As per AS-10 ( Revised ): Property, Plant and Equipment, depreciation on an asset should begin when the asset is in the location and condition necessary for it to be capable of operating in the manner as intended by the management. This means a firm should start charging depreciation when the assetRead more

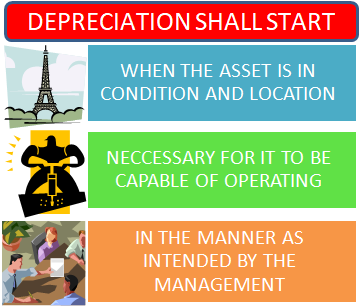

As per AS-10 ( Revised ): Property, Plant and Equipment, depreciation on an asset should begin when the asset is in the location and condition necessary for it to be capable of operating in the manner as intended by the management.

This means a firm should start charging depreciation when the asset is ready to be used as per the management’s desire.

Let’s take an example to understand this clearly:

A business bought a drinking water cooler for its office use on 1st April 2021. Now, this water cooler needs to be installed and wiped with Isopropyl Alcohol before it can be put to use.

The business completed all the required procedures by 1st May 2021, but it opened the machine for office use from 1st August 2021.

So the question arises, from when to start charging depreciation?

- 1st April 2021 – The date of Purchase

- 1st May 2021- The date when the machine was ready to use.

- 1st August 2021 –The date from which the machine was put to use.

The answer is 1st May 2021– The date when the machine was ready to use.

It doesn’t matter whether the company started the use of an asset or not. Once an asset is in

- the location and condition

- necessary for it to be capable of operating

- as intended by the management,

the depreciation should begin.

See less

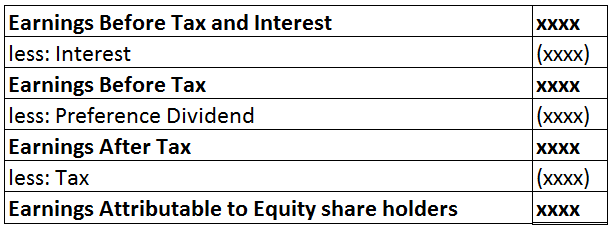

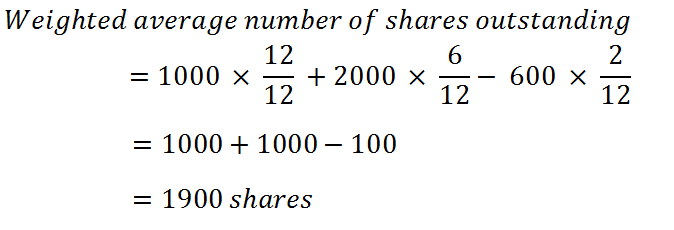

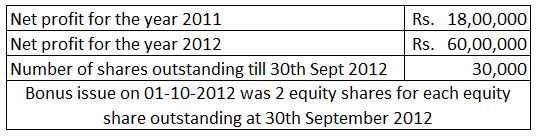

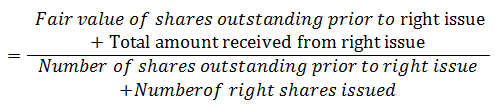

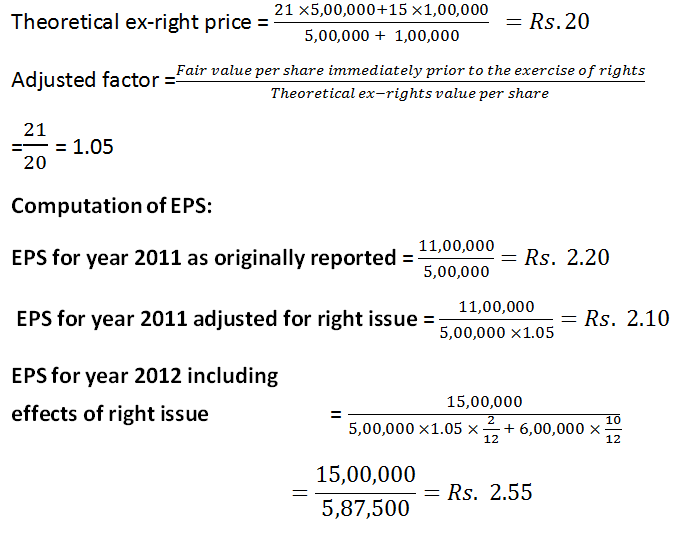

Earnings per share indicate the profit-generating capability of an enterprise and potential investors often compare the EPS of different companies to choose the best investment alternative.

Earnings per share indicate the profit-generating capability of an enterprise and potential investors often compare the EPS of different companies to choose the best investment alternative.

International Financial Reporting Standards (IFRS) is a not-for-profit, public interest organization. The main objective of the IFRS Foundation is to raise the standard of financial reporting and bring about global harmonization of accounting standards. IFRS was established to develop high-quality,Read more

International Financial Reporting Standards (IFRS) is a not-for-profit, public interest organization. The main objective of the IFRS Foundation is to raise the standard of financial reporting and bring about global harmonization of accounting standards.

IFRS was established to develop high-quality, understandable, enforceable, and generally accepted accounting standards. International Accounting Standards Board (IASB) develops IFRS. There are currently 16 IFRSs in issue.

Benefits of IFRS Standards:

Following are the uses of IFRS:

Challenges faced by companies if IFRS is not implemented:

- The financial statements will differ for the companies who have offices worldwide and use only national accounting standards.

- Increased complexity while preparing financial statements.

- Difficulty in comparing and verifying financial statements.

- Accounting of transactions will differ from country to country if IFRS is not implemented.

See less