Meaning A valuation account is a balance sheet account that is paired with another balance sheet account to report the carrying amount of the paired account at a reduced value. The purpose of a valuation account is to reduce the balance of the concerned asset or liability without affecting the mainRead more

Meaning

A valuation account is a balance sheet account that is paired with another balance sheet account to report the carrying amount of the paired account at a reduced value.

The purpose of a valuation account is to reduce the balance of the concerned asset or liability without affecting the main ledger account. This is a conservative approach to use valuation accounts to present the value of the concerned asset or liability at a reduced value.

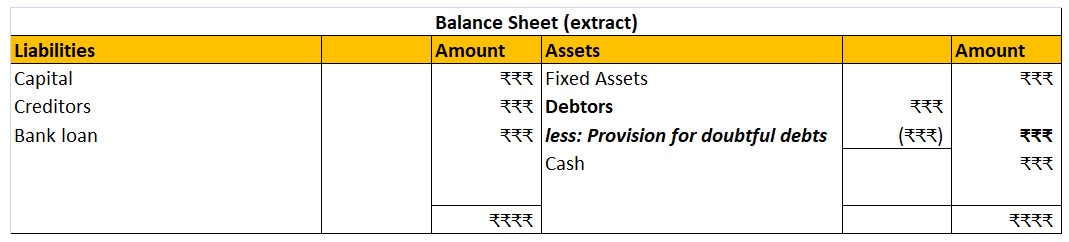

The most common example of a valuation account is the ‘Provision for doubtful debts account’. It appears in the balance sheet as a reduction from the debtors’ accounts. Also when the amount is transferred to this provision, it appears in the statement of profit and loss account. But it doesn’t appear in the debtors’ account ledger.

Treatment

A valuation account appears only in the balance sheet. Sometimes, it also appears in the profit and loss account when any amount is transferred to it.

Valuation accounts are only used in accrual accounting. They cannot be used in cash-based accounting as there is no flow of cash related to valuation accounts.

They have a balance opposite of their paired accounts i.e. if their paired account is an asset then they will have a credit balance and if it is a liability then they will have a debit balance.

Other Examples of valuation accounts are as follows:

- Provision for doubtful debts (offsets the account receivables or debtors’ account)

- Accumulated depreciation (report the assets net of depreciation)

- Discount on bonds payable (reduces the reporting balance of bond payable account)

Sales return shows the sale price of goods returned by customers. It is deducted from sales or gross sales in the income statement. It is a contra revenue account that represents returns from the customers and deductions to the original selling price, in case of any defective product received by theRead more

Sales return shows the sale price of goods returned by customers. It is deducted from sales or gross sales in the income statement.

It is a contra revenue account that represents returns from the customers and deductions to the original selling price, in case of any defective product received by the customer or any other manufacturing default.

Sales allowances arise when any customer accepts the product at a lower price than the original price or, in other words, a reduction in the price charged by a seller, due to any problem related to the sold product like a quality issue, an incorrect price charged or shipment issue.

Sales allowances are created before the final billing is paid by the buyer.

Journal entry for sales return and allowances:

See less