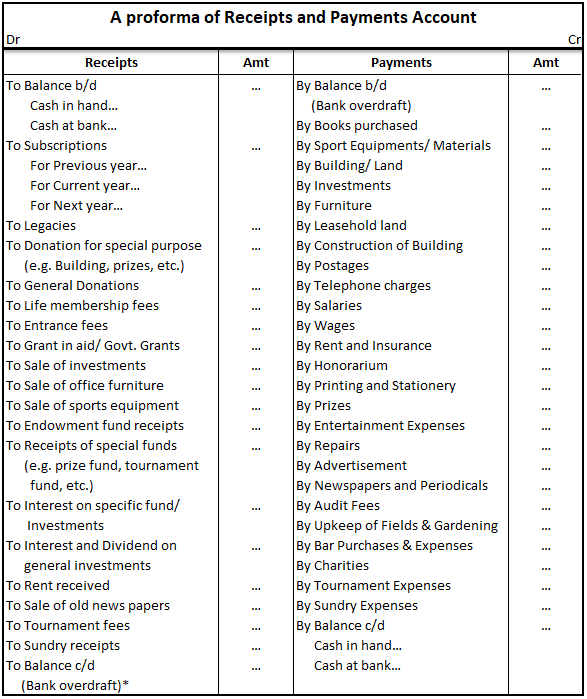

Receipts and payment account is a summary of cash transactions prepared at the end of the accounting period from the cash book where the transactions are recorded in chronological order. It is an Asset/ Real Account that records both revenue and capital receipts and payments. It is mainly prepared fRead more

Receipts and payment account is a summary of cash transactions prepared at the end of the accounting period from the cash book where the transactions are recorded in chronological order. It is an Asset/ Real Account that records both revenue and capital receipts and payments. It is mainly prepared for non-profit organizations and helps in the preparation of final accounts.

Proforma

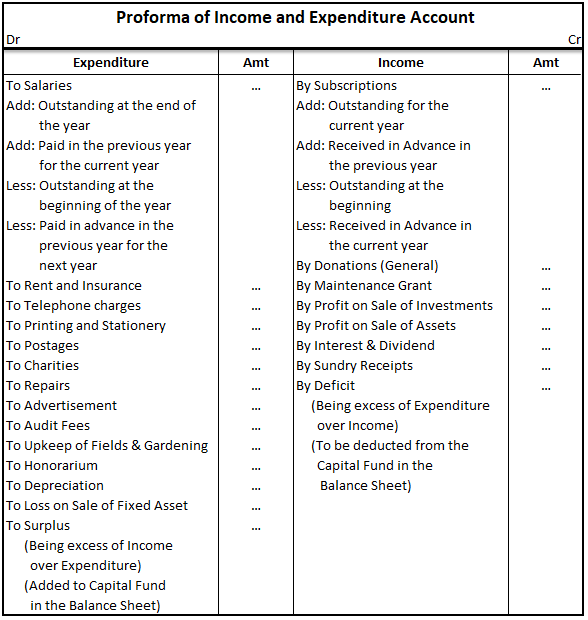

Income and Expenditure Account is an account prepared by not-for-profit organizations to see whether the income of a particular period is sufficient to cover the expenses of that period. If the revenue is more than the expenses, it is known as “Surplus” or “Excess of Income over Expenditure” and if the expenses are more than Income, it is known as “Deficit” or “Excess of Expenditure over Income”. The account is prepared on the accrual basis of accounting i.e. all revenue incomes whether received or not and all revenue expenditures of the period whether paid or not are taken into account. However, in case of surplus, the money is not distributed among the members. Similarly, if there is a deficit it is not borne by the members.

Proforma

The journal entry for the closing stock is passed at the year-end as closing stock is the inventory held by a business at the end of its accounting period. However, the entry for recording closing stock depends on how it is treated in the books of accounts. The two types of the accounting treatmentRead more

The journal entry for the closing stock is passed at the year-end as closing stock is the inventory held by a business at the end of its accounting period. However, the entry for recording closing stock depends on how it is treated in the books of accounts.

The two types of the accounting treatment of closing stock are as follows:

Closing stock is not shown in the Trial Balance:

As per this treatment, the closing stock is not shown in the Trial Balance because it is already a part of the purchases of the business. Showing it in the Trial Balance would lead to a double effect. This will not give us accurate profit/loss at the end of the year.

The closing stock is transferred to Trading A/c by passing a closing entry.

Closing stock is an asset. It is debited because there is an increase in the assets. Trading A/c is credited because of the Matching concept as the value of the closing stock is adjusted against the cost of goods sold.

At the end of the year, it is shown on the Asset side of the Balance Sheet, under the head Current Assets and sub-head Inventory.

For example,

ABC Ltd. at the beginning of the year had an opening inventory of 20,000. During the year, purchases worth 5,000 were made and goods worth 10,000 were sold. At the end of the year, the value of the closing stock will be 15,000 (20,000 + 5,000 – 10,000).

Now the closing stock worth 15,000 will be recorded through this journal entry:

Closing stock is shown in the Trial Balance:

This scenario is possible only when the closing stock is adjusted against purchases. By adjusting against purchases, the double effect of showing both purchases and closing stock in Trial Balance is eliminated.

The following entry is recorded to adjust closing stock against purchases.

Closing Stock is debited as there is an increase in the asset. Purchase A/c is credited because of the Matching concept.

After recording the adjustment entry, the closing stock is shown on the debit column of the Trial Balance. It is not shown in the Trading A/c as it is already adjusted against purchases. In the Balance Sheet, it is shown as a Current Asset.

See less