Credit Note A credit note is a document which generally evidences a sales return. It is created by the seller and sent to the buyer acknowledging the receipt of goods returned by the buyer. On the basis of it, the seller promises to pay back the buyer for the goods returned to him or adjust the amouRead more

Credit Note

A credit note is a document which generally evidences a sales return. It is created by the seller and sent to the buyer acknowledging the receipt of goods returned by the buyer. On the basis of it, the seller promises to pay back the buyer for the goods returned to him or adjust the amount in future transactions.

A credit note is also created when the buyer has sent excess money by mistake against the goods delivered to him.

In Tally, a credit note is created using a credit note voucher. Now, a credit note can only be created only if a sales entry has been made.

Hence first, we will be creating a sales entry and then the credit note.

Creation of sales entry in sales voucher ( If not done before)

The step to create a sale entry in Tally prime is as follows:

Gateway of Tally –> Vouchers –> Press F8 to open sales voucher

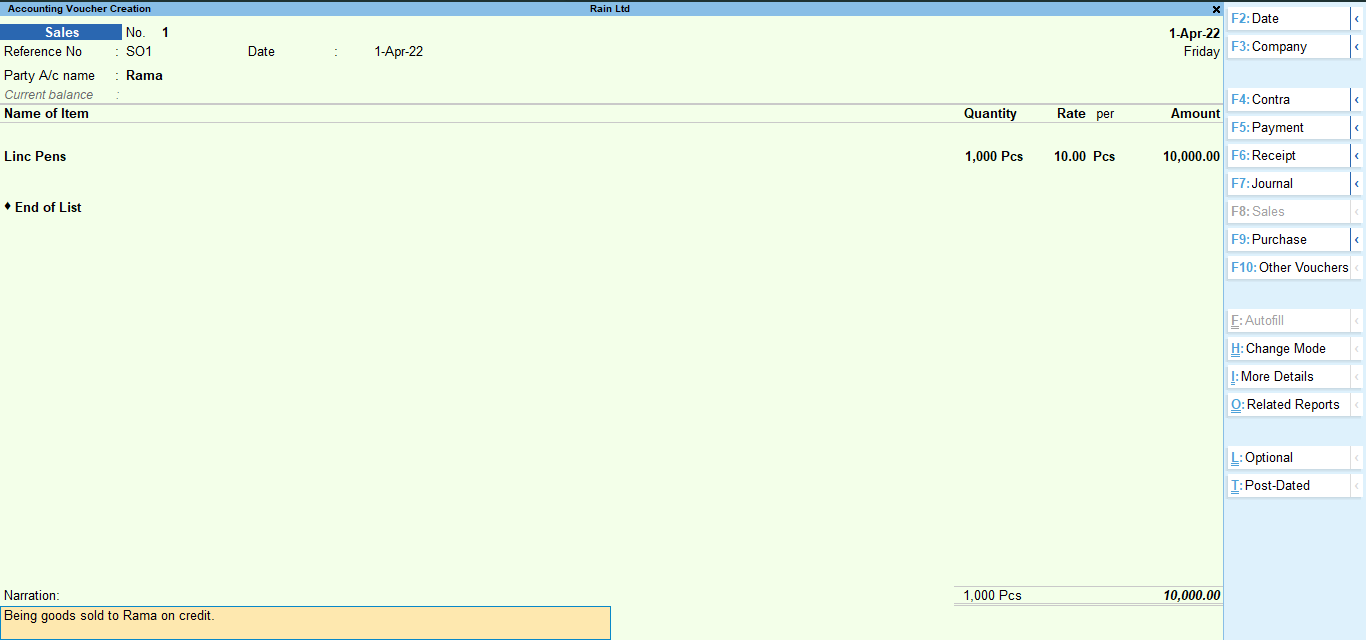

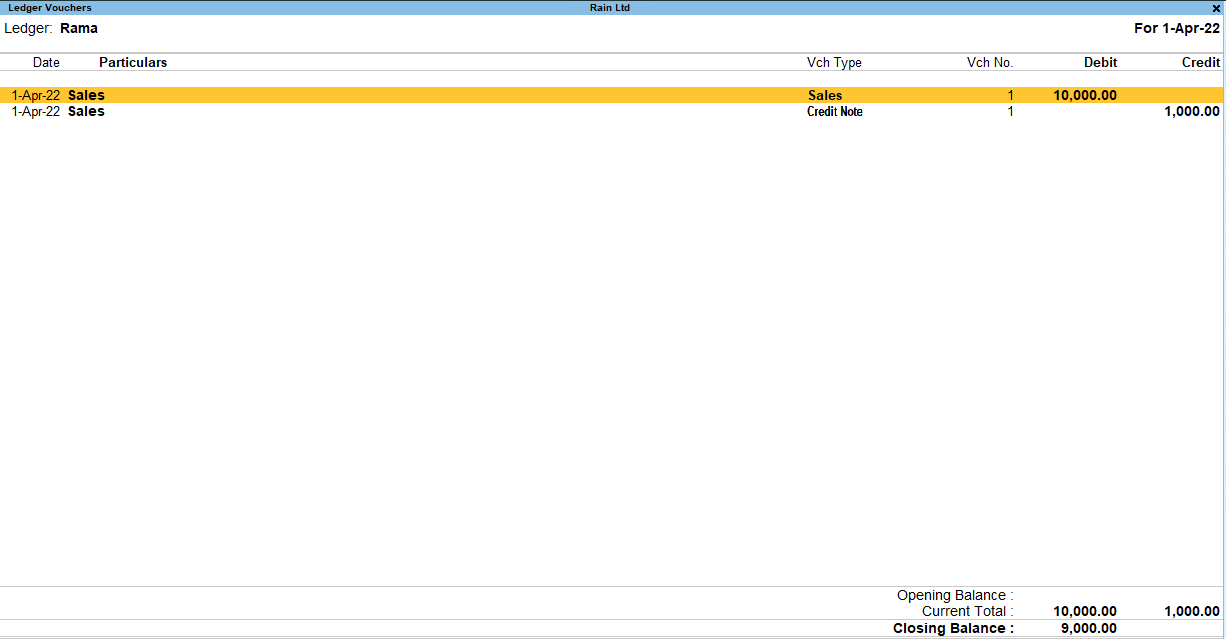

Enter the details of sales in the sales voucher like I have entered in my sale voucher and accept.

Here, my debtor is Rama and I have sold 1000pcs of Linc pens@Rs. 10 to him

Important things to consider:

- If no ledger accounts, stock items and stock units are created in your company, you can easily create them while in the voucher creation menu itself. Just press Alt + C in the field where you need to enter party name, stock item name or stock unit name and the respective creation menus will open.

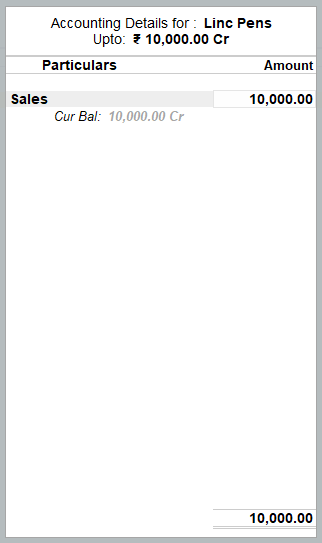

- After entering the item details, a new menu will open which will ask for which account to be credited for the sale entry. As we know, a sales account is credited, so you have select the sales account from the menu or simply create a Sales account if not created by pressing Alt + C. Below is that menu:

#2 Creation of credit note

If already in the voucher creation menu, just press Alt + F6 to open the credit note voucher.

Enter the party name and a menu will open, asking for a tracking number. No need to enter any details there.

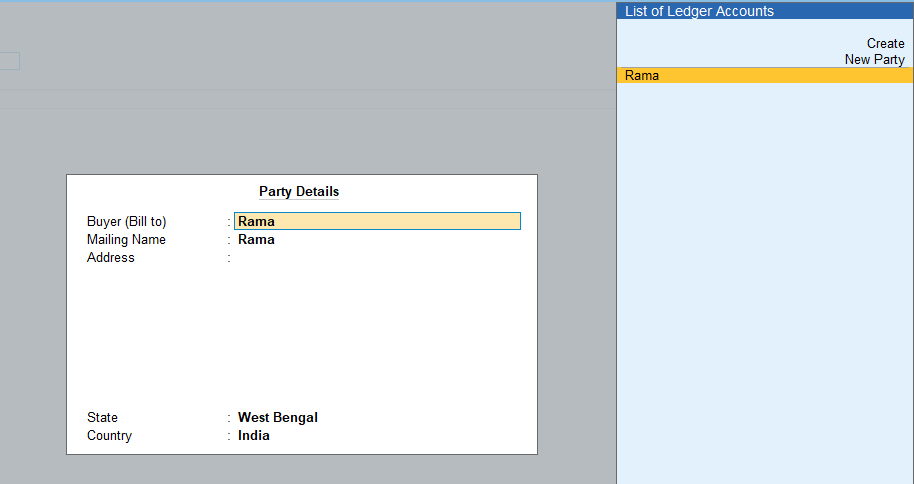

Next, another menu will open asking for party details. Select the name of the respective debtor.

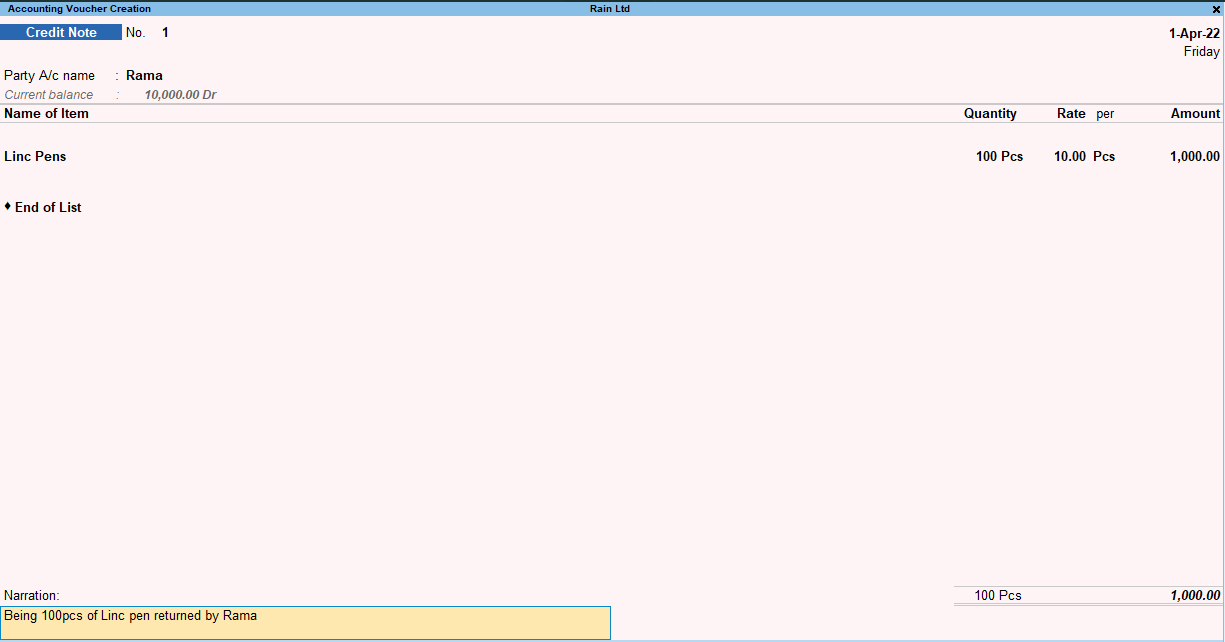

Next enter the details of stock items returned as I have done:

I have made a credit note for 100pcs of Linc pens returned by Rama.

After entering all the details, press Enter and accept.

You can verify the effect of this sales voucher by performing the following steps.

Gateway of Tally –> Display more reports –> Account Books –> Ledger –>Select the debtor account from the list of ledgers.

After opening the ledger, if you see that the debtor account is credited by an amount through a credit note voucher, then it can be said that you have performed the steps correctly.

Errors revealed by Trial Balance Trial balance, as we know, is a statement prepared after the ledger, followed by a journal. It has a list of all the general ledger accounts contained in the ledger of a business. Each nominal ledger account either holds a debit balance or credit. It is primarily useRead more

Errors revealed by Trial Balance

Trial balance, as we know, is a statement prepared after the ledger, followed by a journal. It has a list of all the general ledger accounts contained in the ledger of a business. Each nominal ledger account either holds a debit balance or credit.

It is primarily used to identify the balance of debits and credits entries from the transactions recorded in the general ledger in a certain accounting period. The debit and credit sides total are equal in a trial balance.

Classification of errors in the trial balance

Some of the common errors

Some more (commonly seen) errors while preparation of the trial balance:

Errors of Commission

Errors of Omission

Compensating Errors

Errors of Principles

See less