Tally ERP does not have a voucher for recording closing stock journal entries. It automatically calculates closing stock and reports it in the Profit and Loss account and Balance sheet. However, Tally do have vouchers through which you can adjust the closing stock to be shown at the end of the year.Read more

Tally ERP does not have a voucher for recording closing stock journal entries. It automatically calculates closing stock and reports it in the Profit and Loss account and Balance sheet.

However, Tally do have vouchers through which you can adjust the closing stock to be shown at the end of the year.

Explanation

Tally, as we know is an ERP which can automate many aspects of accounting like calculation of ledger balance, creation of trial balance, financial statements and other reports. Only the data entry in vouchers is done manually.

Tally also calculates closing stock automatically because it already has the required data to do so.

Closing stock = Opening stock + Purchase – Cost of goods sold.

Using the above formula, Tally automatically calculates the closing stock.

But it may happen that the closing stock as per Tally and closing stock as per physical verification of stock do not match.

This may be due to damaged caused to some items of inventory or even theft of inventory items which is usually discovered when stock is physically checked and counted at the end of the financial year.

In that case, we can use the Physical Stock voucher to correct our closing stock in Tally.

Physical Stock Voucher

A physical Stock voucher is an inventory voucher which is used to adjust the amount of closing stock as per the physical stock verified at the end of the year.

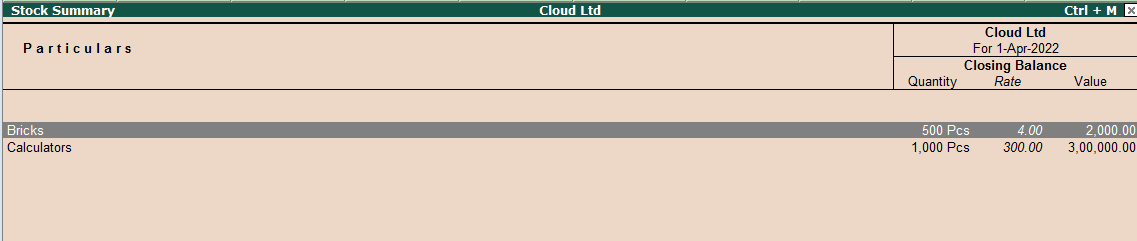

Suppose, if the closing stock for Bricks is 500pcs. Like in my stock summary, the item ‘Bricks’ is shown in the image below:

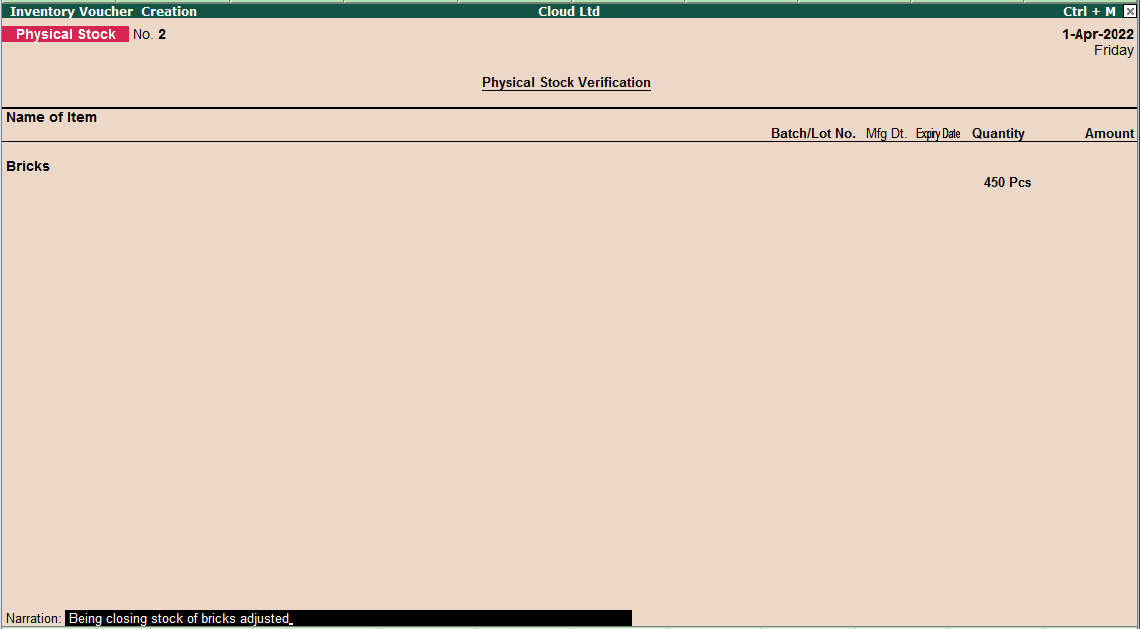

But after physical verification, it was found that there around there are only 450pcs of whole bricks are there. The rest of the bricks were broken.

To rectify this, we will open a Physical Stock voucher.

The steps to open a Physical stock voucher are as follows:

In Tally ERP 9 : Gateway of Tally → Accounting Vouchers → Press Alt + F10

In the physical stock voucher, we will select the stock item and enter the correct quantity, which is 450pcs.

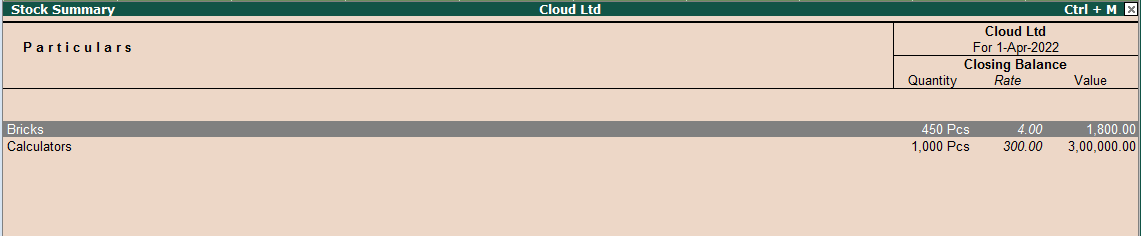

After entering the details above, accept the voucher and open the stock summary again from Gateway of Tally. It will show the Bricks at 450pcs.

Hence, this is how we can adjust our closing stock in Tally.

See less

Introduction & Definition Firstly, let's see what the term 'petty cash book' means. The word ‘petty’ means small. A petty cash book is identical to a cash book, maintained to record the small expenses of a business like stationery, postage, stamps, carriage, etc. The cash received by a petty casRead more

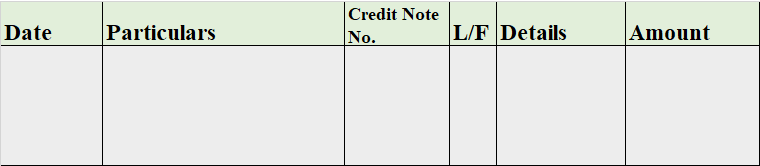

Introduction & Definition

Firstly, let’s see what the term ‘petty cash book’ means. The word ‘petty’ means small. A petty cash book is identical to a cash book, maintained to record the small expenses of a business like stationery, postage, stamps, carriage, etc. The cash received by a petty cashier is recorded on the debit/ receipt side whereas, the money he pays is recorded on the credit/ payment side. The difference between the sum of the debit and credit items represents the balance of the petty cash in hand.

The reason the petty cash book is maintained is that it records small expenses that are inconvenient or too small to be registered in the cash book. This is also called a simple petty cash book. Just like a cash book is maintained by the accountant, the petty cash book is maintained by a petty cashier.

When it comes to the format, there are two types of petty cash book formats. They are-

We have been discussing the simple petty cash book so far. Thus,

Format of Simple Petty Cash Book

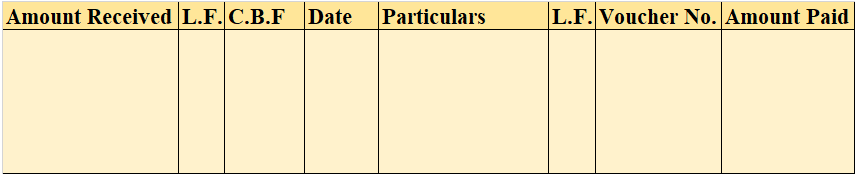

Analytical Petty Cash Book

The analytical petty cash book has numerous columns for the recording of monetary transactions. In the analytical petty cash book, there are pre-existing columns for the usual expenses that are recorded frequently in the business which makes it easier for a business that has daily expenses for food, stationery, postage, etc. They’ll be having individual columns. It has numerous columns in it for the recording of expenses in it.

The key advantages of an analytical petty cash book are-

Format of Analytical Petty Cash Book

See less