Cash Stock in trade Furniture Advance Payment

Ledger posting As we know, a business records all of its transactions in the journal. After the transactions are recorded in the journal, they are posted in the principal book called ‘Ledger’. Transferring the entries from journals to respective ledger accounts is called ledger posting or posting toRead more

Ledger posting

As we know, a business records all of its transactions in the journal. After the transactions are recorded in the journal, they are posted in the principal book called ‘Ledger’. Transferring the entries from journals to respective ledger accounts is called ledger posting or posting to the ledger accounts. Balancing of ledgers is carried out to find differences at the year’s end.

Posting to the ledger account means entering information in the ledger, and respective accounts from the journal for individual records. The accounts that are credited are posted to the credit side and vice versa.

Ledger maintenance is done at the end of an accounting period and it’s maintained to reflect a permanent summary of all the journal accounts. In the end, all the accounts that are entered and operated in the ledger are closed, totaled, and balanced. Balancing the ledger means finding the difference between the debit and credit amounts of a particular account.

While posting to the ledger account, suppose goods were bought for cash. While passing the journal entry, we’ll be debiting the purchases a/c and crediting the cash a/c by stating it as, ‘To Cash A/c’.

Now, this entry will be affecting both the purchases account and the cash account. In the cash account, we’ll be debiting purchases. Whereas in the purchases account, we’ll be crediting the cash. That’s how it works in the double-entry bookkeeping system of accounting.

Example

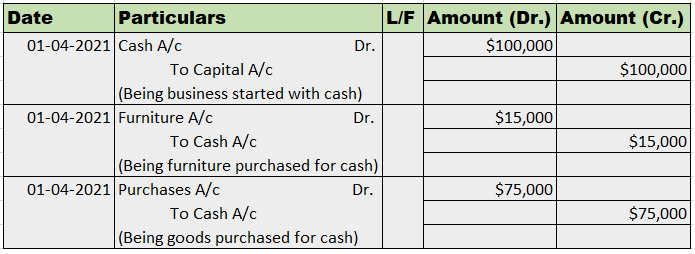

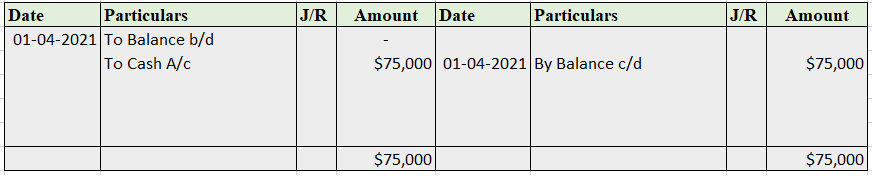

Mr. Tony Stark started the business with cash of $100,000 on April 1, 2021. He bought furniture for business for $15,000. He further purchased goods for $75,000.

Now, we’ll be journalizing the transactions and posting them into the ledger accounts.

Journal Entries

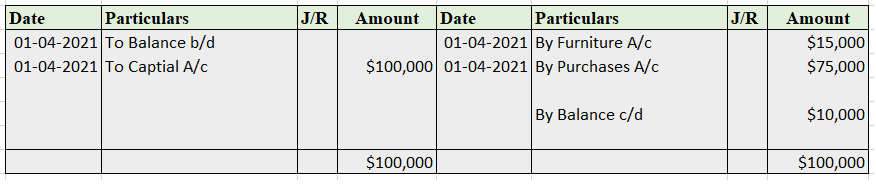

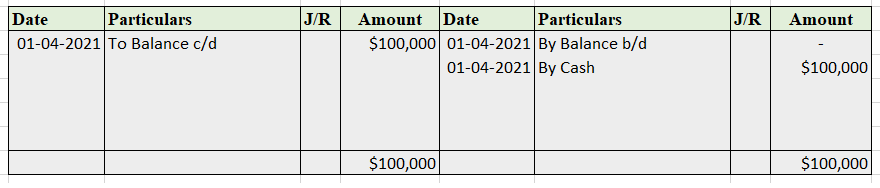

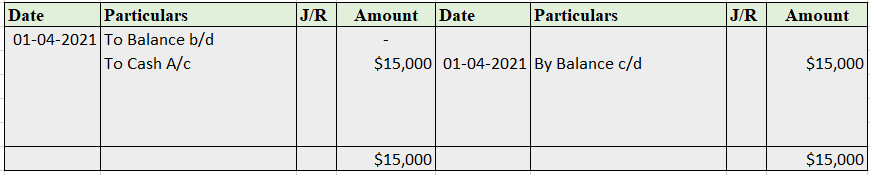

Posting to Ledger Account

Cash A/c

Capital A/c

Furniture A/c

Purchases A/c

See less

The correct option is 3.) The term current assets do not include furniture. Explanation A current asset is any asset that can reasonably be expected to be sold, consumed, or exhausted through the normal operations of a business within one accounting year. Thus, current assets don't have life for morRead more

The correct option is 3.)

The term current assets do not include furniture.

Explanation

A current asset is any asset that can reasonably be expected to be sold, consumed, or exhausted through the normal operations of a business within one accounting year. Thus, current assets don’t have life for more than a year.

Example: Cash and cash equivalent, stock, liquid assets, etc.

Furniture is expected to have a useful life for more than a year and they are bought for a long term by a company.

Cash is a more liquid asset of a company making it a more “current” asset. It requires no conversion and is spendable as it is. Thus, making it a vital current asset.

Stock in trade is a current asset because it can be converted into cash within one year and all the stock in trade of a company is expected to be sold within one accounting period and should not stick for a longer period.

Advance payment, on the other hand, is an amount paid to an employee, essentially a short-term loan by the employer. It’s recorded on the asset side of the balance sheet and as these assets are used, they are expended and recorded on the income statement for the period in which they are incurred, making it a short-term asset ending within an accounting year.

Thus, on the asset side of the balance sheet, we can clearly see which current assets are and which are not included in the current asset

Balance Sheet (As at…..)

Therefore, (3) Furniture, won’t be included in current assets.

See less