Consignment is "goods sent by its owners to his agent for the purpose of sale". In simple language, the word consignment means to send goods to another person for sale on his behalf without transfer of ownership. In accounting terms, consignment is the process where the owner (consignor) transfers tRead more

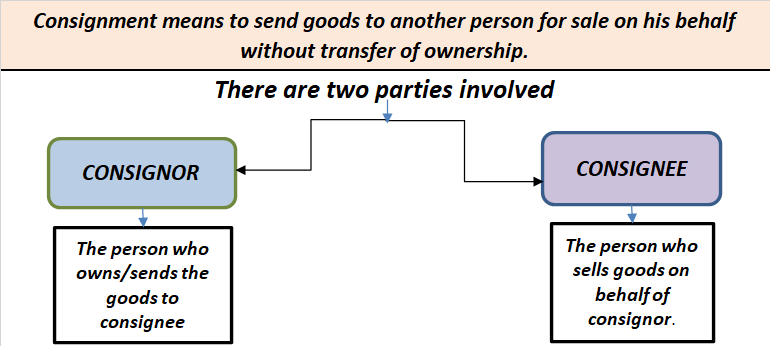

Consignment is “goods sent by its owners to his agent for the purpose of sale”. In simple language, the word consignment means to send goods to another person for sale on his behalf without transfer of ownership.

In accounting terms, consignment is the process where the owner (consignor) transfers the possession of the goods to the agent (consignee) to make a sale on his behalf while the ownership of goods remains with the owner until the sale is made by the agent. In return, the agent receives an agreed percentage of the sum in the form of commission.

Generally, there are two parties involved in consignment, those are as follows:

- CONSIGNOR: the person who is the owner and sender of goods.

- CONSIGNEE: the person who receives goods for sale/resale from the consignor in exchange for a percentage of the sale or on an agreed sum known as commission.

The relationship between consignor and consignee is that of principal and agent.

Let me give you a simple example of how consignment works.

Mr. John (consignor) sends goods to Mr. Jeh (consignee) worth Rs 20,000 to sell these goods at a cost plus 10%. Mr. Jeh agrees to sell these goods on his behalf for a commission of 1% on the sale. Therefore Mr. Jeh sold these goods at the agreed amount i.e Rs 22,000 [20,000+ 10% of 20,000] and charges Rs 220 [1% of Rs 22,000] as commission made on such sale and remit the remaining balance to the owner Mr. John.

There is a lot of confusion regarding “is consignment the same as the sale of goods?“. The answer is NO.

The reason what makes it different from the sale is

a) In sale the ownership gets transferred from seller to buyer but in case of consignment the ownership remains with the consignor until the sale is made by the agent.

b) In sale the risk gets transferred with the transfer of goods, whereas in consignment the risk remains with the owner till the sale is made.

c) Also goods once sold cannot be returned on damages /defaults, but in case of consignment goods that come to be faulty can be returned to the consignor.

Profits earned by a firm are not completely distributed to its owners, some of the profits are retained for various purposes. Reserves are profits that are apportioned or set aside to use in the future for a specific or general purpose. Reserves follow the Conservative Principle of accounting. ReveRead more

Profits earned by a firm are not completely distributed to its owners, some of the profits are retained for various purposes. Reserves are profits that are apportioned or set aside to use in the future for a specific or general purpose. Reserves follow the Conservative Principle of accounting.

Revenue reserve is created from the net profits of a company during a financial year. Revenue reserve is created from revenue profit that a company earns from the daily operations of the business.

Various types of reserves are:

Different parts of profit are apportioned to create a different reserve and those reserves can only be used for purposes as defined.

While accounting for Revenue Reserve, the profit decided to transfer to Revenue Reserve are first transferred to Profit and Loss Appropriation Account and then to Revenue Reserve Account. In the balance sheet, Revenue Account is shown under the Capital and Reserves head.

Uses of Revenue Reserve:

Example:

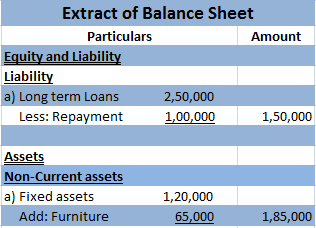

Given that Revenue Reserve Account stands at Rs 1,00,000 and the company wants to distribute Rs. 40,000 as dividend to its shareholders. The treatment of this transaction in the financial statements will be-

Particulars Amount (Rs.)

Revenue Reserve Account 1,00,000

(less) Dividend distributed (40,000)

The amount shown in Balance Sheet 60,000

See less