When a business deposits its money into a bank account, it receives a percentage of the amount deposited as bank interest. The journal entry for interest received from a bank is as follows: Since the Bank account is a current asset, it gets debited. This is in accordance with the modern rules of accRead more

When a business deposits its money into a bank account, it receives a percentage of the amount deposited as bank interest. The journal entry for interest received from a bank is as follows:

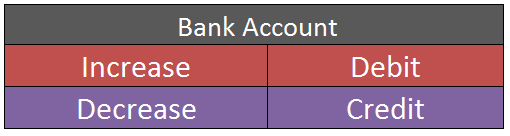

Since the Bank account is a current asset, it gets debited. This is in accordance with the modern rules of accounting where an increase in assets is debited while a decrease in assets is credited. According to the traditional rules (golden rules) of accounting, a bank account is classified under Personal account with the rule of “debit the receiver” and “credit the giver”. In the given journal entry bank account is receiving money and is hence debited.

Meanwhile, Bank interest is the income received by the business and according to the modern rule of accounting, an increase in incomes is credited and a decrease in incomes is debited. Whereas, considering the traditional rules (golden rules), bank interest comes under Nominal account where “all incomes are credited” and “all expenses are debited”. Therefore, considering these rules, bank interest is credited.

EXAMPLE

If Gregor Ltd has a bank account with HSBC, having an opening balance of Rs 10,000 earning an interest of 5% per annum, then the journal entry for interest received from the bank is recorded as

The interest amount is taken on the amount deposited in the bank (10,000 * 5%).

See less

An asset is an item of property owned by a company/business. It may be for a longer or shorter period of time. Assets are classified into two broad heads: Non-Current Assets Current Assets The asset may be sold for several reasons such as: An asset is fully depreciated. It should be sold becaRead more

An asset is an item of property owned by a company/business. It may be for a longer or shorter period of time. Assets are classified into two broad heads:

The asset may be sold for several reasons such as:

The journal entry for profit on the sale of assets will be:

According to the golden rules of accounting, in the above entry “Cash/Bank A/c” it is a Real Account and the rule says “Debit what comes in” and so is debited.

“Asset A/c” is a real account and the rule says “Credit what goes out” and so is credited. Any Gain on sale of an asset goes to the Nominal account and according to the rule “Credit, all incomes and gains” and so is credited.

The journal entry for loss on sale of the asset will be:

In the above entry, “Loss on Sale of Asset” is debited because according to Nominal account rules “Debit all losses and expenses” and so is debited.

According to modern rules of accounting, “Debit entry” increases assets and expenses, and decreases liability and revenue, a “Credit entry” increases liability and revenue, and decreases assets and expenses.

For example, Mr. A sold furniture for $2,500 and incurred a loss on the sale which amounted to $2,500.

According to modern rules, the journal entry will be: