Journal entries in the ledger What is a Journal Entry? Journal entry is a form of bookkeeping. All the economic or non-economic transactions in the business are recorded in the journal entries showing a company's debit or credit balances. It is a double-entry accounting method and requires at leastRead more

Journal entries in the ledger

What is a Journal Entry?

Journal entry is a form of bookkeeping. All the economic or non-economic transactions in the business are recorded in the journal entries showing a company’s debit or credit balances. It is a double-entry accounting method and requires at least two accounts or more in a transaction.

The journal entry helps to identify the transactions. We use journals to get a running list of business transactions. Each journal entry provides this specific information about a transaction:

- Date of the transaction.

- Accounts involved in it.

- Payer, payee, receiver, etc.

- Account name.

- Debit and credit of money.

General Ledger

After the transactions are recorded in the journal, they are posted in the principal book called ‘Ledger’. A ledger account contains information about a specific account. It contains the opening balance as well as the closing balances of an account. It summarizes the business transactions.

Transferring the entries from journals to respective ledger accounts is called ledger posting or posting to the ledger accounts. Balancing of ledgers is carried out to find differences at the year’s end, it means finding the difference between the debit and credit amounts of a particular account.

For instance,

Suppose goods were bought for cash. While passing the journal entry, we’ll be debiting the purchases a/c and crediting the cash a/c by stating it as, ‘To Cash A/c’.

Now, this entry will be affecting both the purchases account and the cash account. In the cash account, we’ll be debiting purchases. Whereas in the purchases account, we’ll be crediting the cash. That’s how it works in the double-entry bookkeeping system of accounting.

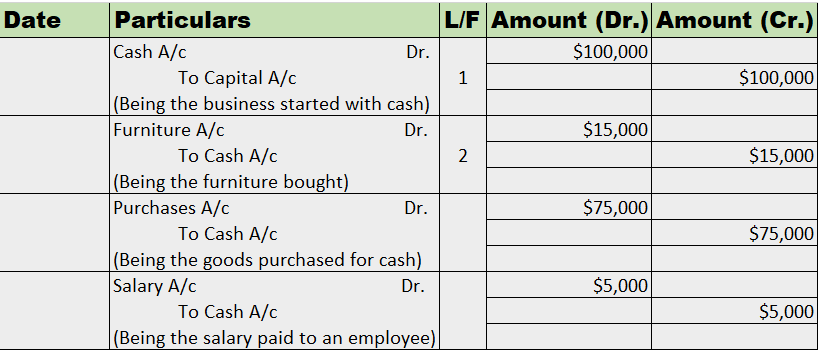

Example

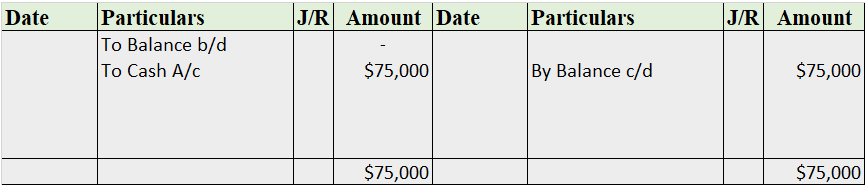

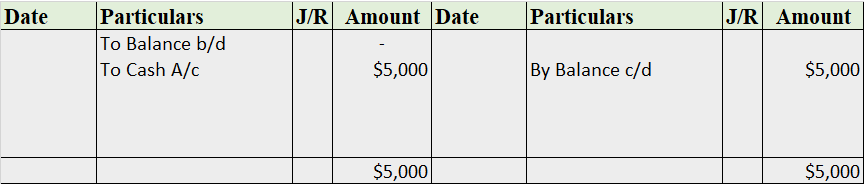

Mr. Tony Stark started the business with cash of $100,000. He bought furniture for business for $15,000. He further purchased goods for $75,000. He hired an employee and paid him a salary of $5,000.

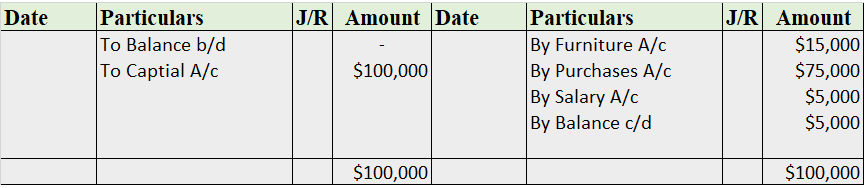

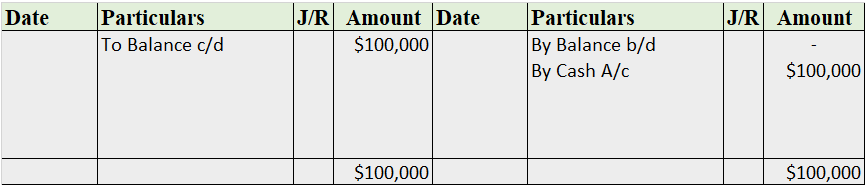

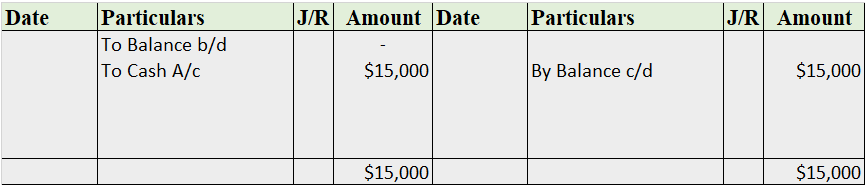

Now, we’ll be journalizing the transactions and posting them into the ledger accounts.

Journal Entries

Recording into Ledger Account

Cash A/c

Capital A/c

Furniture A/c

Purchases A/c

Salary A/c

Note: The balance b/d is not applicable as this is the business’ commencement year.

See less

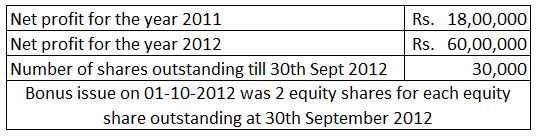

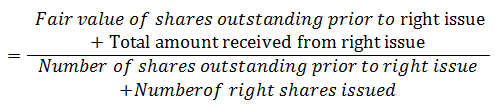

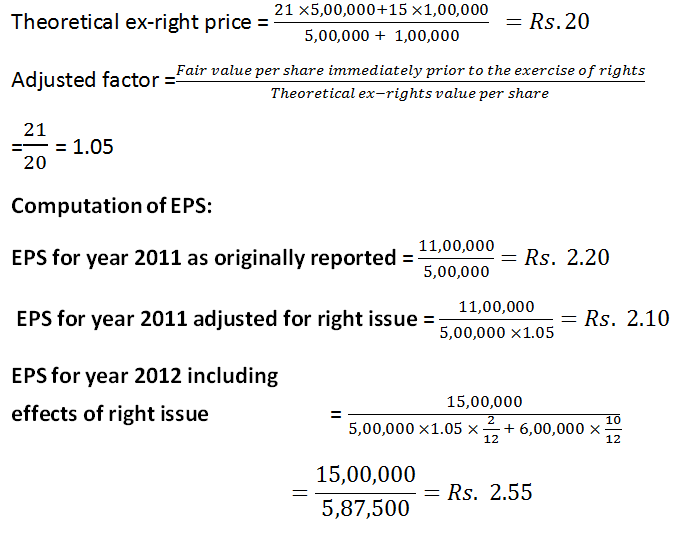

Earnings per share indicate the profit-generating capability of an enterprise and potential investors often compare the EPS of different companies to choose the best investment alternative.

Earnings per share indicate the profit-generating capability of an enterprise and potential investors often compare the EPS of different companies to choose the best investment alternative.

Tally ERP does not have a voucher for recording closing stock journal entries. It automatically calculates closing stock and reports it in the Profit and Loss account and Balance sheet. However, Tally do have vouchers through which you can adjust the closing stock to be shown at the end of the year.Read more

Tally ERP does not have a voucher for recording closing stock journal entries. It automatically calculates closing stock and reports it in the Profit and Loss account and Balance sheet.

However, Tally do have vouchers through which you can adjust the closing stock to be shown at the end of the year.

Explanation

Tally, as we know is an ERP which can automate many aspects of accounting like calculation of ledger balance, creation of trial balance, financial statements and other reports. Only the data entry in vouchers is done manually.

Tally also calculates closing stock automatically because it already has the required data to do so.

Closing stock = Opening stock + Purchase – Cost of goods sold.

Using the above formula, Tally automatically calculates the closing stock.

But it may happen that the closing stock as per Tally and closing stock as per physical verification of stock do not match.

This may be due to damaged caused to some items of inventory or even theft of inventory items which is usually discovered when stock is physically checked and counted at the end of the financial year.

In that case, we can use the Physical Stock voucher to correct our closing stock in Tally.

Physical Stock Voucher

A physical Stock voucher is an inventory voucher which is used to adjust the amount of closing stock as per the physical stock verified at the end of the year.

Suppose, if the closing stock for Bricks is 500pcs. Like in my stock summary, the item ‘Bricks’ is shown in the image below:

But after physical verification, it was found that there around there are only 450pcs of whole bricks are there. The rest of the bricks were broken.

To rectify this, we will open a Physical Stock voucher.

The steps to open a Physical stock voucher are as follows:

In Tally ERP 9 : Gateway of Tally → Accounting Vouchers → Press Alt + F10

In the physical stock voucher, we will select the stock item and enter the correct quantity, which is 450pcs.

After entering the details above, accept the voucher and open the stock summary again from Gateway of Tally. It will show the Bricks at 450pcs.

Hence, this is how we can adjust our closing stock in Tally.

See less