Introduction A capital reduction account is an account used to pass entries related to the internal reconstruction of a company. During reconstruction, paid-up capital reduced is credited to this account; hence its name is capital reduction account. It is also known as the reconstruction account. TyRead more

Introduction

A capital reduction account is an account used to pass entries related to the internal reconstruction of a company. During reconstruction, paid-up capital reduced is credited to this account; hence its name is capital reduction account. It is also known as the reconstruction account.

Type of account

A capital reduction account is a temporary account open just to carry out internal reconstruction. It represents the sacrifices made by the shareholders, debenture holders and creditors. Also, any appreciation in the value of assets is credited to this account. It is closed to capital reduction when internal reconstruction is completed.

Entries passed through capital reduction account

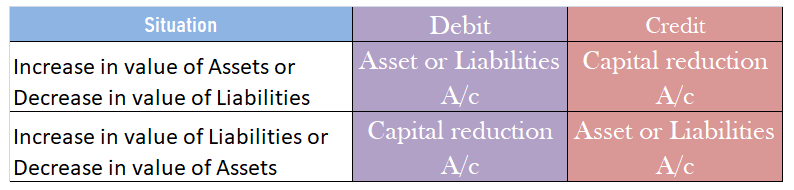

When paid-up capital is cancelled.

When paid-up capital is cancelled, the share capital account is debited and the capital reduction account is debited as share capital is getting reduced.

| Share Capital A/c | Dr. | Amt |

| To Capital Reduction A/c | Cr. | Amt |

When assets and liabilities are revalued

At the time of internal reconstruction, the gain or loss on revaluation is transferred to the capital reduction account instead of the revaluation reserve.

Writing off of accumulated losses and intangible assets

The credit balance of the capital reduction account is used to write off the accumulated losses and intangible assets like goodwill, patents etc which are unrepresented by capital. The capital reduction account is debited and profit and loss account and intangible assets accounts are credited.

| Capital Reduction A/c | Dr. | Amt |

| To Profit and loss A/c | Cr. | Amt |

| To Goodwill/ Patents A/c | Cr. | Amt |

Treatment in books of account

The balance in the capital reduction account, whether debit or credit, it is transferred to the capital reduction account. Hence, it doesn’t appear on the balance sheet.

See less

Bank Reconciliation Statement or BRS is a statement prepared to reconcile the bank account balance as per the cashbook with the bank balance as per the passbook. This is done so because often the bank balance as per the cashbook does not match with the bank balance as per the passbook. BRS is usuallRead more

Bank Reconciliation Statement or BRS is a statement prepared to reconcile the bank account balance as per the cashbook with the bank balance as per the passbook. This is done so because often the bank balance as per the cashbook does not match with the bank balance as per the passbook.

BRS is usually prepared by the accountant of an entity to find out the causes of the difference between the bank balance as per cashbook and the bank balance as reported in the passbook. The frequency of preparation of BRS is usually monthly. Nowadays, many enterprises have computerised accounting systems which help in automatic bank reconciliation.

Sometimes, BRS is also prepared by auditors during the audit of financial statements.

The balance of the bank account column of the cashbook does not match the bank balance as per the passbook. This is due to many transactions like the following that go unnoticed by the accountant:

Differences also occur due to accounting errors like posting wrong amounts in the cashbook.

To prepare the BRS, we have to start either with the bank balance as per cashbook, then add or subtract amounts to arrive at the bank balance as per passbook. Or we can do the vice verse. Here, the amounts we add or subtract are the amounts of items that are causes for the difference between the two balances.

See less