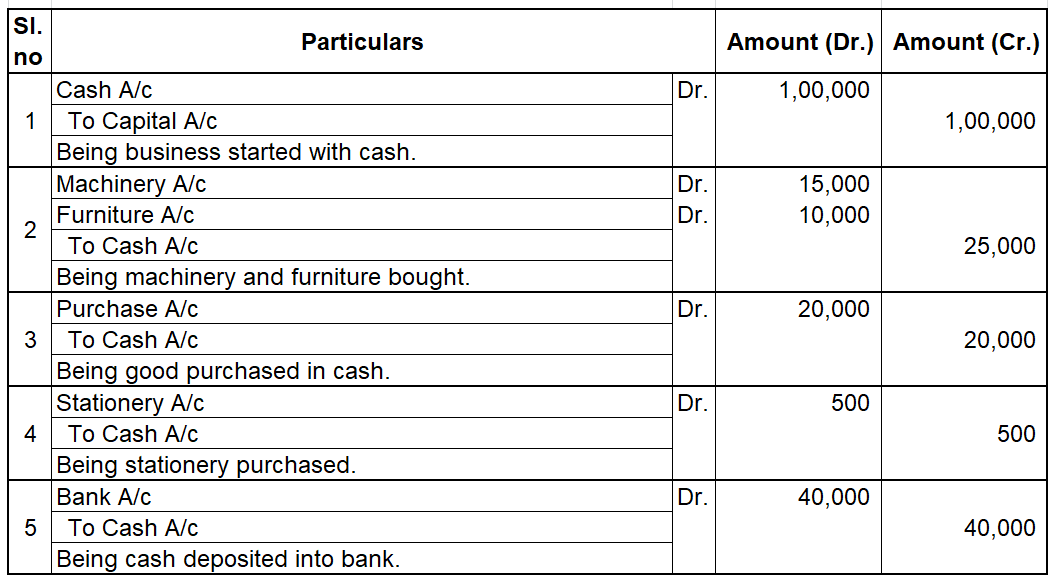

- The business started with Rs. 1,00,000

- Bought machinery for Rs. 15,000 and furniture for Rs. 10,000

- Purchased goods of Rs. 20,000 with cash

- Bought Stationery for Rs. 500

- Cash deposited into bank Rs. 40,000

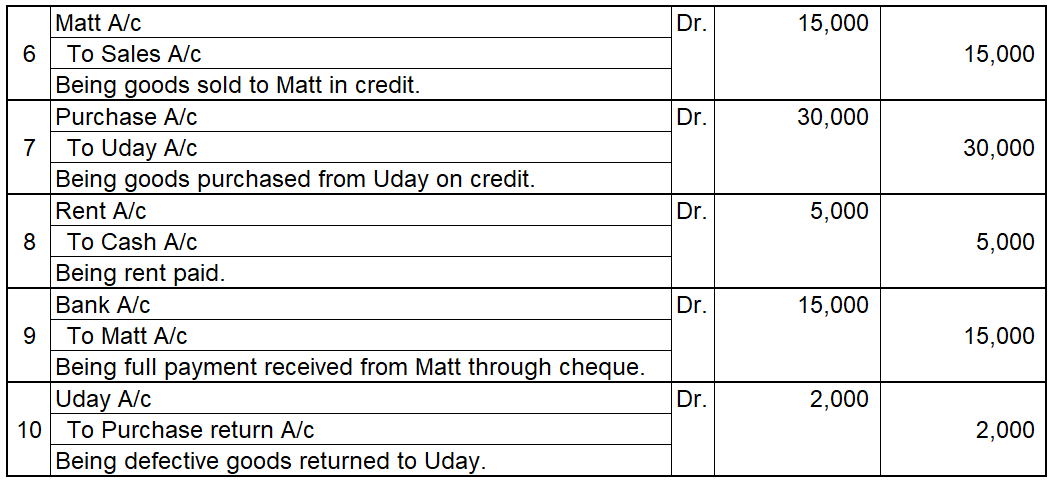

- Goods sold to Matt for Rs. 15,000

- Purchased goods from Uday of Rs. 30,000

- Being Rs. 5,000 rent paid for premises

- Cheque received from Matt of Rs. 15,000

- Defective goods returned to Uday returned of Rs. 2,000

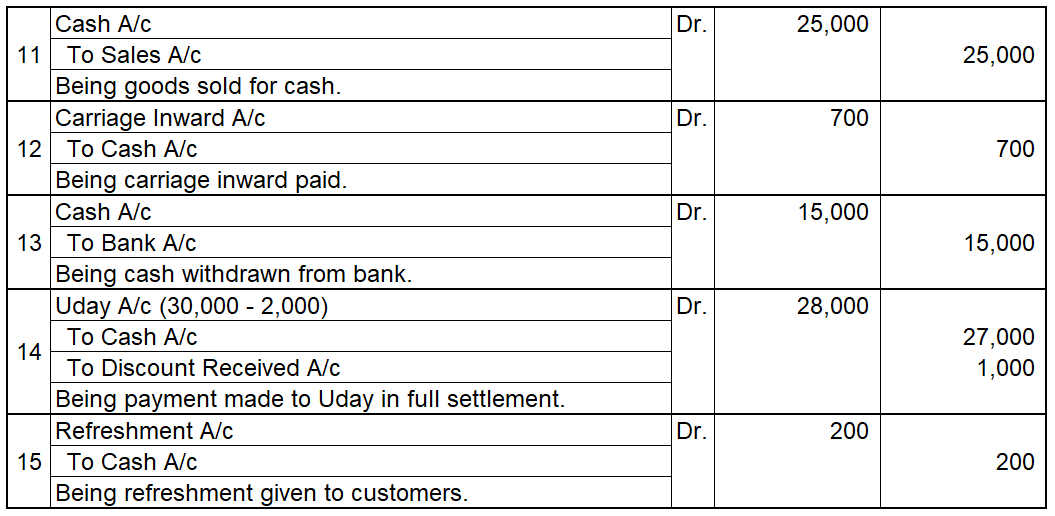

- Cash sales of Rs. 25,000

- Carriage Inward paid Rs. 700

- Cash withdrawn from bank Rs. 15,000

- Full payment made to Uday in cash. Discount received from Uday Rs. 1000.

- Refreshments given to customers of Rs. 200

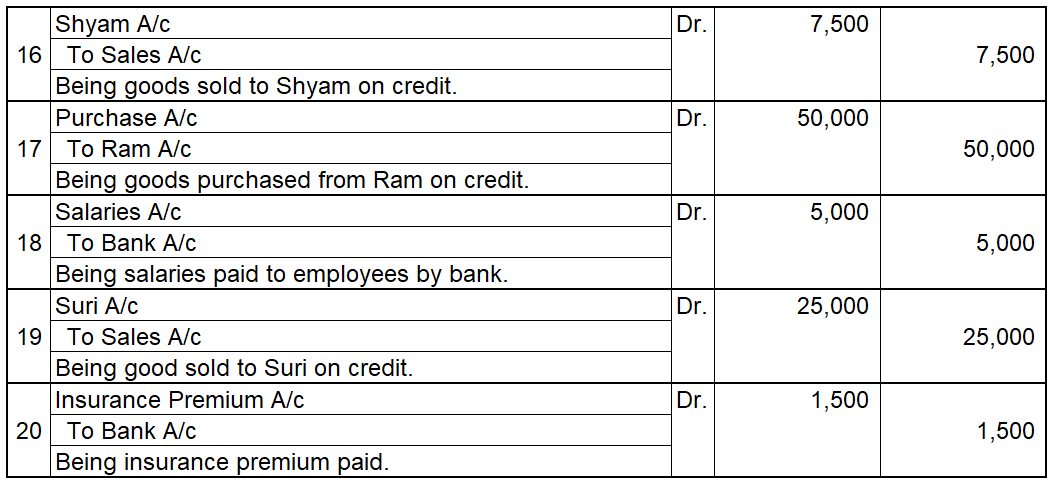

- Goods sold to Shyam for Rs. 7,500

- Goods purchased from Ram of Rs. 50,000

- Salaries paid to employees by bank Rs. 5,000

- Good sold to Suri for Rs. 25,000

- Insurance premium paid of Rs. 1,500 by the bank.

Journal Entries

The journal entries based on the above are as follows:

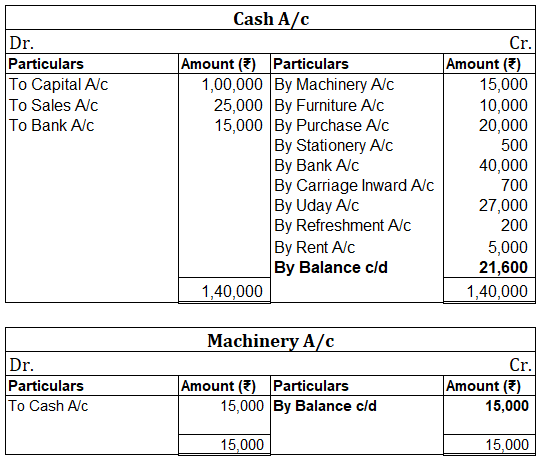

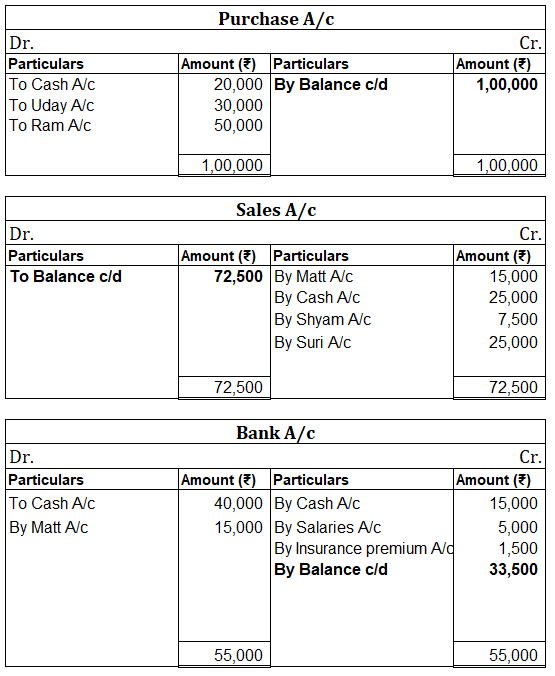

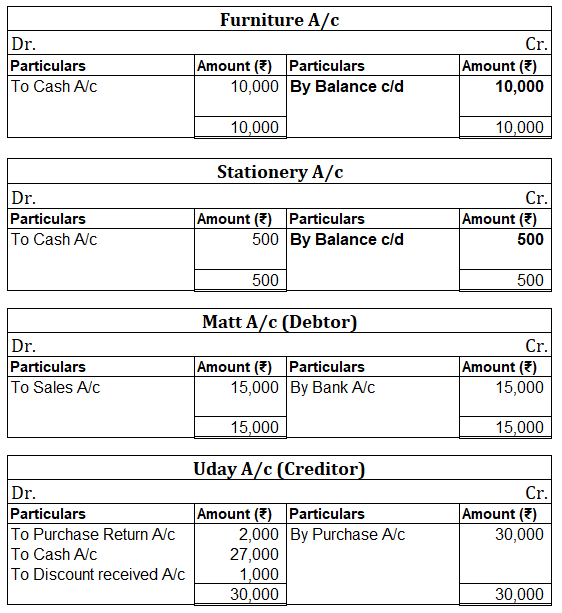

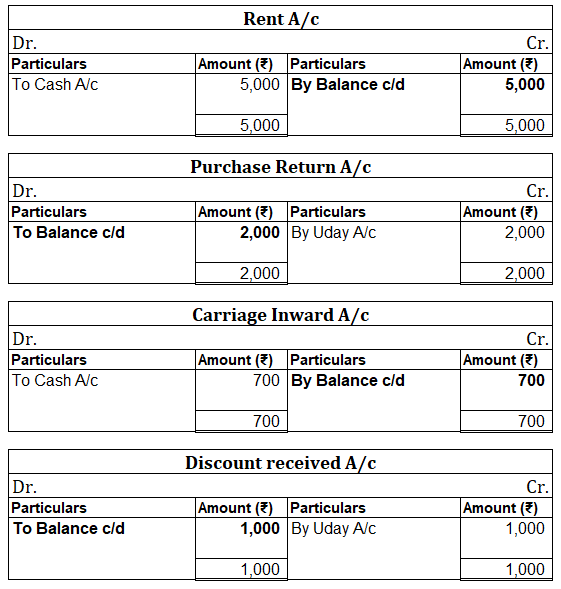

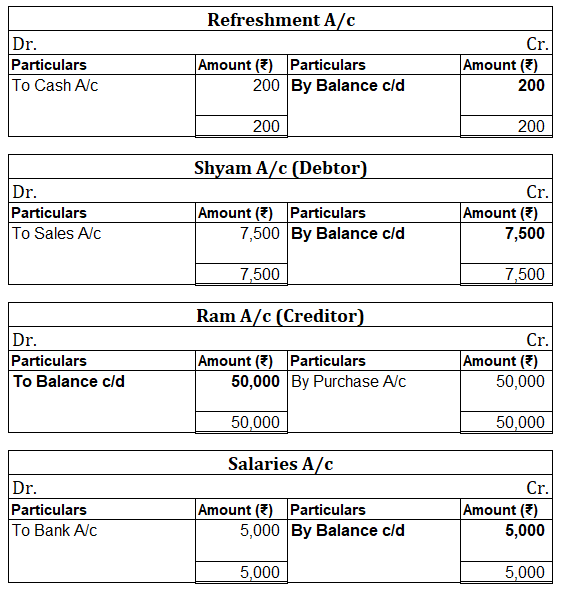

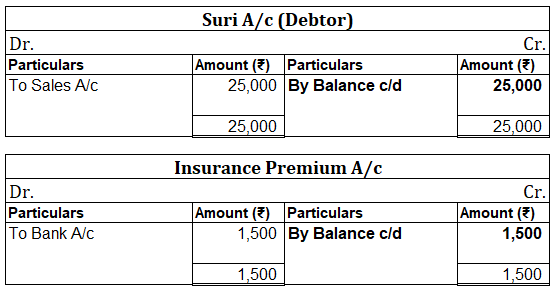

Ledgers

Ledger is known as the book of final entry. It is the book where the transactions related to a specific account are posted. This posting of transactions is done from journal entries.

The posting of journal entries into the ledger is performed in the following way:

The journal entry of cash sales is :

| Cash A/c Dr. | Amt | ||

| To Sales A/c | Amt |

Here, Cash A/c is debited to Sales A/c. So, in the Cash A/c ledger, posting will be made on the debit side as “To Sales A/c”

In the Sales A/c ledger, the posting will be made on the credit as “By Cash A/c” because Sales A/c is credited to Cash A/c

For creating ledgers, journal entries are a prerequisite.

Now, the ledgers to be created as per the journal entries made above are as follows:

- Cash A/c

- Bank A/c

- Capital A/c

- Furniture A/c

- Machinery A/c

- Purchase a/c

- Sales A/c

- Matt A/c (Debtor)

- Uday A/c (Creditor)

- Rent A/c

- Purchase Return A/c

- Stationery A/c

- Carriage Inward A/c

- Refreshment A/c

- Shyam A/c (Debtor)

- Ram A/c (Creditor)

- Suri A/c (Debtor)

- Refreshment A/c

- Discount Received A/c

The account ledgers are as follows:

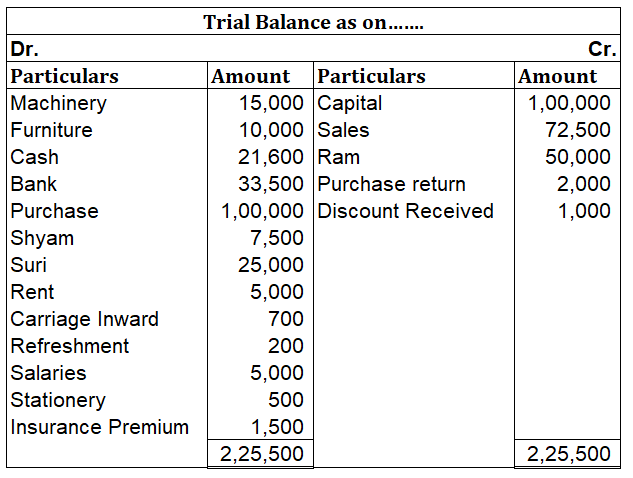

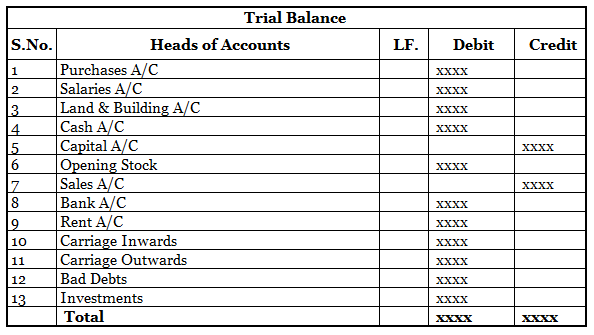

Trial Balance

A trial balance is a statement that is prepared to check the arithmetical accuracy of books of accounts.

In this statement, the total of all accounts having debit balance and the total of all accounts having credit balance is computed. If the total of debit and credit matches, then it can be said that the books of accounts are arithmetically accurate.

Here also we have prepared the trial balance by computing the total of accounts having debit balances and the total of accounts having credit balances

The debit column total and credit column total are matching. Hence, we can say that the books of accounts we have prepared are arithmetically accurate.

Note: Matt A/c and Uday A/c have not appeared in the trial balance because they do not have any carrying balance.

See less

The term set off in English means to offset something against something else. It thereby refers to reducing the value of an item. In accounting terms, when a debtor can reduce the amount owed to a creditor by cancelling the amount owed by the creditor to the debtor, it is termed as set off. It is coRead more

The term set off in English means to offset something against something else. It thereby refers to reducing the value of an item. In accounting terms, when a debtor can reduce the amount owed to a creditor by cancelling the amount owed by the creditor to the debtor, it is termed as set off.

It is commonly used by banks where they seize the amount in a customer’s account to set off the amount of loan unpaid by the customer.

Types

There are various types of set-offs as given below:

Example

Let’s say Divya owes Rs 20,000 to Sherin for the purchase of goods. But, Sherin owed Rs 6,000 to Divya already for use of her Machinery. Therefore, the amount of 6,000 can be set off against the 20,000 owed to Sherin and hence Divya would effectively owe Sherin Rs 14,000.

This helps in reducing the number of transactions and unnecessary flow of cash.

See less