Effective Capital is an amount calculated for purpose of arriving at the maximum limit of managerial remuneration as per the Companies Act, 2013 where profit is inadequate or no profit. Other than that it has no use. Computation of effective capital is given in Explanation I to Schedule II of the CoRead more

Effective Capital is an amount calculated for purpose of arriving at the maximum limit of managerial remuneration as per the Companies Act, 2013 where profit is inadequate or no profit. Other than that it has no use.

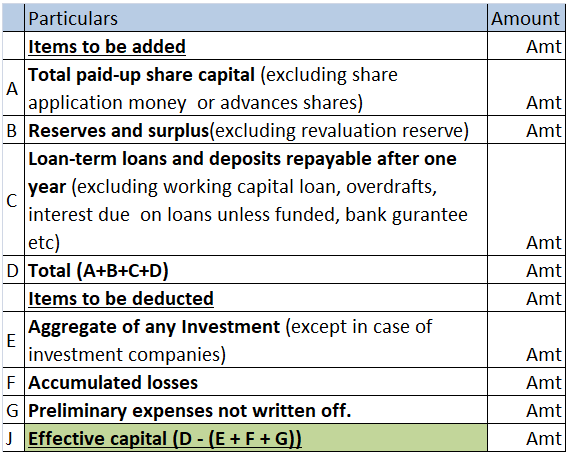

Computation of effective capital is given in Explanation I to Schedule II of the Companies Act. Schedule II deals with remuneration payable to managers in case of no profit or inadequate profit in the following manner:

Computation of effective capital is done in the following manner:

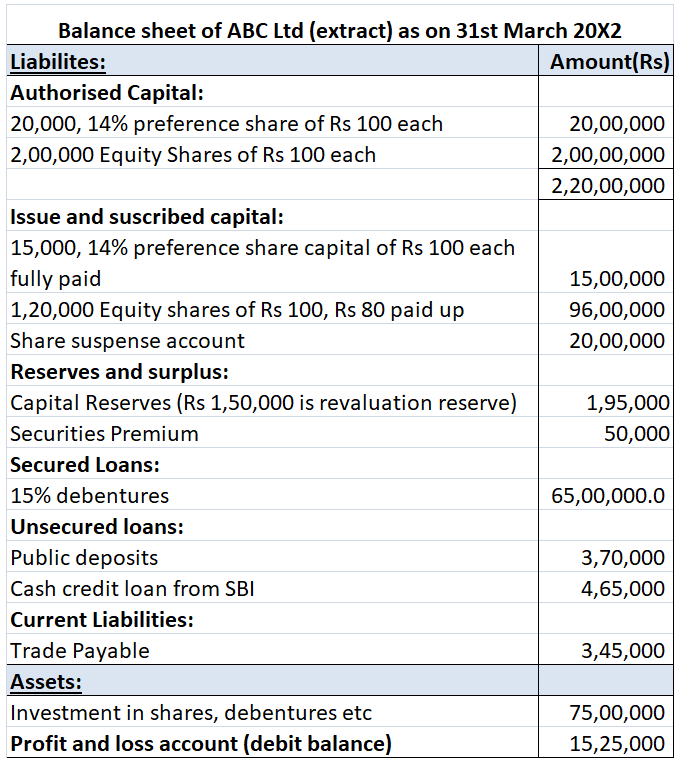

Numerical example:

ABC Ltd reports its balance sheet as given below:

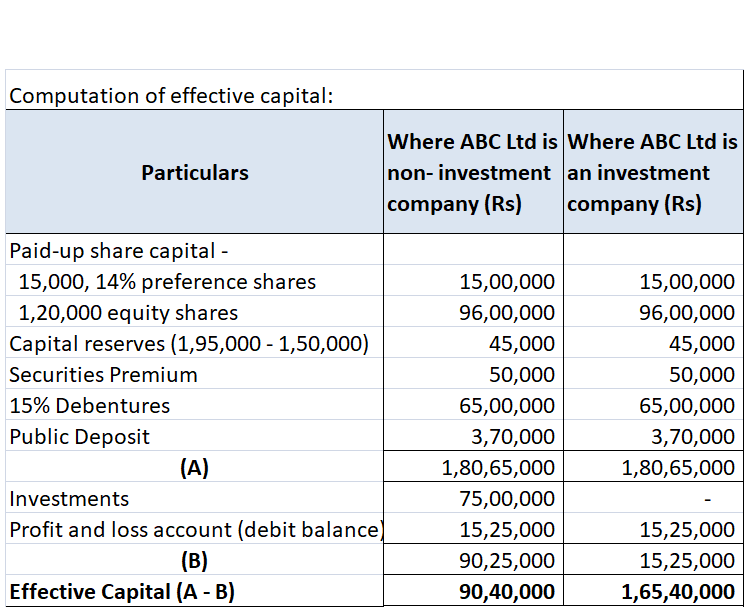

We will compute its effective capital for both an investment company and a non-investment company.

A cash flow statement is a statement showing the inflow and outflow of cash and cash equivalents during a financial year. Cash Flow Statements along with Income statements and Balance Sheet are the most important financial statements for a company. The Cash Flow Statement provides a picture to the sRead more

A cash flow statement is a statement showing the inflow and outflow of cash and cash equivalents during a financial year. Cash Flow Statements along with Income statements and Balance Sheet are the most important financial statements for a company.

The Cash Flow Statement provides a picture to the shareholders, government, and the public of how the company manages its obligations and fund its operations. It is a crucial measure to determine the financial health of a company.

The Cash Flow Statement is created from the Income Statement and the Balance Sheet. While Income Statement shows money engaged in various transactions during the year, the Balance Sheet presents information about the opening and closing balances.

The primary objective of a Cash Flow Statement is to present a record of inflow and outflow of cash, cash equivalents, and marketable securities through various activities of a company.

Various activities in a company can be broadly classified into three parts or heads:

Cash Flow Statements also present a picture of the liquidity of the company and are therefore used by the management of a company to take decisions with the help of the right information.

Cash Flow Statements are a great source of comparison between a company’s last year’s performance to its current year or with other companies in the same industry and hence, helps shareholders and potential investors to make the right decisions.

It also helps to differentiate between non-cash and cash items; incomes and expenditures are divided into separate heads.

See less