A) No entries made at all in the general ledger for items paid by petty cash B) The same number of entries in the general ledger. C) Fewer entries made in the ...

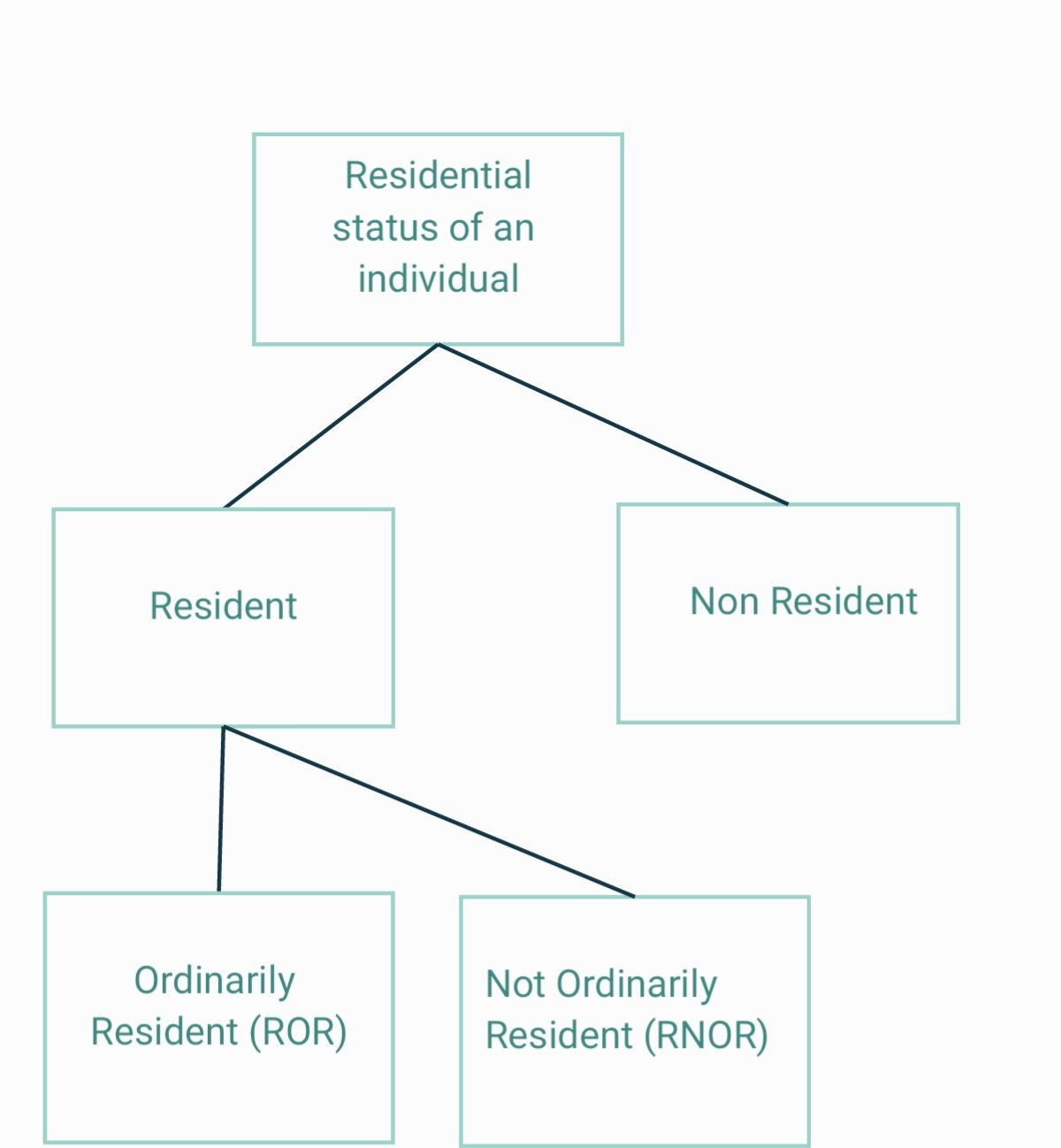

To determine if a person is a resident in India as per the Income Tax Act 1961, he has to fulfil any of the 2 following conditions; Condition A Stay in India for 182 days or more in the previous year, or Stay in India for 60 days or more in the previous year and another 365 days or more in the 4 yeaRead more

To determine if a person is a resident in India as per the Income Tax Act 1961, he has to fulfil any of the 2 following conditions;

Condition A

- Stay in India for 182 days or more in the previous year, or

- Stay in India for 60 days or more in the previous year and another 365 days or more in the 4 years immediately preceding the previous year.

The second condition above is not applicable if he is an Indian citizen leaving India for the purpose of employment, or he is a member of the crew of an Indian ship, or he is only coming to India on a visit.

If he fails to fulfil either of the two conditions, then he is termed as a non-resident.

In India, a resident person can be classified into two:

- Resident and ordinarily resident

- Resident but not ordinarily resident

Condition B

A resident is a resident and ordinarily resident if (B):

- He has been a resident in India for at least 2 out of the previous 10 years immediately preceding the relevant previous year, and

- He has been in India for a period of 730 days or more during 7 years immediately preceding the relevant previous year.

If a person satisfies any one condition of (A) but does not follow all conditions of (B), then he is termed as a resident but not ordinarily resident.

EXAMPLE

If Nithin is living in India for 190 days in the previous year and was a resident for the previous two years only staying for 400 days in the previous 7 years, then he fulfils condition (A) but not both conditions of (B) and hence he is a resident but not ordinarily resident.

The correct option is D) Fewer entries in the general ledger To understand why option D is correct, we need to understand the concept. Petty cashbook is a special cashbook prepared for recording petty or small cash expenses. The benefit is that the chief cashier can focus on large cash and bank tranRead more

The correct option is D) Fewer entries in the general ledger

To understand why option D is correct, we need to understand the concept.

Option A ‘No entries made at all in the general ledger for items paid by petty cash ‘ is wrong. It is not possible to omit entries of petty expense just because there is a petty cashbook. There will be entries related to:

Petty cash A/c Dr. Amt

To Cash A/c Amt

Option (B) ‘The same number of entries in the general ledger is wrong because there can never be the same number of entries as all the petty expenses are recorded in the petty cashbook and only the entries for transfer of cash to the petty cashier is recorded in the main cash book.

Option D ‘More entries made in the general ledger’ is wrong because the number of entries actually reduce as only petty cash transfer entries are recorded in the main cashbook instead of numerous entries of petty cash transactions.

See less