Negative working capital means the excess of current liabilities over current assets in an enterprise. Let’s understand what working capital is to get more clarity about negative working capital. Meaning of Working Capital Working Capital refers to the difference between current assets and current lRead more

Negative working capital means the excess of current liabilities over current assets in an enterprise.

Let’s understand what working capital is to get more clarity about negative working capital.

Meaning of Working Capital

Working Capital refers to the difference between current assets and current liabilities of a business.

Working Capital = Current Assets – Current Liabilities

It is the capital that an enterprise employs to run its daily operations. It indicates the short term liquidity or the capacity to pay off the current liabilities and pay for the daily operations.

Items under Current Assets and Current Liabilities

It is important to know about the items under current assets and current liabilities to understand the significance of working capital.

Current assets include cash and bank balance, accounts receivables, inventories, short term investments, prepaid expenses etc.

Current liabilities include accounts payable, short term loans, bank overdraft, interest on short term investment, outstanding salaries and wages etc.

Types of working capital

Since the working capital is just the difference between current assets and liabilities, the working capital can be one of the following:

- Positive (Current assets > Current liabilities)

- Zero (Current assets = Current liabilities)

- Negative (Current assets < Current liabilities)

Hence, negative working capital exists when current liabilities are more than current assets.

Implications of having negative working capital

Having negative working capital is not an ideal situation for an enterprise. Having negative working capital indicates that the enterprise is not in a position to pay off its current liabilities and there may be a cash crunch in the business.

An enterprise may have to finance its working capital requirements through long term finance sources if its working capital remains negative for quite a long time.

The ideal situation is to have current assets two times the current liabilities to maintain a good short term liquidity of the business i.e.

Current Assets = 2(Current Liabilities)

See less

Revenue also called income is nothing but the income generated by individuals or businesses from the sale of goods or investing capital or assets. Some examples of revenue are as follows:- Sales revenue Dividend received Interest earned Rent received Commission 1. SALES REVENUE Sales revenueRead more

Revenue also called income is nothing but the income generated by individuals or businesses from the sale of goods or investing capital or assets. Some examples of revenue are as follows:-

1. SALES REVENUE

Sales revenue is the income received by the individual or business by selling its product or provision of services. the words “sale” and “revenue” are used interchangeably to mean the same thing. It is to be noted that revenue does not necessarily mean it has been received in cash, it can be partly in cash or partly on credit also.

How to calculate sales revenue?

SALES REVENUE = NO. OF UNITS SOLD * AVERAGE PRICE PER UNIT

For example:- Amazon sold 4000 units of shirts @ 500 each. Therefore sales revenue for amazon is

Sales revenue = 4000 * 500

= 20,00,000

Treatment of sales revenue in the financial statement, since sales are part of a trading account and appear on the credit side of the trading account.

2. DIVIDEND RECEIVED

Naina, this can be explained in simple terms. Suppose you own shares of a company which declares dividend so the dividend received is income for you. Since it does not reduce the assets of a company nor creates a liability it is shown as income and posted on the credit side of profit & loss A/c.

Let me give you a short example of a dividend received, suppose you own 1000 shares of ABC.ltd. the company at the quarter-end calculate its earnings and decides to declare a dividend of Rs 5 per share. Therefore you would receive 1000* 5 i.e Rs 5000 as dividend income.

3. INTEREST INCOME EARNED

Interest income is the earnings the entity receives on any investments made. To be more precise it is money earned by an individual or business for lending their fund either by putting them as deposit in the bank. It is shown on the credit side of the profit & loss A/c.

A very simple example for interest earned is when a business or an individual deposits money in the bank as savings and decided not to touch it for the coming years then such a depositor will gain interest on such savings by the bank. such type of income so received is treated as interest received and shown as income in the profit & loss A/c.

3. RENT RECEIVED

When money is received by the business for exchange of use of assets of the business by the other person, then it will be called rent received. Rent can be received by the business firm in respect of land, building, machinery, etc. As rent received is income for the business firm, it is shown on the credit side of profit & loss A/c.

For example, X. ltd received Rs 20,000 via cash on one of its properties to Mr. Z. Then rent so received shall be treated as income in the books of ABC. ltd and same shall be treated as income and shown in the profit & loss statement.

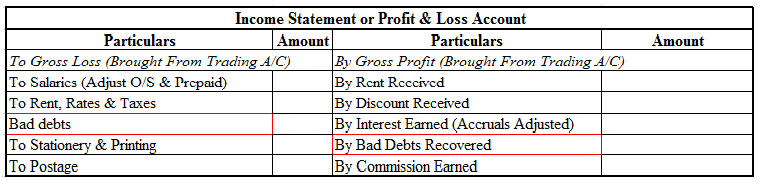

Summarised extract of profit & loss account is shown below for dividend received, Rent received and interest earned.

See less