As per AS-10 ( Revised ): Property, Plant and Equipment, depreciation on an asset should begin when the asset is in the location and condition necessary for it to be capable of operating in the manner as intended by the management. This means a firm should start charging depreciation when the assetRead more

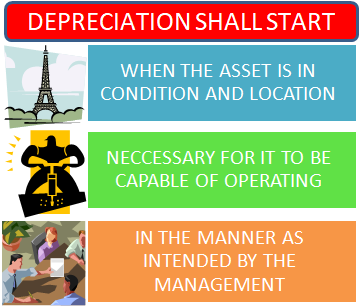

As per AS-10 ( Revised ): Property, Plant and Equipment, depreciation on an asset should begin when the asset is in the location and condition necessary for it to be capable of operating in the manner as intended by the management.

This means a firm should start charging depreciation when the asset is ready to be used as per the management’s desire.

Let’s take an example to understand this clearly:

A business bought a drinking water cooler for its office use on 1st April 2021. Now, this water cooler needs to be installed and wiped with Isopropyl Alcohol before it can be put to use.

The business completed all the required procedures by 1st May 2021, but it opened the machine for office use from 1st August 2021.

So the question arises, from when to start charging depreciation?

- 1st April 2021 – The date of Purchase

- 1st May 2021- The date when the machine was ready to use.

- 1st August 2021 –The date from which the machine was put to use.

The answer is 1st May 2021– The date when the machine was ready to use.

It doesn’t matter whether the company started the use of an asset or not. Once an asset is in

- the location and condition

- necessary for it to be capable of operating

- as intended by the management,

the depreciation should begin.

See less

Fictitious assets On seeing or hearing ‘fictitious’, the words which come to our mind are ‘not true, ‘fake’ or ‘fantasy’. So, fictitious assets are those items that appear on the assets side of the balance sheet but are actually not assets. In substance, fictitious assets are the expenses and lossesRead more

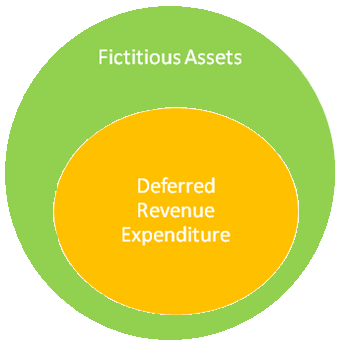

Fictitious assets

On seeing or hearing ‘fictitious’, the words which come to our mind are ‘not true, ‘fake’ or ‘fantasy’. So, fictitious assets are those items that appear on the assets side of the balance sheet but are actually not assets.

In substance, fictitious assets are the expenses and losses that are not completely written off in a financial year and are required to be carried forward to the next financial year.

The examples of fictitious assets are as follows:

Fictitious assets appear on the asset side of the balance sheet as expenses and losses have a debit balance.

*when the balance sheet is prepared as per Schedule III of Companies Act, the Net loss is shown as a negative figure under the head Reserve and Surplus.

Intangible Assets

Intangible assets mean the assets which don’t have any physical existence. They cannot be seen or touched but are assets because they do provide future economic benefits to the business. Like tangible assets (like machinery and building), they can be also created, purchased or sold.

Like tangible assets are depreciated, intangible assets are gradually written over by amortization over their useful lifespan to account for the economic benefits provided by them.

Following are the examples of intangible assets:

Intangible assets which are created by the business-like goodwill or brand recognition do not appear in the balance sheet.

Only acquired intangible assets can be shown in the balance sheet. Like purchased goodwill, patents, trademarks etc.

Intangible assets also face impairment if their fair value is less than their carrying value after deducting amortization expense. The difference between carrying value and fair value is shown in the Profit and loss A/c as impairment charge and the asset is valued at fair value in the balance sheet.

See less