Meaning of lease A lease is an agreement or a contract in which the right to use an asset like land, building, or machinery is given by one party to the other party for a fixed period of time against the consideration of a single payment or a series of payments. There are two parties in a lease agreRead more

Meaning of lease

A lease is an agreement or a contract in which the right to use an asset like land, building, or machinery is given by one party to the other party for a fixed period of time against the consideration of a single payment or a series of payments.

There are two parties in a lease agreement:

- Lessor: The party who gives the right to use its asset in return for a series of payments or a single payment.

- Lessee: The party who receives the right to use the asset from the Lessor.

This is similar to a rent agreement or contract. The only difference between lease and rent is duration. A rent agreement is generally for less than 12 months while a lease agreement is for more than 12 months like 5 years or 10 years, sometimes even for like 99years.

Type of lease

There are two types of lease:

- Operating lease

- Finance Lease

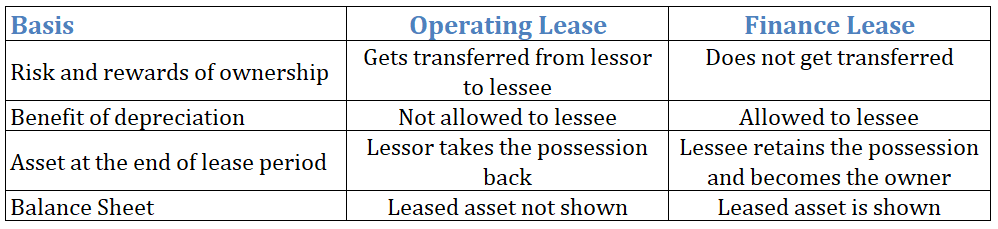

Operating lease

- An operating lease is a type of lease in which the possession of the leased asset is transferred back from the lessee to the lessor at the end of the lease period.

- Here, all the risk and rewards incident to ownership remains with the lessor, not the lessee.

- The depreciation on the leased asset in case of operating lease is not charged by the lessee to its profit and loss account as the leased asset is not shown in the balance sheet. A leased asset is an off-balance sheet item in the case of an operating lease.

Finance lease

- Unlike an operating lease, the ownership of the leased asset is transferred to the lessee at the end of the leased period.

- Thus, at the inception of the lease agreement, all the risk and rewards incident to ownership is transferred from the lessor to the lessee.

- The depreciation on the leased asset is charged by the lessee to its profit and loss account as the leased asset is shown in the balance sheet. A leased asset is a balance sheet item in the case of an operating lease.

- Along with the leased asset, the obligation to pay the future lease payment is also shown in the balance sheet as a non-current liability or current liability as the case may be.

Difference between operating lease and finance lease in tabular format

See less

Profitability ratios measure how profitable a company is and are used to assess its performance and efficiency. Based on the income statement and balance sheet of a company, these ratios are calculated. In terms of profitability ratios, there are several types, each providing a different viewpoint.Read more

Profitability ratios measure how profitable a company is and are used to assess its performance and efficiency. Based on the income statement and balance sheet of a company, these ratios are calculated.

In terms of profitability ratios, there are several types, each providing a different viewpoint.

The following are some common profitability ratios:

Gross profit margin: This ratio measures the percentage of revenue that remains after the cost of goods sold has been deducted. Producing and selling efficiently is indicated by this metric.

Net profit margin: An organization’s net profit margin is the portion of revenue left after all expenses have been deducted. A company’s profitability is measured by this indicator.

Return on assets (ROA): This ratio measures how profitable a company’s assets are. In other words, it indicates how effectively a company generates profits from its assets.

Return on equity (ROE): This ratio measures the profitability of a company’s equity. It shows how effectively a company generates profits from its shareholders’ investments.

Analysts and investors use profitability ratios to evaluate a company’s performance and profitability ability.

An investor or analyst can evaluate a company’s relative strength and identify potential opportunities or risks by comparing its profitability ratios with its peers or its industry averages.

See less