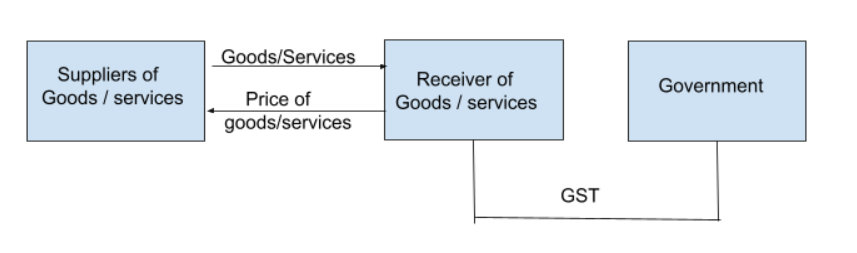

Goods and services tax (GST) is an indirect tax that was introduced in place of other indirect taxes like value-added tax, service tax, purchase tax, etc. It was introduced to ensure that only one tax would be applicable all over India. Reverse Charge is a mechanism where the liability to pay tax onRead more

Goods and services tax (GST) is an indirect tax that was introduced in place of other indirect taxes like value-added tax, service tax, purchase tax, etc. It was introduced to ensure that only one tax would be applicable all over India. Reverse Charge is a mechanism where the liability to pay tax on goods and services lies on the recipient instead of the supplier.

APPLICABILITY

Reverse charge is applicable when:

- It is specified by the CBIC for the supply of certain goods and services.

- Goods are supplied by an unregistered dealer to a registered dealer.

- There is a supply of services through an E-commerce operator.

TIME OF SUPPLY

As per reverse charge in the case of goods, the time of supply is the earliest of the three:

- Date of receipt of goods

- Date of payment

- The date is immediately after 30 days from the date of issue of invoice from the supplier.

For example, If goods were received by the supplier on 15th June, and the date of the invoice was on 3rd July but the date of entry in the books of the receiver was 25th June, then the time of supply of goods would be on 15th June.

As per reverse charge in the case of services, the time of supply is the earliest of the two:

- Date of payment.

- Date immediately after 60 days from the date of issue of invoice by the supplier.

For example, if the date of payment of services provided was on 16th July, and the date of issue of the invoice was on 15th May ( 60 days from 15th May is 14th July), then the time of supply of services would be 14th July.

See less

External liabilities are the amounts which a business is obliged to pay to the outsiders (who are not owners of the business). Here is the list of external liabilities:- Accounts payable ( trade creditors and bills payables) Loan taken from outsiders Loan from bank Debentures Public deposits accepteRead more

External liabilities are the amounts which a business is obliged to pay to the outsiders (who are not owners of the business).

Here is the list of external liabilities:-

The list is not exhaustive.

Just for more understanding, internal liabilities are those liabilities which a business is supposed to pay back to its owners. Such as capital balance, profit surplus etc.

See less