The journal entry for the dividend collected by the bank is as follows: Bank A/c Dr. Amt To Dividend Received A/c Amt Here, Bank Account is debited and the Dividend Received Account is credited. This treatment is explained below. The logRead more

The journal entry for the dividend collected by the bank is as follows:

| Bank A/c Dr. | Amt | |

| To Dividend Received A/c | Amt |

Here, Bank Account is debited and the Dividend Received Account is credited. This treatment is explained below.

The logic behind the journal entry

This can be explained through the following rules of accounting:

- Golden rules of accounting

- Modern rules of accounting

Golden rules of accounting

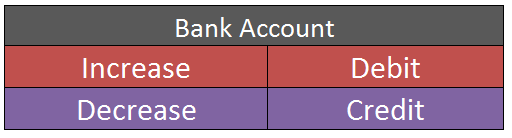

A bank account is a real account and the golden rule of accounting for the real account is, “Debit what comes in and credit what goes out”

Hence, the bank account is debited as the money is coming into the bank.

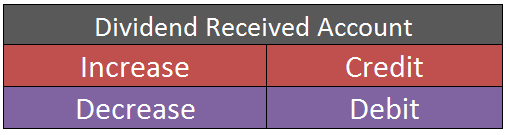

Dividend is an income hence dividend received is a nominal account. The golden rule of accounting for a nominal account is “Debit all expenses and losses and credit all income and gains”

Hence, the dividend received account is credited as income.

Modern rules of accounting

As per modern rules of accounting, a bank account is an asset account.

The asset account is debited when increased and credited when decreased.

Hence, the Bank account is debited here as it is increased.

A dividend received account is an income account.

The income account is credited when increase and debited when decreased.

Hence, the dividend received account is credited here as it is increased.

Treatment in the financial statements

Since the dividend received is an income; it is shown on the credit side of the Statement of profit and loss.

The bank account is an asset so it will be shown on the balance sheet.

See less

To start with let me give you a brief explanation of what a subscription is After joining a not-for-profit organization, a member is required to pay a certain amount of money every year at periodical intervals in order to keep his membership activated, such an amount of money is the subscription. FoRead more

To start with let me give you a brief explanation of what a subscription is

After joining a not-for-profit organization, a member is required to pay a certain amount of money every year at periodical intervals in order to keep his membership activated, such an amount of money is the subscription.

For accounting purposes, subscription is always taken on an accrual basis which means the amount which is received during the current year is only taken into consideration.

Now, Subscription received in advance means the amount of money that has been received during the current year but which relates to the year that is yet to come. In other words, we can say it is the unearned income by the organization.

It is recurring in nature and liability for the organization as it does not relate to the current year.

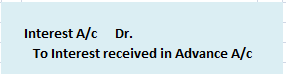

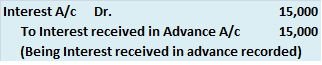

Journal Entry for Subscription received in advance

Here, the Subscription received in advance is credited to the Subscription account for the current year.

This is the adjustment entry made during the current year.

Treatment of Subscription in Financial Statements

Receipts and Payment account: In the receipts and payment account, the entire amount of subscription is written on the receipts side. That is to say, subscription amount relating to the previous year, current year, and the year to come (outstanding subscription, current year subscription, advance subscription).

Income and Expenditure account: In the Income and Expenditure Account, the subscription comes on the Income side. It is shown as

Here, a subscription received in advance in the current year is deducted to find the actual amount because although the money is received in advance the benefits related to it are yet to be provided by the organization.

Balance sheet: In the balance sheet, a subscription received in advance comes in the liability side under current liabilities as the benefits related to it are yet to be derived.

For Example, Lionel club received subscription from its members for the year 2020 as follows-

The total subscription was received during the year – 10,000

Here,

Subscription of 2020 was received in 2019- It is an Outstanding Subscription.

Subscription of 2021 was received in 2020- It is an advance Subscription.

See less