Capital Expenditure: Capital expenditure is the expenditure incurred by an entity or organization to acquire or purchase a fixed asset. This expenditure forms part of non-current assets. The fixed asset is not expensed at the time of purchase instead, it is depreciated or amortized over its useful lRead more

Capital Expenditure:

Capital expenditure is the expenditure incurred by an entity or organization to acquire or purchase a fixed asset. This expenditure forms part of non-current assets. The fixed asset is not expensed at the time of purchase instead, it is depreciated or amortized over its useful life.

Example of Capital Expenditure:

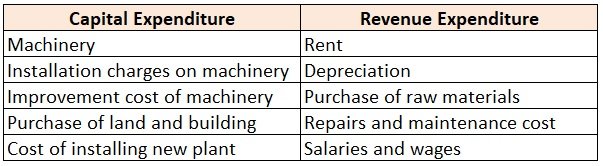

- Machinery: Machinery is a tangible non-current asset purchased by a company for business purposes. Since it is a non-current asset company will be using it for more than one accounting period hence, it should be capitalized in the balance sheet under the head assets. Capitalization is a method in which cost is included in the value of the asset and expensed over its useful life.

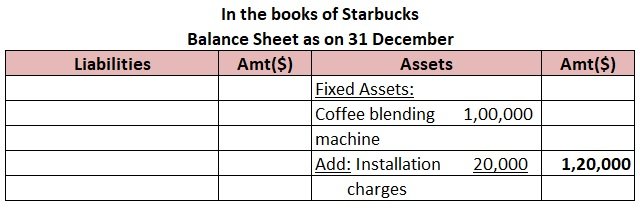

For example, XYZ Ltd purchased machinery worth $1,00,000 and its useful life is 10 years.

In this case, XYZ Ltd will capitalize the amount of machinery because it will be using it for more than one accounting year. Any asset used for more than one accounting year should be capitalized.

- Installation charges on machinery: This expense is incurred while installing machines in the business premises and is a one-time expenditure. The whole amount of installation will be capitalized along with the cost of machinery in the balance sheet.

In the above example cost of the machine is given as $1,00,000 and at the time of installation company incurred a further expenditure of $10,000. Here, the company will add the amount of installation with the cost of machinery because the installation charge is a one-time expense. The total cost of the machine will be $1,10,000.

- Improvement cost of machinery: Any cost incurred in the improvement of the machine will be capitalized. It is so as it will improve the quality or extend the life of the machinery. Hence, this cost should be added to the historic cost of the machine.

In the above example, after installation charges were incurred historic cost of the machine was $1,10,000. After a few years, the company made some improvements to the machine which amounted to $20,000 and the machine’s useful life was extended to more 5 years.

The improvement cost of $20,000 will be added to the historical cost of $1,10,000. The total amount of $1,30,000 ($1,10,000+$20,000) will be shown in the balance sheet.

Revenue Expenditure:

Revenue expenditure is expenditure incurred for the purpose of trade or to maintain non-current assets. These are short-term expenses and consumed within one accounting year and also known as operating expenses.

Examples of Revenue Expenditure:

- Rent: It is an expense paid by the company for using the premises for business purposes to the owner of the premises. It is recurring in nature and hence, should be classified under revenue expenditure.

For example, a company rented premises for business purposes and paid a monthly rent of $10,000. This expenditure of $10,000 incurred will fall under revenue expenditure because the company is incurring this expenditure monthly.

- Depreciation: Depreciation is a non-cash expense and it is added back to the cash flow statement, alongside other expenses. This expense is incurred as a basis of consuming a portion of fixed assets for the current period. Depreciation is charged to the fixed assets to reduce their carrying amount as their value is consumed over time. This expense is of recurring in nature.

For example, a company purchased an asset worth $2,00,000 and charges 10% depreciation every year for 10 years. Since, the company will charge 10% depreciation every year it is recurring in nature and hence, should be considered as revenue expenditure.

- Purchase of raw material: Raw materials are materials used in primary production for the manufacturing of goods. These are needed on a regular basis and the cost of purchasing them is recurring in nature. Hence, they are classified under revenue expenditure.

For example, a manufacturing company orders stock of its raw material every quarter. Here, the company is going to reorder stock in every quarter and hence, this will be a revenue expenditure.

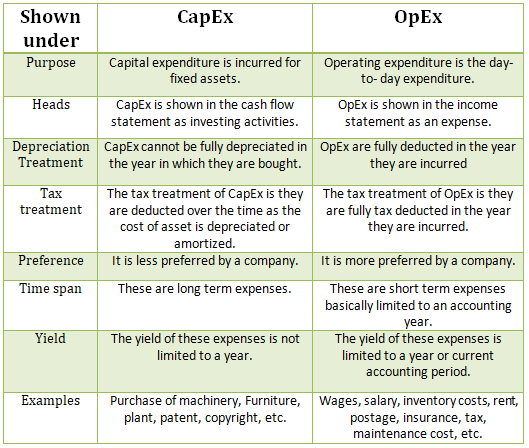

Capital expenditure can be capitalized as a part of non-current assets. Revenue expenditure cannot be capitalized and must be expensed in the statement of profit and loss.

See less

Capital Expense Capital expenses are incurred for acquiring assets including incidental expenses. Such expenses increase the revenue earning capacity of the business. These are incurred to acquire, upgrade and maintain long term assets such as buildings, machines, etc and are non-recurring in natureRead more

Capital Expense

Capital expenses are incurred for acquiring assets including incidental expenses. Such expenses increase the revenue earning capacity of the business. These are incurred to acquire, upgrade and maintain long term assets such as buildings, machines, etc and are non-recurring in nature.

Revenue Expenses

Revenue expenses are incurred to carry on operations of an entity during an accounting period. Such expenses help in maintaining the revenue earning capacity of the business and are recurring in nature.

These include ordinary repair and maintenance costs necessary to keep an asset working without any substantial improvement that leads to an increase in the useful life of the asset.

Suppose, company Takeaway ltd. purchases machinery for 50,000 and pays installation charges of 10,000. Salary of 15,000 is paid to the employees and existing machinery is painted costing 8,000. Here, the cost of machinery 50,000 and installation charges of 10,000 are treated as capital expenditure and the salary of 15,000 and painting cost of 8,000 is treated as revenue expenditure.

Identification

Points to categorize an expenditure as Capital or Revenue are as follows:

For example, a company Motors ltd. purchases furniture for 65,000, repays loans amounting to 1,00,000 and pays salary of 25,000.

Here the company creates an asset of 65,000 and reduces liability by 1,00,000 as shown below and therefore is considered as capital expenditure.

However, payment of salaries neither creates assets nor reduces liability. It only reduces profits and therefore is considered as revenue expenditure.

For example, a company Stars ltd purchases machinery for 1,20,000, furniture for 35,000 and has a rental expense of 80,000.

Here, the purchase of machinery is capital expenditure since it results in higher expense. However, the purchase of furniture cannot be regarded as a revenue expense and payment of rent cannot be regarded as a capital expense only because the rental expense is higher than the amount expended for the purchase of furniture.

For example, a company Caps ltd. purchases land for 1,00,00,000 on an equal monthly installment basis. Then such payments cannot be considered as revenue expense only because the payments are recurring. Since the installments are paid in lieu of the purchase of land which is a long term asset, the payments will be considered as capital expenditure.

For example, a company Marks Ltd. purchases machinery directly from the manufacturer for 50,000. For the manufacturer, the proceeds from the sale of machine are revenue in nature but the amount expended by Marks Ltd. will be categorized as capital expenditure.

Following conclusion can be inferred from the above explanation:

*Such transactions may or may not hold true as explained above.

See less