Let us begin with a short explanation of what Calls-in-Advance is: Whenever a company accepts money from its shareholders for calls not yet made, then we call it calls-in-advance. To put it in even simpler terms, it is the amount not yet called up by the company but paid by the shareholder. An imporRead more

Let us begin with a short explanation of what Calls-in-Advance is:

Whenever a company accepts money from its shareholders for calls not yet made, then we call it calls-in-advance. To put it in even simpler terms, it is the amount not yet called up by the company but paid by the shareholder. An important thing to note here is that a company can accept calls-in-advance from its shareholders only when authorized by its Articles of Association.

Calls-in-advance is treated as the company’s liability because it has received the money in advance, which has not yet become due. Till the amount becomes due, it will be treated as a current liability of the company.

The journal entry for recording calls-in-advance is as follows:

The money received from the shareholder is an asset for the company and therefore Bank A/c is debited with the amount received as calls-in-advance. The calls-in-advance A/c is credited because it is a liability for the company.

Since Calls-in-Advance is a liability, it is shown in the Equities and Liabilities part of the Balance Sheet under the head Current Liabilities and sub-head Other Current Liabilities.

For better understanding, we will take an example,

ABC Ltd. made the first call of 3 per share on its 10,00,000 equity shares on 1st May. Max, a shareholder, holding 5,000 shares paid the final call amount 2 along with the first call money. Now let me show the journal entry to record calls-in-advance.

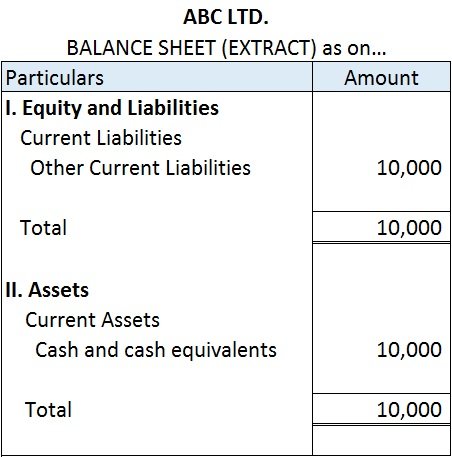

In the Balance Sheet, I will show calls-in-advance in the following manner,

The calls-in-advance of 10,000 is shown under the Equities and Liabilities side of the balance sheet under the head current liabilities and sub-head other current liabilities. It will be shown as a liability till the final call money becomes due. The amount received by the company from Max is shown on the Assets side of the balance sheet under head current assets and under the sub-head cash and cash equivalents.

See less

What is Inventory? Inventory refers to the stock of goods or raw materials a business uses to produce the final goods sold to the customers. What is the Inventory Turnover Ratio? Inventory Turnover Ratio is the financial ratio that shows how efficiently a business sells and replenishes its inventoryRead more

What is Inventory?

Inventory refers to the stock of goods or raw materials a business uses to produce the final goods sold to the customers.

What is the Inventory Turnover Ratio?

Inventory Turnover Ratio is the financial ratio that shows how efficiently a business sells and replenishes its inventory. It shows how well a business manages its inventory.

Inventory Turnover ratio is calculated as follows:

Inventory Turnover Ratio = Cost of goods sold / Average Inventory

where Average Inventory = (Inventory at the beginning of the year + Inventory at the end of the year) / 2

If inventory turnover is high, it means products are selling quickly. But if it’s too high, the company might not have enough stock, leading to fewer sales.

If turnover is low, there are slow sales or too much stock. That can lead to higher storage costs and obsolete products. It is important to find the right balance between the two.

Why is the Cost of Goods Sold taken as a numerator instead of revenue while calculating the Inventory Turnover Ratio?

The cost of goods sold is the sum of all the direct costs involved in the production of goods. On the other hand, Revenue is the total amount of money earned through the sale of goods and services.

The cost of goods sold (COGS) includes materials, labor, and overhead costs. Inventory consists of these costs and hence, it is better to take (COGS) as the numerator.

Revenue, however, considers things like markups, discounts, and other adjustments that don’t directly relate to the actual cost of inventory.

Let us understand it better with the help of an example:

Suppose the opening inventory is 20,000 and the closing inventory is 10,000. Average inventory can be calculated as (20,000 + 10,000)/2 = 15,000.

If the cost of goods sold is 45,000 the Inventory turnover ratio comes out to be 45,000/15,000 = 3.

On the other hand, if the revenue of 60,000 is taken as the numerator, the Inventory turnover ratio comes out to be 60,000/15,000 = 4

A high inventory turnover ratio shows that the inventory is moving faster than it is which is misleading for the stakeholders.

Hence, the Cost of goods sold is taken as the numerator for the calculation of the Inventory turnover ratio.

See less