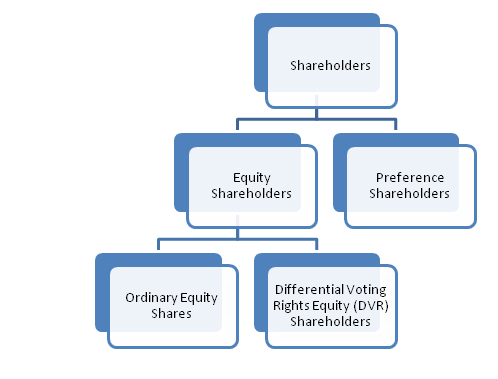

Shareholders are the entities that hold some amount or number of shares of a company. As we know that ownership of a company is divided into its shares, a shareholder is actually a part-owner of a company. By entity, it means a shareholder may be: An individual Any other company Any other incorporatRead more

Shareholders are the entities that hold some amount or number of shares of a company. As we know that ownership of a company is divided into its shares, a shareholder is actually a part-owner of a company.

By entity, it means a shareholder may be:

- An individual

- Any other company

- Any other incorporated entity

- Cooperative society

- BOI( Body of Individuals)

- AOP(Association of Persons)

- Artificial Juridical Person

The rights of shareholders depend on the type of shareholder one is.

Types of shareholders

1. Equity Shareholders: By the term ‘shareholders’ we usually mean equity shareholders. They are permanent in nature i.e. they are not repaid the money they have invested into the company until the company is liquidated or wound up. Equity shareholders have the following rights:

- Right to have a share in profits made by the company. The profit made by a company, when distributed to its equity shareholders is known as a dividend.

- Right to vote on all resolutions to be passed in the Annual General Meeting of a company.

- Right to get repaid in event of winding up of the company. However, they are paid after meeting the obligations of outsiders and of preference shareholders.

- Right to transfer ownership of the shares. A shareholder may sell its shares to some willing buyer and cease to be a shareholder of a company.

2. Preference Shareholders: They are shareholders who are given preference regarding:

- Dividend

- Repayment at time of winding up

Unlike equity shareholders, they are not of permanent nature. Preference shares are redeemable i.e. they are to be repaid after a period which cannot be more than 20 years from the date of allotment of such shares (as the Companies Act, 2013). Also, a company cannot issue irredeemable preference shares. The rights of preference shareholders are as follows:-

- By preference as to dividend, it means preference shareholders have the right to receive a fixed dividend as a certain percentage on the nominal value of the share and that too before equity shareholders are paid.

- Right to get repaid at the date of redemption.

- If the company get liquidated before redemption of the preference shareholder, then they have the right to get repaid before equity shareholders.

3. Differential Voting Rights Shareholders: These shareholders hold equity shares but with differential, right as to voting i.e. they may either have less voting rights or more voting right as compared to ordinary equity shares. Generally, DVR shares carry less voting power.

For example, a DVR shareholder gets 1 vote for 10 shares whereas an ordinary equity shareholder gets 10 votes for 10 shares i.e. one vote for every share. DVR shares issued to raise not only permanent capital but also prevent dilution of voting rights.

The rest of the right remains the same as the equity shareholders.

See less

General reserve is the part of profits or money kept aside to meet future uncertainties and obligations of the entity. General reserve is created out of revenue profits for unspecified purposes and therefore is also a part of free reserves. General reserve forms a part of the Profit & Loss ApprRead more

General reserve is the part of profits or money kept aside to meet future uncertainties and obligations of the entity. General reserve is created out of revenue profits for unspecified purposes and therefore is also a part of free reserves.

General reserve forms a part of the Profit & Loss Appropriation account and is created to strengthen the financial position of the entity and serves as a sources of internal financing. It is upon the discretion of the management as to how much of a reserve is to be created. No reserve is created when the entity incurs losses.

General reserve is shown in the Reserves & Surplus head on the liability side of the balance sheet of the entity and carries a credit balance.

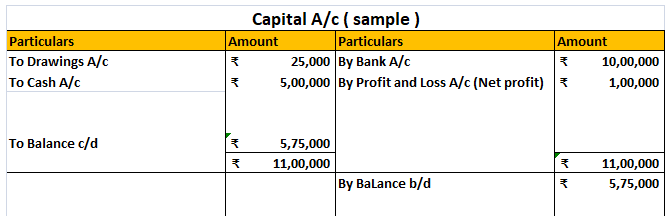

Suppose, an entity, ABC Ltd engaged in the business of electronics earns a profit of 85000 in the current financial year and has an existing general reserve amounting to 100000. The management decides to keep aside 20% of its profits as general reserve.

Then the amount to be transferred to general reserve will be = 85000*20% = 17000.

In the financial statements it will be shown as follows-

Now, in the next financial year, the entity incurs losses amounting to 45000. In this case, no amount shall be transferred to the general reserve of the entity and will be shown in the financial statement as follows-

The creation of general reserve can sometimes be deceiving since it does not show the clear picture of the entity and absorbs losses incurred.

See less