Definition The trial balance is a list of all the closing balances of the general ledger at the end of the year. Or in other words, I can say that it is a statement showing debit and credit balances. A trial balance is prepared on a particular date and not on a particular period. What does trial balRead more

Definition

The trial balance is a list of all the closing balances of the general ledger at the end of the year. Or in other words, I can say that it is a statement showing debit and credit balances.

A trial balance is prepared on a particular date and not on a particular period.

What does trial balance include?

As in each double-entry system, each account has two aspects debit and credit.

Hence the following trial balance includes:

• Debit or credit of the reporting period.

• The amount which is to be debited or credited to each account.

• The account numbers.

• The dates of the reporting period.

• The totaled sums of debits and credits entered during that time.

When we prepare a trial balance from the given list of ledger balances, these need to be included which are as follows :

The balance of all

• Assets accounts

• Expenses accounts

• Losses

• Drawings

• Cash and bank balances

Are placed in the debit column of the trial balance.

• The balances of

• liabilities accounts

• income accounts

• profits

• capital

Are placed in the credit column of the trial balance.

Importance

As the trial balance is prepared at the end of the year so it is important for the preparation of financial statements like balance sheets or profit and loss.

The purpose of the trial balance is as follows:

• To verify the arithmetical accuracy of the ledger accounts

This means trial balance indicates that equal debits and credits have been recorded in the ledger accounts.

It enables one to establish whether the posting and other accounting processes have been carried out without any arithmetical errors.

• To help in locating errors

There can be some errors if the trial balance is untallied therefore to get error-free financial statements trial balance is prepared.

• To facilitate the preparation of financial statements

A trial balance helps us to directly prepare the financial statements and then which gives us the right to not look or no need to refer to the ledger accounts.

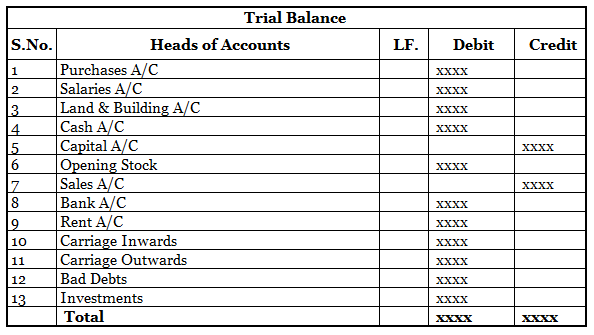

Structure of trial balance

Financial analysis of a company means analyzing the previous data of the company and giving recommendations based on that whether the company will improve in the future on not. It is the process of evaluating the financial performance and stability of the company. There are various types of financiaRead more

Financial analysis of a company means analyzing the previous data of the company and giving recommendations based on that whether the company will improve in the future on not.

It is the process of evaluating the financial performance and stability of the company.

There are various types of financial analysis. They are leverage, growth, cash flow, liquidity, profitability, etc.

The main objectives of Financial analysis are

1.Reviewing the current position: In order to know if the company is doing well, past analysis of data is required to be carried out. Regular recording of the transactions helps to understand the financial position of the company.

For example, A company wants to generate a revenue of 2000 crores in the next 5 years. The last four years’ data shows revenue as 1100, 1300,1600, 1800 crores respectively.

So from the above, we can say that the company is performing well and looks like it will reach the desired target in the fifth year or may perform better than the target desired.

However, if the revenue declines, it will cause concern for the team but the team will get time to gear up and work efficiently to achieve the desired target.

2. Ease in decision making: For Future decision-making, quarterly financials play an important role. Subsidiary books and accounts like the sales book, purchase orders, manufacturing a/c, etc. help in giving more reliable information.

For example, If sales are increasing inconsistently in a quarter, and in the next quarter the level of sales decrease due to any reason then the management can analyze and change the strategy.

3. Performance Comparison: It helps in comparing the performance of the business every month, quarterly, half-yearly, and yearly. Analyzing the data can help the management to compare if the company is proceeding in the right direction.

4. Assessing the profitability: Financial statements are used to assess the profitability of the firm. The analysis is made through the accounting ratios, trend line, etc. Accounting ratios calculated for a number of years shows the trend of change of position i.e. positive, negative or static. The assessing of the trend helps the management to analyze if the company is making profits or not.

5. Measure the solvency of the firm: Financial analysis helps to measure the short-term and long-term efficiency of the firm for the benefit of the Stakeholders.

6. Helps the end-users: The owners are the end-users for whom the financial statements are prepared. Financial statements are the summaries that are prepared for providing various disclosures to the owners which helps them understand the statements in a better way. If the end-users arrive at the right decision with the help of financial statements that means the objective is achieved.

7. Other objectives:

- It helps to settle disputes among the parties.

- It helps in the expansion decision of the firm.

- It helps in analyzing the amount of tax to be paid.

- It reduces the chances of fraud.

- It provides information about resources.

- It provides a true and fair view of financial position.

See less