Sundry Debtors Sundry Debtors are those persons or firms to whom goods have been sold or services rendered on credit and the payment has not been received from them. In other words, Debtors are the persons or firms from whom the payment is to be received by the business. For Example, Ramen Sold goodRead more

Sundry Debtors

Sundry Debtors are those persons or firms to whom goods have been sold or services rendered on credit and the payment has not been received from them. In other words, Debtors are the persons or firms from whom the payment is to be received by the business.

For Example, Ramen Sold goods to Sam on credit, Sam did not pay for the goods immediately, so here Sam is the debtor for Ramen because he owes the amount to Ramen.

Another Example, If goods worth Rs 7000 have been sold to Sid on credit, he will continue to remain as debtor of the business so long as he does not make the full payment.

Treatment:

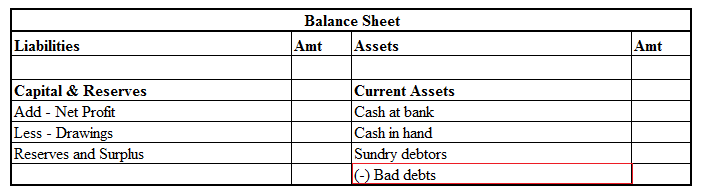

Sundry Debtor is considered as a current asset and hence it is shown on the assets side of the balance sheet under the Current Assets heading.

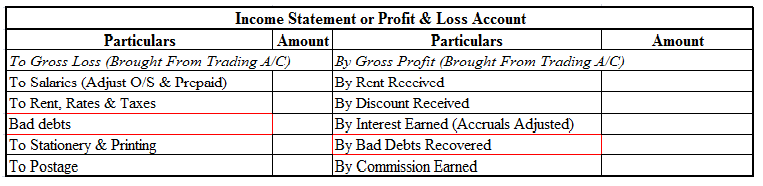

Sundry Debtors are not considered as an item of profit and loss because it is not considered as an item of income or expense. However, the items associated with sundry debtors such as bad debts or provision for doubtful debts or bad debts recovered are shown in profit and loss accounts in the debit and credit sides respectively.

Sundry Creditors

Sundry creditors are those persons or firms from whom goods have been purchased or services rendered on credit and for which payment has not been made. In other words, Creditors are the person or firms to whom some money has to be paid by the business.

For Example, Ramen purchased goods from Sam on credit, Ramen did not pay for the goods immediately, so here Ramen is the creditor for Sam because he owes money to Sam.

Another Example, If Mr. Johnson purchased goods worth Rs 3000 from M/s. Rick & Co. on credit, Mr. Johnson will continue to remain as a creditor of M/s. Rick & Co. as long as the full payment is made by Mr. Johnson.

Treatment:

Sundry Creditor is shown in the liabilities side of the balance sheet under the heading Current Liabilities.

See less

Income and Expenditure A/c of Charitable Trust Income and Expenditure A/c is like the Profit and Loss A/c in the Balance Sheet of the Charitable Trust. All the income and expenses are, therefore, recorded in this. It is used to determine the surplus or deficit of income over expenditures over a specRead more

Income and Expenditure A/c of Charitable Trust

Income and Expenditure A/c is like the Profit and Loss A/c in the Balance Sheet of the Charitable Trust. All the income and expenses are, therefore, recorded in this. It is used to determine the surplus or deficit of income over expenditures over a specific accounting period.

It shows the summary of all the income and expenditures done by the charitable trust over an accounting year. All the revenue items relating to the current period are shown in this account, the expenses and losses on the expenditure side, and incomes and gains on the income side of the account.

Later on, they are even used in the Balance Sheet. As follows-

On the Assets Side

On the Liability Side

See less