All expenses whose benefits are received over the years or the expenses or losses that are to be written off over the years are classified as Deferred revenue expenses. It includes fictitious expenses like preliminary expenses, loss on issue of debentures, advertising expenses, loss due to unusual oRead more

All expenses whose benefits are received over the years or the expenses or losses that are to be written off over the years are classified as Deferred revenue expenses. It includes fictitious expenses like preliminary expenses, loss on issue of debentures, advertising expenses, loss due to unusual occurrences like loss due to fire, theft, and research and development expenses, etc.

DEFERRED REVENUE EXPENSES

There are certain expenses which are revenue in nature (i.e. expenses incurred to maintain the earning capacity of the firm and generate revenue) but whose benefits are received over a period of years generally between 3 to 7 years. It means its benefit is received not only in the current accounting period but over a few consecutive accounting periods.

CHARACTERISTICS

- Revenue in nature

- Benefits received for more than one accounting period.

- Huge expenditure (large amount is involved)

- Affects the profitability of the business (since a large amount is involved if charged in the same accounting period, then it will decrease the profitability for the year)

- Written off over the years either partially or entirely.

- Fictitious asset It doesn’t result in the creation of any asset but is shown as an asset (fictitious asset) on the Balance Sheet till fully written off.

EXAMPLES

ADVERTISING EXPENSES refers to the expenses incurred for promoting the goods or services of the firm through various channels like TV, Social media, Hoardings, etc.

As the benefit of advertising is not received not only in the period when such expenses were incurred but also in the coming few years, it is classified as Deferred revenue expense.

For example – Suppose the company incurred $10 lakh on advertising to introduce a new product in the market and estimated that its benefit will last for 4 years. In this case, $250,000 will be written off every year, for 4 consecutive years.

EXCEPTIONAL LOSSES are losses that are incurred because of some unusual event and don’t happen regularly like loss from fire, theft, earthquake, flood or any other natural disaster, confiscation of property, etc.

Since these losses can’t be written off in the year they occurred they are also treated as Deferred revenue expenditure and are written off over the years.

RESEARCH AND DEVELOPMENT EXPENSES are expenses incurred on researching and developing new products or improving the existing ones. Its benefits are received for many years and thus are classified as Deferred revenue expenses.

For example – Expenses incurred on the creation of intangible assets like patents, copyrights, etc.

PRELIMINARY EXPENSES are those expenses which are incurred before the incorporation and commencement of the business. It includes legal fees, registration fees, stamp duty, printing expenses, etc.

These expenses are fictitious assets and are written off over the years.

TREATMENT

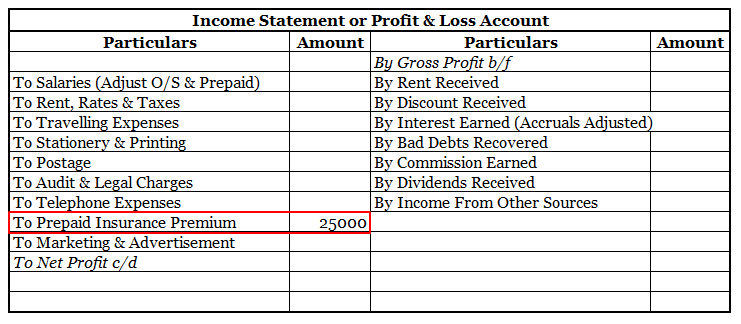

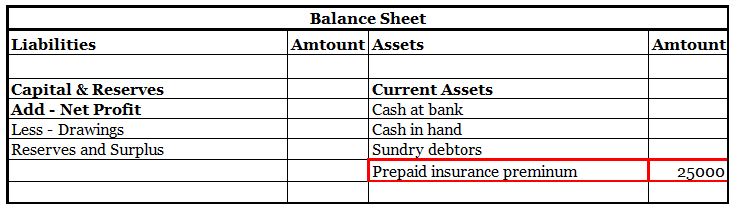

It is debited to the P&L amount (amount written off that year) and the remaining amount on the Aeest side of the Balance Sheet.

In the above example of advertising expenses, in Year 1, $250,000 will be debited in the P&L A/c and the remaining amount of $750,000 is shown on the Asset side of the Balance Sheet.

In Year 2, $250,00 in P&L A/c and the remaining $500,000 in Balance Sheet.

In Year 3, $250,000 in P&L A/c and the remaining $250,000 in the Balance Sheet and in the last Year 4, only the remaining amount of $250,000 in P&L A/c and nothing in the Balance Sheet.

See less

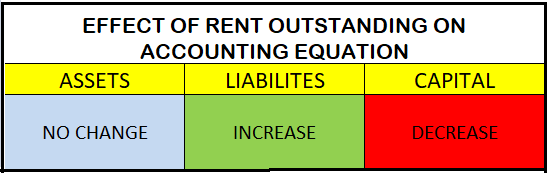

Accruals are not the same as provisions both are totally different from each other. Accruals and provision both are vital parts of accounts but work differently Accrual Accrual expense means the transaction that takes place in a particular period must be accounted for in that period only irreRead more

Accruals are not the same as provisions both are totally different from each other. Accruals and provision both are vital parts of accounts but work differently

Accrual

Accrual expense means the transaction that takes place in a particular period must be accounted for in that period only irrespective of the fact when such an amount has been paid.

An accrual of the expenditure which is not paid will be listed in the books of accounts. These accruals can be further divided into two parts

Accrual Expense

Accrual Expense means any transaction that takes place in a particular period but the amount for it will be paid on a later period.

For example- 10,000 for the month of March was paid in April month then this rent will be accounted for in the books in March

These are the following accrued expense

Accrual Revenue

Accrual Revenue means any transaction that takes place in a particular period but the amount for it will be received on later period. For example- If interest of 10,000 on bonds for the period of March is received in April months then this amount will be accounted for in March. These are the following accrued revenue

PROVISIONS

Provision refers to making a provision/allowance against any probable future expense that the company might incur in the near future. This amount is uncertain and difficult to predict its surety.

However, as per the prudence concept of accounting a company needs to anticipate the losses that will incur in the near future due to which provision is made.

For example- A company has debtors of 10,000 but as per the company’s previous records company anticipates that 1% of debtors will become bad debts. So in this case company will make a provision of 1% that is 100 on it.

There are various types of provisions which are-

- Provision on Depreciation– Provision for Depreciation means a provision for future depletion of assets has been already created

- Provision for Doubtful Debts– Provision for Doubtful Debts means a provision created against debtors that doesn’t seem to be recovered in the near future

See less