No, drawings are not shown in the statement of profit or loss. By drawings, we mean the withdrawal of cash or goods by the owner of the business for his personal use. Drawings are actually shown in the balance sheet as a deduction from the capital account. Let’s take an example, Mr X runs a tradingRead more

No, drawings are not shown in the statement of profit or loss. By drawings, we mean the withdrawal of cash or goods by the owner of the business for his personal use.

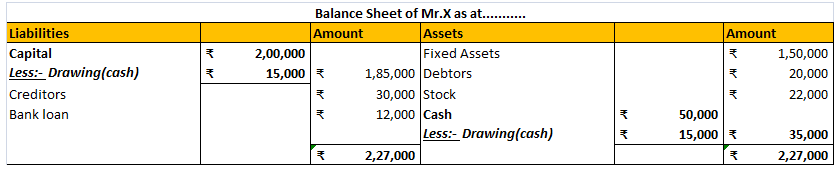

Drawings are actually shown in the balance sheet as a deduction from the capital account.

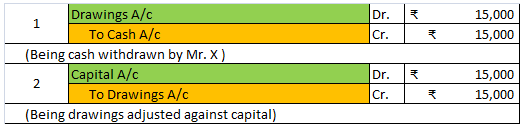

Let’s take an example, Mr X runs a trading business. For meeting his personal expense we withdrew cash from his business cash of amount Rs. 15,000. It shall be reported like this:

Journal Entries:

Balance sheet:

Profit and loss account reports only the nominal accounts i.e. incomes and expenses. That’s why drawings are not shown in the statement of profit or loss because it is neither an expense nor an income.

It represents the owner’s withdrawal of capital from business for personal use. Hence, the drawings account is a personal account. Drawings lead to a simultaneous reduction in capital and cash or stock of a business which has nothing to do with Profit and loss A/c.

Therefore it is reported in the balance sheet only.

See less

The word, “deferred” means delayed or postponed and “revenue” in layman’s terms means income. Therefore deferred revenue means the revenue which is yet to be recognised as income. It is actually unearned income. In accrual accounting, income is recognised only when it is accrued or earned. DeferredRead more

The word, “deferred” means delayed or postponed and “revenue” in layman’s terms means income. Therefore deferred revenue means the revenue which is yet to be recognised as income. It is actually unearned income.

In accrual accounting, income is recognised only when it is accrued or earned. Deferred revenue is the income received before the performance of the economic activity to earn it.

Example: A shoe shop owner gives an order to a shoe manufacturer of 1000 pair of shoes which is to be delivered after 4 months. He also gives him a cheque of ₹15,000 in advance, the rest ₹5000 is to be given at the time of delivery.

So, in this case, the ₹15,000 is actually is unearned revenue i.e. deferred revenue. It will be recognised as revenue when the shoe manufacture completes the order and deliver it.

Till then, the deferred revenue is reported as a liability in the balance sheet. Like this:

After recognition as revenue, it will be reported in the statement of profit or loss:

Hence, to summarise, deferred revenue is:

Some examples of deferred revenue are as follows:

Now the question arises why deferred revenue is recognised as a liability. It is due to the fact that the business may not be able to perform the economic activity successfully to earn that revenue.

Taking the above example, suppose the shoe manufacturer is not able to honour its commitment and the shoe shop owner can wait no more, then the advanced money of ₹ 15,000 is to be refunded. That’s why deferred revenue is recognised as a liability because it is a liability if we consider the principle of conservatism (GAAP).

See less