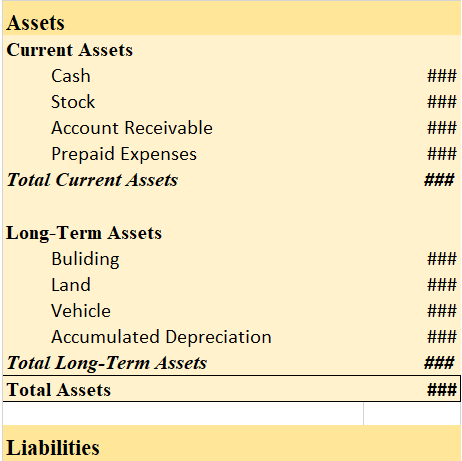

Land in the balance sheet The land is an asset and hence it is shown on the asset side of the balance sheet. On the asset side of the balance sheet, the land is stated under the heading long-term assets. Balance Sheet (for the year…) Explanation The land is a fixed asset and is supposed not to be caRead more

Land in the balance sheet

The land is an asset and hence it is shown on the asset side of the balance sheet.

On the asset side of the balance sheet, the land is stated under the heading long-term assets.

Balance Sheet (for the year…)

Explanation

The land is a fixed asset and is supposed not to be cashed, consumed, last, sold, or written off within one accounting year and is purchased for long-term use. The fixed assets are also called non-current assets and the reason behind it is that current assets are easily converted into cash within one year and they are not.

- The sole purpose of buying fixed assets like the land is that they are planned to be used for the long term in order to generate income.

- Examples of fixed assets – Land, buildings, furniture, plants & equipment, etc.

- Also called non-current assets and capital assets.

Why is it shown on the asset side?

The land is an asset, although it is not depreciable it is still considered to be an asset because just like other assets the business spends its own money to acquire it, and it gives them a long-term benefit while reselling it.

Therefore, the land is shown on the asset side under the fixed asset heading.

See less

Journal entry for commission earned but not received Commission earned but not received is called accrued income. As we know there are two types of accounting, cash basis of accounting, in which the transaction is recorded only when cash is received or paid, and accrual basis of accounting, in whichRead more

Journal entry for commission earned but not received

Commission earned but not received is called accrued income. As we know there are two types of accounting, cash basis of accounting, in which the transaction is recorded only when cash is received or paid, and accrual basis of accounting, in which even if money is yet to be accepted or paid, the transactions are still recorded.

E.g of accrual income- rent earned but not collected, interest on the investment earned but not received, etc.

Journal entry

Simplifying with an example

If the rent earned was $1,000 and it’s yet to be received, we’ll be passing this entry-

When it’s received, this entry is passed

See less