Prepaid Payable Prepaid payable or prepaid expenses refer to the future expenses that have been paid in advance. It is an advance payment made by the business for the goods and services to be received by the business in the future. A prepaid expense is an asset on the balance sheet. The number of prRead more

Prepaid Payable

Prepaid payable or prepaid expenses refer to the future expenses that have been paid in advance. It is an advance payment made by the business for the goods and services to be received by the business in the future.

A prepaid expense is an asset on the balance sheet. The number of prepaid expenses that will be used up within one year is reported on a company’s balance sheet as a current asset. According to generally accepted accounting principles (GAAP), expenses should be recorded in the same accounting period as the benefit generated from the related asset.

Example

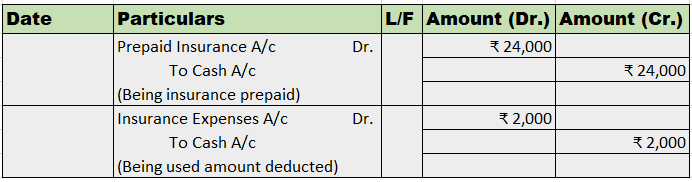

ABC Ltd. purchases insurance for the warehouse. It was ₹2,000 per month. The company pays ₹24,000 in cash upfront for a 12-month insurance policy for the warehouse. Each month an adjusting journal entry will be passed, adjusting the amount of insurance used from the prepaid insurance.

Journal Entry-

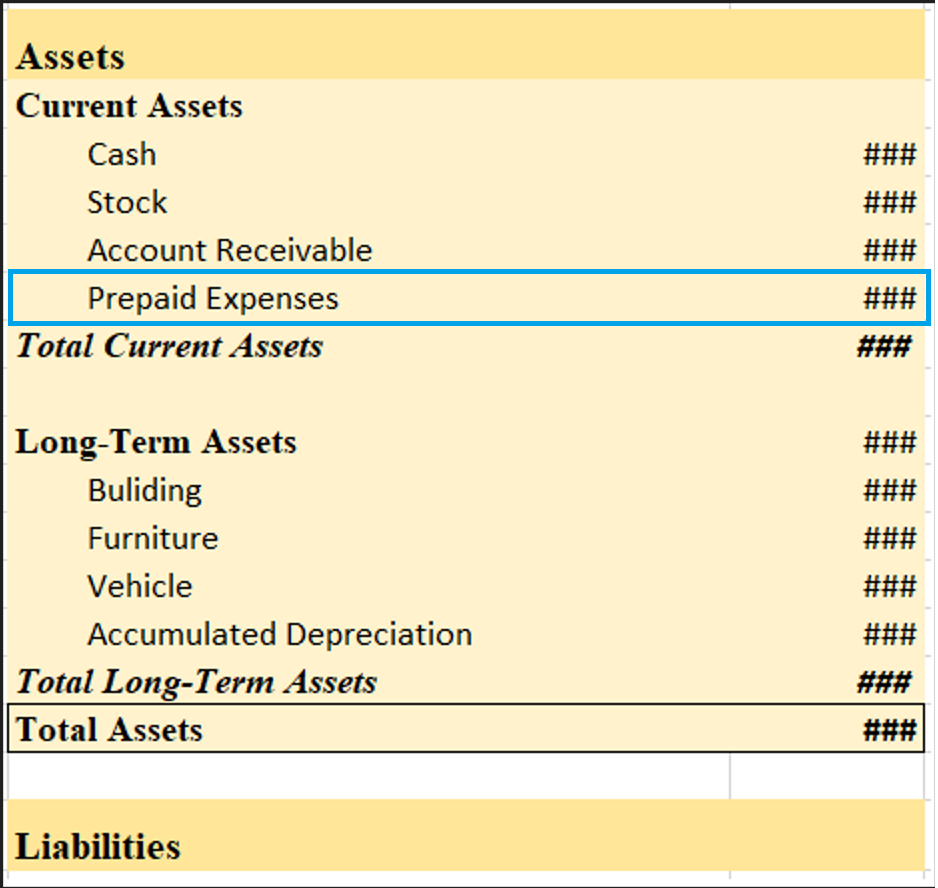

Prepaid Expenses in Balance Sheet-

Prepaid expenses are shown in the balance sheet under the current assets heading as it’s a short-term asset and to be consumed within one accounting year.

Balance Sheet (for the year ending…)

Profit refers to the excess of total revenue over total expenses. According to the rule "Debit all expenses and losses, Credit all incomes and gains", expenses are recorded on the debit side while revenues are recorded on the credit side. There is profit when Total revenue > Total expenses, whichRead more

Profit refers to the excess of total revenue over total expenses. According to the rule “Debit all expenses and losses, Credit all incomes and gains”, expenses are recorded on the debit side while revenues are recorded on the credit side.

There is profit when Total revenue > Total expenses, which means the balance of the credit side > the balance of the debit side. Since, in accounting Dr. side is always equal to the credit side, a balancing figure (representing profit or loss) is shown on the shorter side, to make both sides equal.

When Credit side > Debit side, Profit(balancing figure) is shown on the Dr. side so that both sides are equal.

PROFIT

Profit refers to the excess of total revenue over the total expenses of the business for an accounting year. In simple words, it shows how much extra the firm earned after deducting all the expenses it incurred during the year.

Profit = Total Revenue – Total Expenses

Suppose, the firm earned a total revenue of $10,000 for the accounting year 2022-23. Also, it incurred total expenses of $6,000 during the year. So, Profit for the AY 2022-23 is $4,000.

ASCERTAINING PROFIT

To ascertain profit earned or loss incurred by the firm during an accounting year, it prepares two accounts.

Points to be noted:

TRADING ACCOUNT

It is the first final account prepared for calculating gross profit or gross loss during the year because of the trading activities of the firm.

Trading activities are related to the buying and selling of goods. In between buying and selling a lot of activities are there like transportation, warehousing, loading, unloading, etc. All expenses that are directly related to buying and selling as well as manufacturing of goods are known as Direct expenses and are also recorded in the trading accounts.

Items included on the debit side:

Items included on the credit side:

Gross Profit is when Cr. side (incomes) > Dr. side (expenses). It is recorded on the debit side as a balancing figure.

PROFIT AND LOSS ACCOUNT

A businessman incurs a lot of expenses during the year which may be directly related or indirectly related to the business.

As the Trading account only considers direct expenses, the businessman prepares the P&L A/c which considers all the expenses incurred during a year to ascertain net profit or loss.

Items written on the Debit side

Items written on the Credit side

Net Profit is when the Cr. side (incomes)> Dr. side(expenses). It is recorded on the Debit side as a balancing figure.

See less