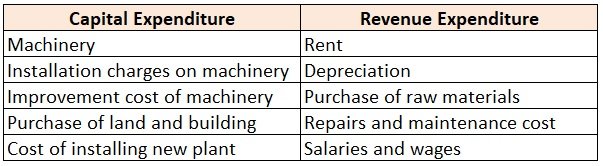

Capital Expenditure: Capital expenditure is the expenditure incurred by an entity or organization to acquire or purchase a fixed asset. This expenditure forms part of non-current assets. The fixed asset is not expensed at the time of purchase instead, it is depreciated or amortized over its useful lRead more

Capital Expenditure:

Capital expenditure is the expenditure incurred by an entity or organization to acquire or purchase a fixed asset. This expenditure forms part of non-current assets. The fixed asset is not expensed at the time of purchase instead, it is depreciated or amortized over its useful life.

Example of Capital Expenditure:

- Machinery: Machinery is a tangible non-current asset purchased by a company for business purposes. Since it is a non-current asset company will be using it for more than one accounting period hence, it should be capitalized in the balance sheet under the head assets. Capitalization is a method in which cost is included in the value of the asset and expensed over its useful life.

For example, XYZ Ltd purchased machinery worth $1,00,000 and its useful life is 10 years.

In this case, XYZ Ltd will capitalize the amount of machinery because it will be using it for more than one accounting year. Any asset used for more than one accounting year should be capitalized.

- Installation charges on machinery: This expense is incurred while installing machines in the business premises and is a one-time expenditure. The whole amount of installation will be capitalized along with the cost of machinery in the balance sheet.

In the above example cost of the machine is given as $1,00,000 and at the time of installation company incurred a further expenditure of $10,000. Here, the company will add the amount of installation with the cost of machinery because the installation charge is a one-time expense. The total cost of the machine will be $1,10,000.

- Improvement cost of machinery: Any cost incurred in the improvement of the machine will be capitalized. It is so as it will improve the quality or extend the life of the machinery. Hence, this cost should be added to the historic cost of the machine.

In the above example, after installation charges were incurred historic cost of the machine was $1,10,000. After a few years, the company made some improvements to the machine which amounted to $20,000 and the machine’s useful life was extended to more 5 years.

The improvement cost of $20,000 will be added to the historical cost of $1,10,000. The total amount of $1,30,000 ($1,10,000+$20,000) will be shown in the balance sheet.

Revenue Expenditure:

Revenue expenditure is expenditure incurred for the purpose of trade or to maintain non-current assets. These are short-term expenses and consumed within one accounting year and also known as operating expenses.

Examples of Revenue Expenditure:

- Rent: It is an expense paid by the company for using the premises for business purposes to the owner of the premises. It is recurring in nature and hence, should be classified under revenue expenditure.

For example, a company rented premises for business purposes and paid a monthly rent of $10,000. This expenditure of $10,000 incurred will fall under revenue expenditure because the company is incurring this expenditure monthly.

- Depreciation: Depreciation is a non-cash expense and it is added back to the cash flow statement, alongside other expenses. This expense is incurred as a basis of consuming a portion of fixed assets for the current period. Depreciation is charged to the fixed assets to reduce their carrying amount as their value is consumed over time. This expense is of recurring in nature.

For example, a company purchased an asset worth $2,00,000 and charges 10% depreciation every year for 10 years. Since, the company will charge 10% depreciation every year it is recurring in nature and hence, should be considered as revenue expenditure.

- Purchase of raw material: Raw materials are materials used in primary production for the manufacturing of goods. These are needed on a regular basis and the cost of purchasing them is recurring in nature. Hence, they are classified under revenue expenditure.

For example, a manufacturing company orders stock of its raw material every quarter. Here, the company is going to reorder stock in every quarter and hence, this will be a revenue expenditure.

Capital expenditure can be capitalized as a part of non-current assets. Revenue expenditure cannot be capitalized and must be expensed in the statement of profit and loss.

See less

Let us begin with a short explanation of what opening balance is: The opening balance is the amount of funds that are bought forward from the end of one accounting period to the beginning of a new accounting period. In a firm’s account, the first entry done is of the opening balance. It can either hRead more

Let us begin with a short explanation of what opening balance is:

The opening balance is the amount of funds that are bought forward from the end of one accounting period to the beginning of a new accounting period.

In a firm’s account, the first entry done is of the opening balance. It can either have a debit balance or a credit balance depending upon whether the firm has a negative or positive balance.

Opening balance of a ledger

Opening balance is the first entry of the ledger account at the beginning of an accounting period.

In the case of a newly started business, there will be no closing balances and as such there will be no balances to be carried forward. In such a case, the investment and capital of the business will be entered as an opening balance for the current accounting period.

So the first and foremost part is to identify on which side of the ledger i.e. the debit side or the credit side the opening balance is to be entered.

For Example, A trial balance is given which represents the debit and credit balances, accordingly, I will prepare different ledger accounts to make it simpler.

As the Furniture is an Asset account, the opening balance will be on the debit side of the ledger account.

As Sundry creditor is a credit account, we put the opening balance on the credit side.

As the Capital is a credit account, we put the opening balance on the credit side.

As Wages is a debit account, we put the opening balance on the debit side.

As the Discount received is a credit account, we put the opening balance on the credit side.

Exception

Drawing Account.

Drawing account is an exception to this topic. It is considered a contra account to the owner’s capital account because it reduces the value of the owner’s equity. Drawings, therefore, have no opening balance.

Contra Entry.

Contra entry involves transactions of cash and bank. Any entry which involves both the cash and bank is contra entry.

For example, we deposit cash 5000 into the bank.

Accounting entry for this transaction would be

In this case, the ledger entry would be

As the bank account has a debit balance, the opening balance would come on the debit side.

As the cash account has a credit balance, the opening balance would come on the credit side.

Alternatively, If we withdraw cash 5000 from the bank.

Accounting entry would be

In this case, the ledger entry would be

As the Cash account has a debit balance, the opening balance would come on the debit side.

As the Bank account has a credit balance, the opening balance would come on the credit side.

See less