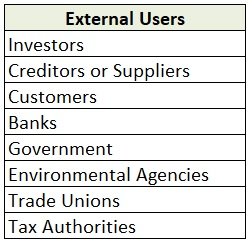

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization's activities. For example - Tax Authorities, Banks, Customers, Trade Unions, Government, Investors,Read more

External users are people outside the business or entity who use accounting information. They do not have a direct link with the organization but can influence or can be influenced by the organization’s activities.

For example – Tax Authorities, Banks, Customers, Trade Unions, Government, Investors, or Creditors.

External Users:

- Investors – Investors are interested in the past performance and future earnings of the business. They want to track the performance of their business whether it is giving them any benefit or not. A business’s past information helps investors in assessing their investments.

- Creditors or Suppliers – Some suppliers provide goods and services on credit, and before providing any credit they check the company’s ability to pay. Creditors are interested in the company’s liquidity i.e to see if a company can fulfill short-term obligations.

- Customers – Customers are more interested in a company’s financial statement as they rely on them for goods and services. They check the ability of the company whether it is providing them good quality goods and will continue to provide them in future.

- Banks – Banks are most likely interested in the liquidity and profitability of the company. They keep track of whether the company can pay the debt when it is due along with interest.

- Government – The company’s activities are central to the economy and must be met by them. The government controls a company’s actions if they break a law or damage the environment.

- Environmental agencies – They keep an eye on organizations whether their activities are harming the environment or not.

- Trade unions – They take an active part in the decision-making process. They want to see the financial statements of the company and want to decide the compensation of the employees they represent.

- Tax authorities – They determine whether the business has declared the correct amount of tax in its tax returns. They conduct audits of the tax returns to verify them with the accounting records disclosed.

Here is a summary of external users

The Realisation account is prepared at the time of dissolution of the Partnership firm to ascertain profit or loss from the sale of assets and payment of liabilities of the firm. All assets that can be converted into cash (i.e. from which any value can be realised) and all external liabilities thatRead more

The Realisation account is prepared at the time of dissolution of the Partnership firm to ascertain profit or loss from the sale of assets and payment of liabilities of the firm. All assets that can be converted into cash (i.e. from which any value can be realised) and all external liabilities that are to be paid are recorded in the Realisation A/c.

DISSOLUTION OF PARTNERSHIP FIRM

It means the firm closes down its business and comes to an end. Simply, it means the firm will cease to exist in the future. As the firm is closing down, it will sell all its assets to realise all the value blocked in the assets, it is liable to pay off all of its liabilities whether due now or on some future date, and the remaining amount (if any) is distributed among the partners.

REALISATION ACCOUNT

This account is prepared only once, at the time of dissolution of the Partnership firm. It is opened to dispose of all the assets of the firm and make payments to all the external creditors of the firm.

It ascertains the profit earned or loss incurred on the realisation of assets and payment of liabilities.

The Realisation account is a NOMINAL ACCOUNT (Debit all expenses and losses, Credit all incomes and gains)

ITEMS RECORDED IN THE REALISATION ACCOUNT

DEBIT SIDE OF REALISATION ACCOUNT

1. TRANSFER OF ASSETS

Assets are any property or the possession of the business enterprise that allows it to get cash or any other benefit in the future.

Since all assets are sold at the time of the dissolution, all assets that can be converted into cash are transferred to the Debit side of the Realisation A/c at their book values.

Such as Plant & Machinery, Building, Debtors, etc.

EXCEPTIONS

NOTE – If there is any provision against any asset, such as ‘Provisions for Bad debts’ or ‘Provision for Depreciation, then such assets are transferred to the Debit side of the Realisation A/c at its gross value and the Provision is transferred to the Credit side of the Realisation A/c.

For example – Suppose there are Debtors of $50,000 and the Provision for Doubtful Debts is $2,000.

Then, Debtors will be recorded on the Debit side with a value of $50,000 and the Provision for Doubtful Debt on the Credit side with the amount of $2,000.

2. PAYMENT OF LIABILITIES

All liabilities are either paid in cash or the Partner agrees to pay for some liabilities. Since they are expenses, they are recorded on the debit side of the Realisation A/c as “Debit all expenses and Losses”

3. PROFIT ON REALISATION

There is profit when Cr. side > Dr. side, as it means incomes are more than the payments made. This profit is distributed among the partners.

CREDIT SIDE OF THE REALISATION ACCOUNT

1. TRANSFER OF LIABILITIES

Liabilities refer to the amount owed by the firm to outsiders. All liabilities must be paid off before accounts are closed. So, all external liabilities are transferred to the Credit side of the Realisation account, to make their payment.

Such as creditors, bills payable, loans, outstanding expenses, partner’s wife’s loan, etc.

EXCEPTION (not included)

2. SALE OF ASSETS

Assets can be sold for cash or taken by the Partner. The amount received from the sale of assets is recorded on the credit side of the Realisation account as “Credit all incomes and gains”.

Also, if any asset is given to the creditors in part or full payment of his dues, then the agreed amount is deducted from the creditor’s claim and no other entry is passed.

3. LOSS ON REALISATION:

There is a loss, if the Dr. side> Cr. side, which means Expenses > Incomes. This loss is also distributed among the Partners.

See less