Interest on Investment is to be shown on the Credit side of a Trial Balance. Interest on investment refers to the income received on investment in securities. These securities can be shares, debentures etc. of another company. When one invests in securities, they are expected to receive a return onRead more

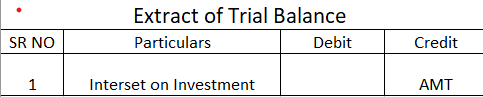

Interest on Investment is to be shown on the Credit side of a Trial Balance.

Interest on investment refers to the income received on investment in securities. These securities can be shares, debentures etc. of another company. When one invests in securities, they are expected to receive a return on investment (ROI).

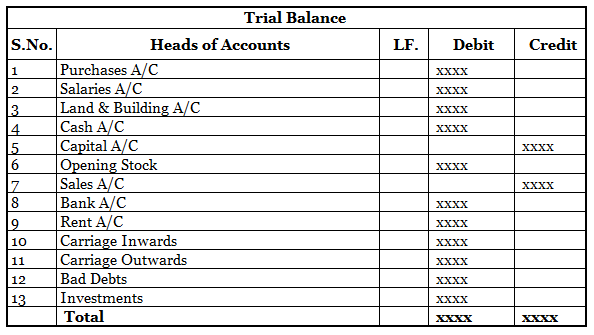

Since interest on investment is an income, it is shown on the credit side of the Trial Balance. This is based on the accounting rule that all increase in incomes are credited and all increase in expenses are debited. A Trial Balance is a worksheet where the balances of all assets, expenses and drawings are shown on the debit side while the balances of all liabilities, incomes and capital are shown on the credit side.

For example, if Jack bought Corporate Bonds of Amazon, worth $50,000 with a 10% interest on investment, then the accounting treatment for interest on investment would be

Cash/Bank A/C Dr 5,000

To Interest on Investment in Corporate Bonds (Amazon) 5,000

As per the above entry, since interest on investment is credited, it will show a credit balance and hence be shown on the credit side of the Trial Balance. Interest on investment account is not to be confused with an Investment account. Investment is an asset whereas interest on investment is an income.

See less

Yes, the account receivable is a sub ledger account. It is an account that is used to record the payment history of each and every customer to whom the business has sold goods or provided services on credit. Accounts receivable represent the amount that the customers owe to the business with respectRead more

Yes, the account receivable is a sub ledger account. It is an account that is used to record the payment history of each and every customer to whom the business has sold goods or provided services on credit.

Accounts receivable represent the amount that the customers owe to the business with respect to the goods sold or services provided to them on credit. They are also known as trade receivable or debtors.

The accounts receivable subledger shows various details of every transaction like the invoice number, amount due, date of payment, discount allowed etc. The subledger accounts are also known as the subsidiary accounts.

Difference between general ledger and subledger accounts

Here is a list of the major differences between sub-ledgers and the general ledger:

Importance/ use of Subsidiary Account

The usefulness of an accounts receivable sub ledger account lies in the fact that it provides detailed information about the money different customers owe to the business.

For example, the general ledger account may show that the total balance of trade receivable is 1 lakh without indicating the individual amount that each customer owes to the business. The subsidiary account can help us by showing that customer A owes 50000 rupees, customer B owes 30000 rupees while customer C owes 20000 rupees.

In short, the subsidiary accounts provide detailed information about each and every transaction. They help us to find useful information quickly and easily. They help us analyze the business policies and take corrective actions.

Thus, we can conclude that accounts receivable is a subledger account that provides us detailed information about the various credit transactions and the amount that each customer owes to the business. It helps us analyze our credit policies and take corrective actions. It helps us identify and classify bad debts as such on

See less