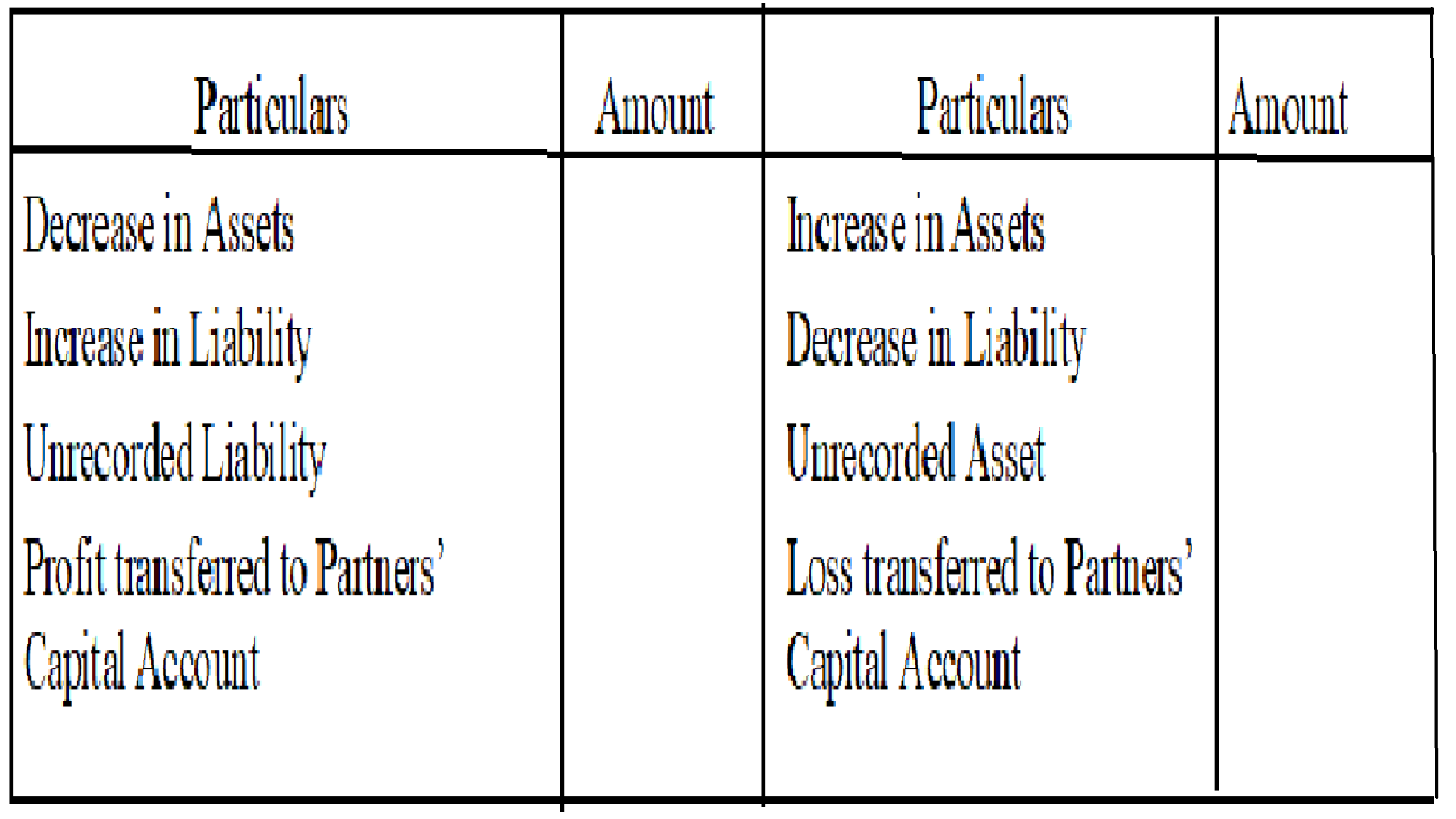

Unrecorded Assets are the assets that are completely written off but still physically available in the company or assets that are not shown in the books of the company. Unrecorded assets are generally recorded or recognized at the event of admission, retirement, death of a partner when all the assetRead more

Unrecorded Assets are the assets that are completely written off but still physically available in the company or assets that are not shown in the books of the company.

Unrecorded assets are generally recorded or recognized at the event of admission, retirement, death of a partner when all the assets and liabilities are revalued or dissolution of the firm.

Since Accounting Standards require firms to record all the assets and liabilities in their books, it is therefore mandatory to record such unrecorded assets.

There can be two cases for treatment of such unrecorded assets:

- Unrecorded Asset entered into the business and recorded in books

| Unrecorded Asset A/c (Dr.) | Amt | |

| To Revaluation A/c | Amt |

The unrecorded asset is now debited since it has to be recorded in the books now and Revaluation Account is credited since it is again for the business which will eventually be transferred to Partners’ Capital Account.

- Unrecorded Asset taken over by a partner and paid cash

| Cash A/c (Dr.) | Amt | |

| To Partners’ Capital A/c | Amt |

If a partner decides to take over an unrecorded asset then his account is credited with that amount and since cash paid by the partner comes into business Cash Account is debited.

- Unrecorded Asset discovered during Dissolution

| Cash/ A/c (Dr) | Amt | |

| To Realization A/c | Amt |

When an unrecorded asset is discovered during the dissolution of the firm, such an asset is sold directly to the outsider and as a result, cash A/c is debited since the cash is entering the business. The entry is made through the Revaluation A/c and it is hence credited.

Example:

At the time of revaluation, firms find a typewriter that has not been recorded in the books and is valued at Rs 10,000. The journal entry to record that typewriter will be:

| Typewriter A/c (Dr.) | 10,000 | |

| To Revaluation A/c | 10,000 |

See less

Today, mobile phones especially smartphones are an indispensable part of most businesses and they qualify as fixed assets as they usually last for more than a year. Being a fixed asset, the depreciation on mobile phones is to be provided. The rate of depreciation to be charged on mobile phones is 15Read more

Today, mobile phones especially smartphones are an indispensable part of most businesses and they qualify as fixed assets as they usually last for more than a year. Being a fixed asset, the depreciation on mobile phones is to be provided.

The rate of depreciation to be charged on mobile phones is 15% WDV* as per the Income Tax Act. The rates as per the companies act, 2013 are 4.75% SLM** and 13.91% WDV*.

*Written Down Value **Straight Line Method

A company has to charge depreciation on mobiles in their books as per the rates of Companies Act, 2013.

Any business or entity other than a company can choose the rate as per the Income Tax Act, 1961 which is 15% WDV. It is a general practice for non-corporates to charge depreciation in their books as per the rates of the Income Tax Act.

An important thing to know is that as per the Income Tax Act, 1961, mobile phones are treated as plants and machinery and the general rate of 15% is applied to it.

One may consider mobile phones as computers and charge depreciation at the rate of 40%. However, such a practice is not correct. Mobile phones are not considered equivalent to computers and there is case judgment given by Madras High Court which backs this consideration. The case is of Federal Bank Ltd. vs. ACIT (supra).

Therefore we are bound to this case judgment and should treat mobile phones as part of plant and machinery and charge depreciation on it accordingly for the time being.

See less