Brief Introduction Alternate Minimum Tax or AMT as the name suggests, is an alternate tax that an assessee has to pay, subject to certain conditions, instead of the income tax liability which is computed as per normal provisions of the Income-tax law. Alternate Minimum Tax is levied to impose higherRead more

Brief Introduction

Alternate Minimum Tax or AMT as the name suggests, is an alternate tax that an assessee has to pay, subject to certain conditions, instead of the income tax liability which is computed as per normal provisions of the Income-tax law.

Alternate Minimum Tax is levied to impose higher tax liability on non-corporate assessees who have claimed various profit-link deductions or investment-linked deductions in the relevant previous year.

My answer is based on the Indian Income law i.e. Income Tax Act, 1961.

The concept behind Alternate Minimum Tax

Let’s start our discussion with MAT i.e. Minimum Alternative Tax. It applies to corporate entities or companies.

Before MAT, it was seen that companies used to declare huge dividends to their shareholders. But when it came to filing income tax returns, they used to claim various profit linked and investment-linked deductions to report very low profits and even losses to arrive at negligible tax or nil tax whereas their financial statements would report huge profits.

It is true that the government provides such profit linked or investment linked deductions to encourage business and investments, but it also needs a sufficient and regular flow of revenue in the form of tax to fund its expenditure.

Hence, to prevent misuse of deductions to evade taxes by corporates, government introduce Minimum Alternate Tax to charge such assessees a minimum rate of tax.

Alternate Minimum Tax is the same as Minimum Alternate Tax in terms of concept. The provisions related to AMT are given under section 115JC of the Income Tax Act, 1961.

Scope of AMT as per section 115JC

Alternate Minimum Tax applies to all non-corporate assessees who claimed have claimed

- Deduction claimed if any under Chapter VI-A from section 80H to 80RRB except section 80P

- Exemption under section 10AA

- Deduction under section 35AD (Investment-linked deduction)

However, there is a threshold limit for certain non-corporates.

By non-corporate assessees we mean:

- Individual

- Hindu Undivided Family (HUF)

- Firms (partnership firms)

- Co-operative societies

- Association of Persons (AOP)

- Body of Individuals (BOI)

- Artificial Juridical Person (AJP)

- Limited Liability Partnership (LLP)

AMT is applicable to all except

- Individuals

- HUF

- AOP

- BOP

- Artificial Juridical Person

If their total adjusted income does not exceed Rs 20,00,000 in the previous year.

Therefore, AMT is applicable to all other non-corporate assessees like LLP, firms and cooperative societies irrespective of their total adjusted income.

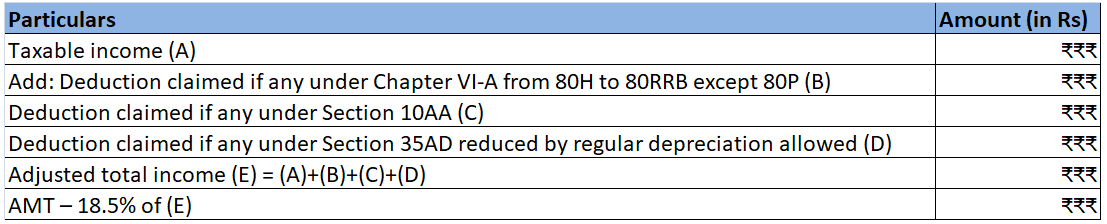

Calculation of Alternate Minimum Tax

The rate of AMT is 18.5% of the adjusted total income. This adjusted total income and the AMT on it is calculated in the following manner:

The higher of the following becomes the tax liability of the assessee:

- Alternate Minimum Tax calculated on adjustment income plus surcharges u/s 87A (4% Health and education cess)

- Income Tax calculated on taxable income (as per normal provisions)

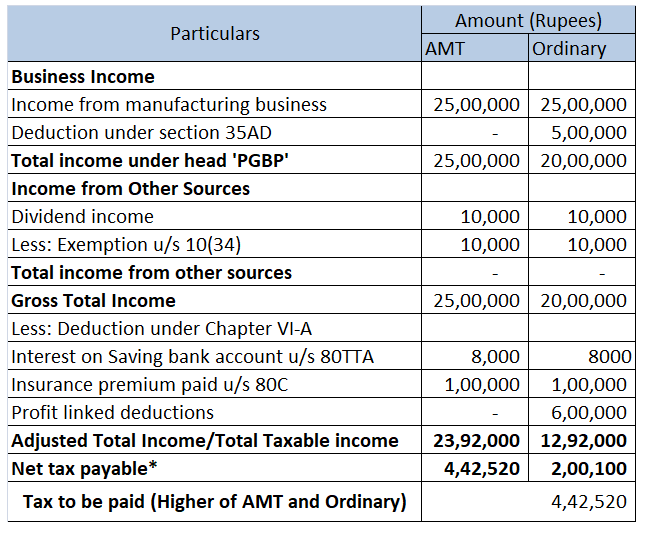

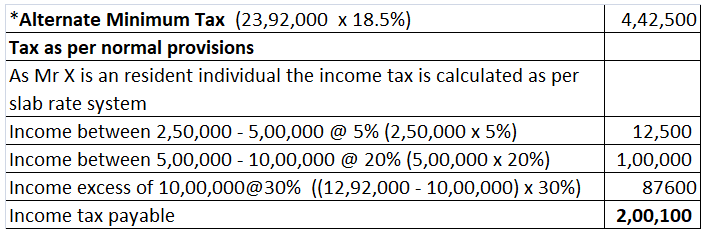

Numerical example

Mr X is a businessman who has earned the following income and expenditure in P.Y 2020-2021: (Amount in Rupees)

Income from manufacturing business 25,00,000

Interest on saving bank account 8,000

Dividend from ABC ltd 10,000

Insurance premium paid 1,00,000

Capital expenditure made as per section 35AD 5,00,000

Mr X is eligible to claim a profit linked deduction of Rs 6,00,000.

Also, the depreciation allowed (other than under 35AD) as per Income-tax Act,1961 amounts to Rs. 3,00,000.

Following is his computation of both AMT and Income tax liability as per normal provisions.

See less

Sales Return is shown on the debit side of the Trial Balance. Sales Return is also called Return Inward. Sales Return refers to those goods which are returned by the customer to the seller of the goods. The goods can be returned due to various reasons. For example, due to defects, quality differenceRead more

Sales Return is shown on the debit side of the Trial Balance.

Sales Return is also called Return Inward.

Sales Return refers to those goods which are returned by the customer to the seller of the goods. The goods can be returned due to various reasons. For example, due to defects, quality differences, damaged products, and so on.

In a business, sales is a form of income as it generates revenue. So, when the customer sends back those goods sold earlier, it reduces the income generated from sales and hence goes on the debit side of the trial balance as per the modern rule of accounting Debit the increases and Credit the decreases.

For Example, Mr. Sam sold goods to Mr. John for Rs 500. Mr. John found the goods damaged and returned those goods to Mr. Sam.

So, here Sam is the seller and John is the customer.

The journal entry for sales return in the books of Mr. Sam will be

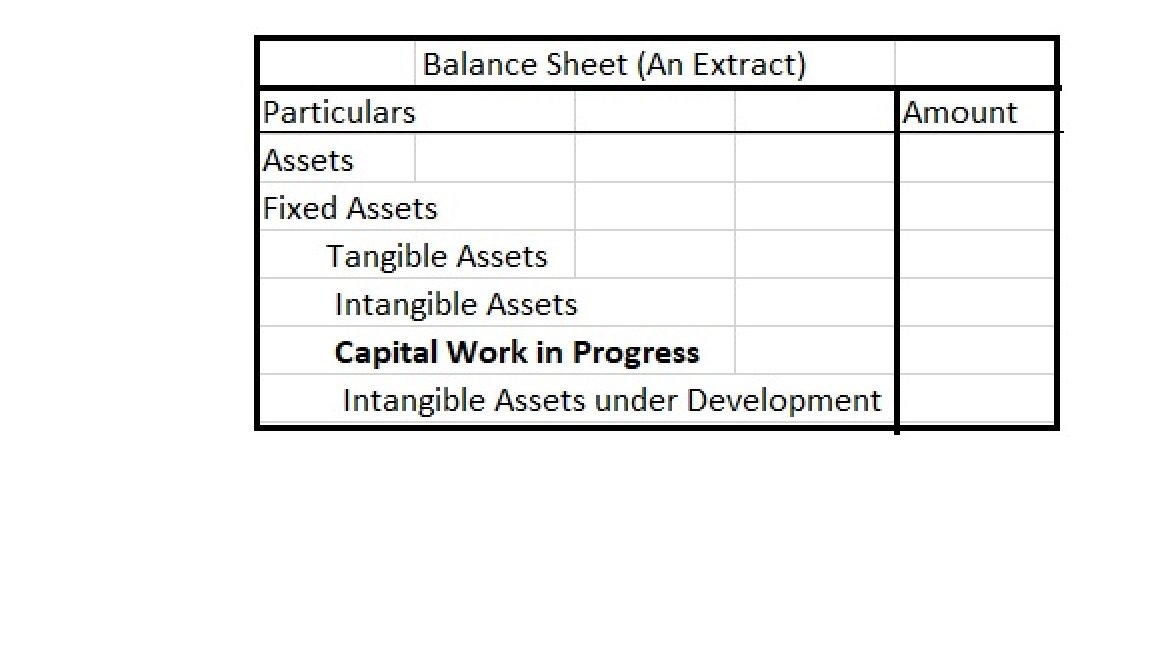

Treatment in Trial Balance

See less